2023年FPD生産能力は前年比2%減の見通し~計画延期やLGD/SDCのライン閉鎖が影響

冒頭部和訳

2023年のFPD生産能力は前年比2%減の見通しである。韓国メーカーのLG Display (LGD) とSamsung Display (SDI) が中国や韓国でLCD生産ラインの閉鎖や転換を実施、その他のメーカーも市況の低迷を受けて生産能力の増強計画を延期している。DSCCは Quarterly Display Capacity and Equipment Market Share Report (一部実データ付きサンプルをお送りします) において、2023年にはLCD生産能力が前年比3%減、OLED生産能力が前年比6%増となる予測を示している。マイナス成長が予測されているものの、生産能力シェアではLCDが2023年も依然として圧倒的で、面積ベースでは92%から下げるものの、シェア91%を確保するとみられる。

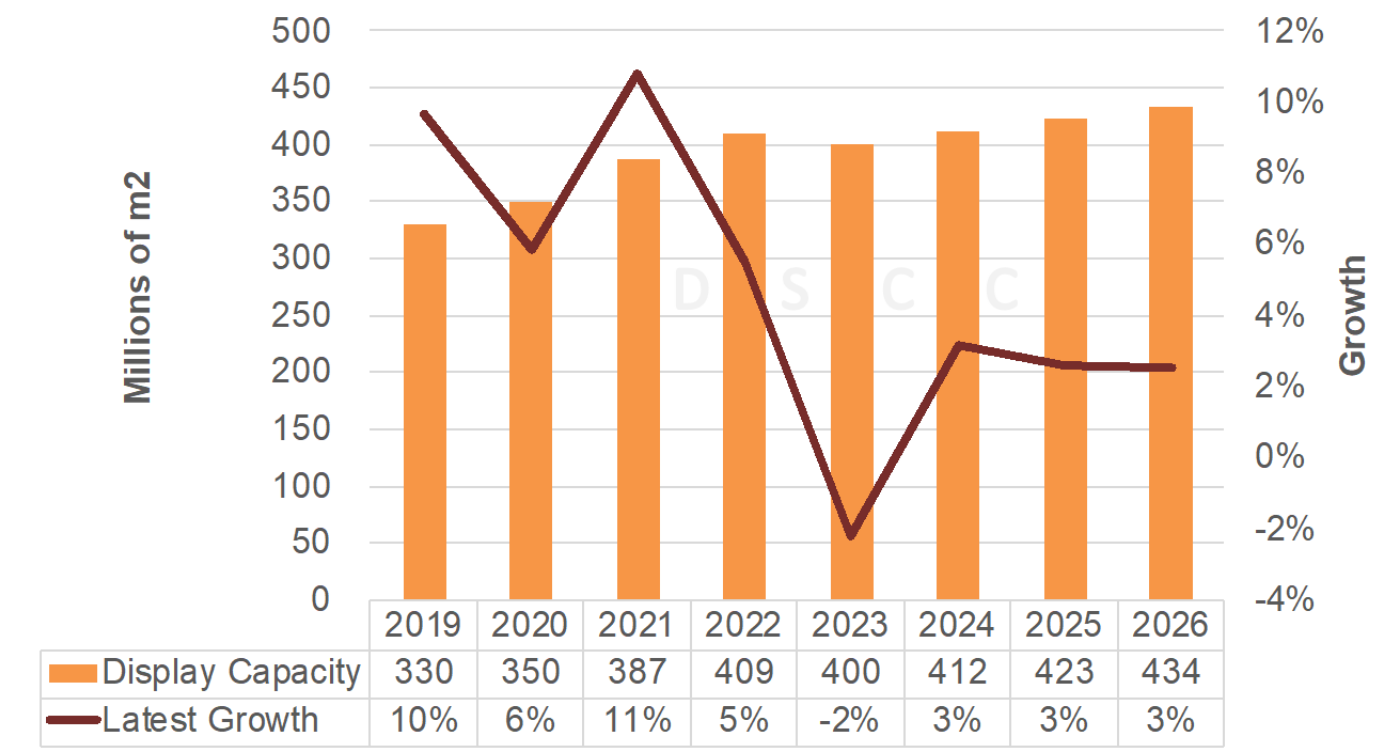

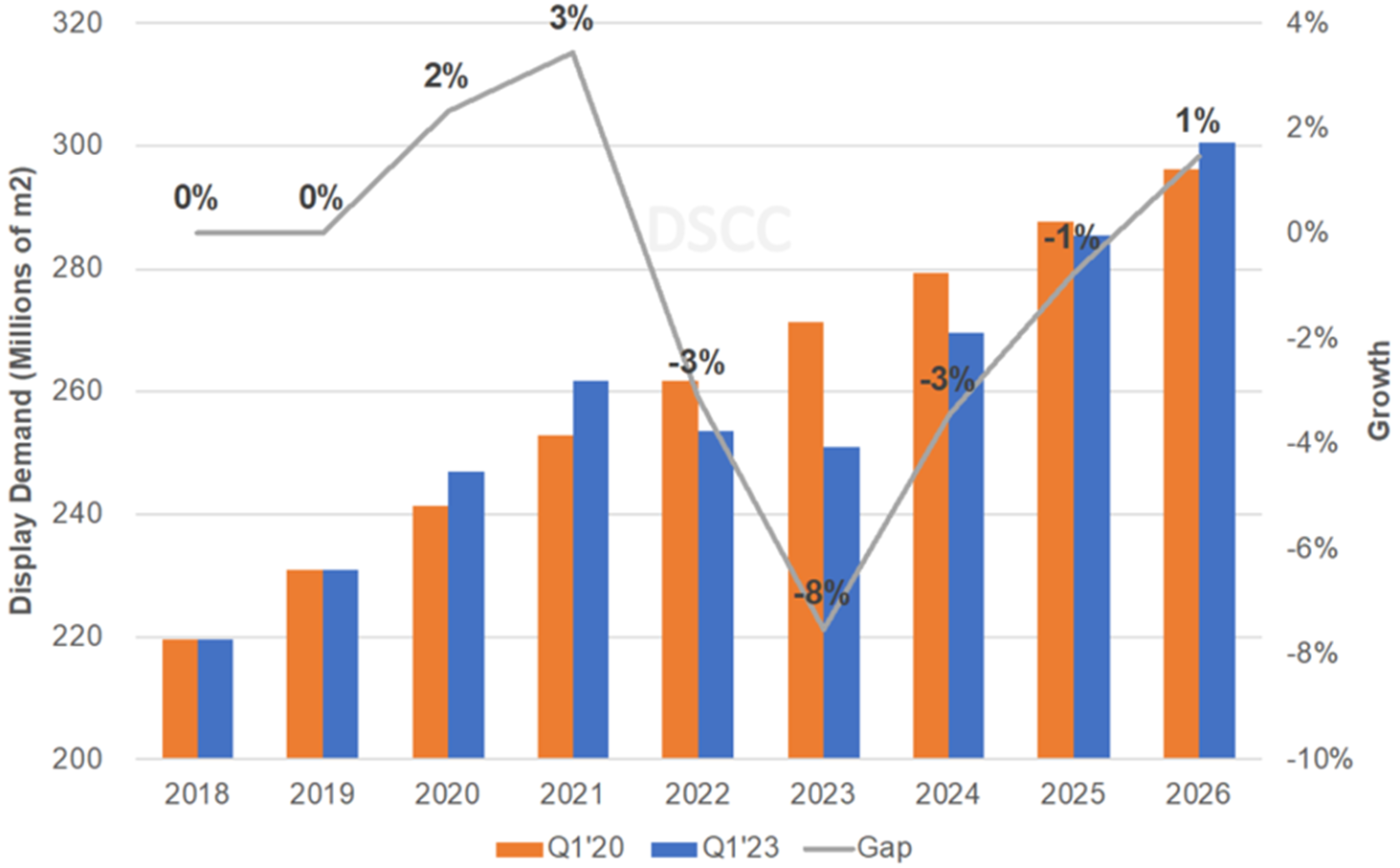

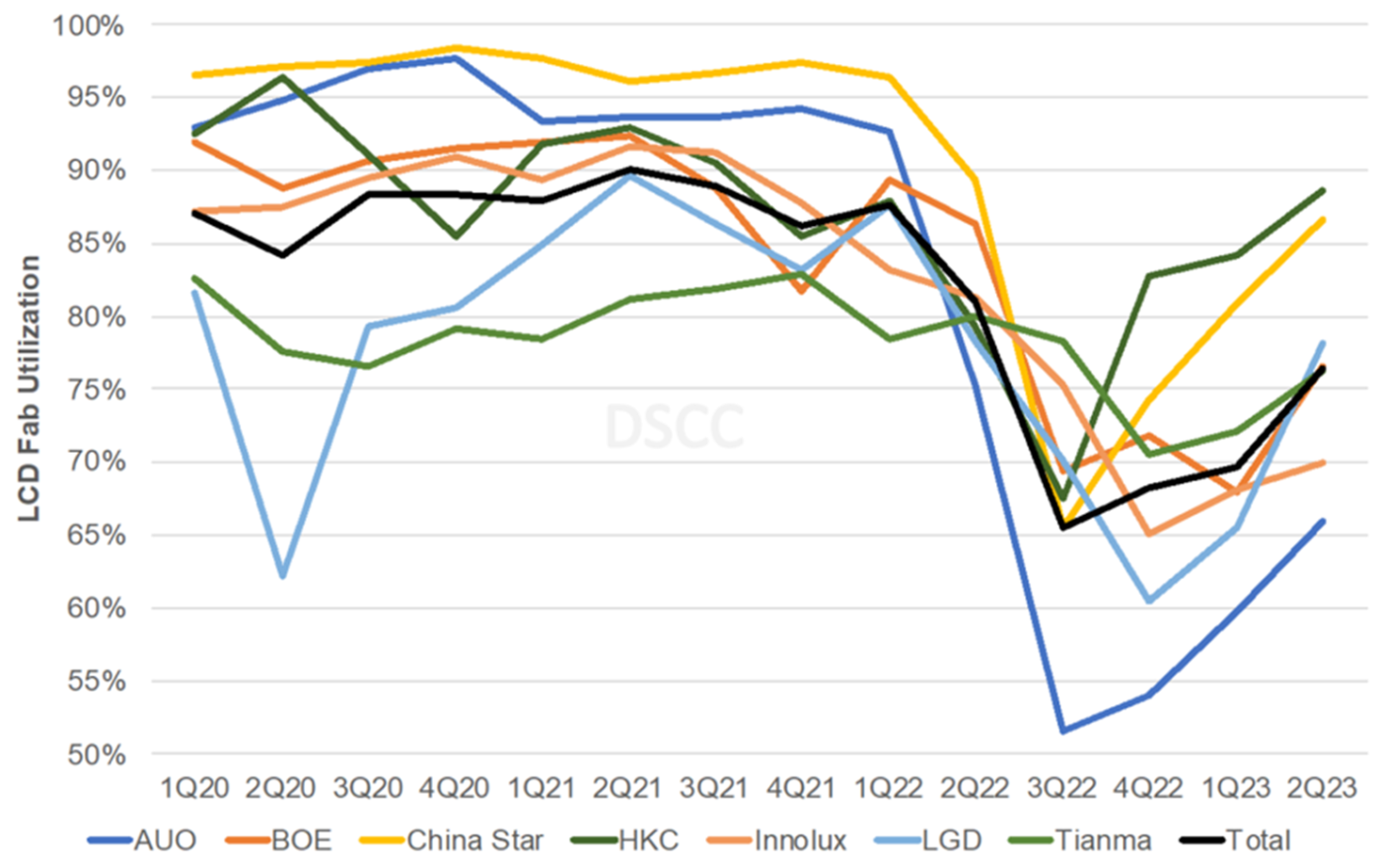

LCDは近年、どのメーカーにとっても不採算事業であることが明らかになっており、2022年にはパネル価格がキャッシュコストを下回るなか、各企業は需給と価格設定の状況改善を目指した新規投資を進めている。1つ目のグラフからわかるように、生産能力は2021年から2022年にかけて急速に増加している。2つ目のグラフからは、コロナ禍でバブル需要が拡大したことがわかる。その後、2022年から2023年にかけて需要と供給に大きなミスマッチが生じ、3つ目のグラフからわかるように、LCD生産ライン稼働率は極端に低くなった。そのため、各メーカーは2023年の設備投資を削減しており、先日掲載の記事で伝えたように、今年の設備投資額は2012年以来の最低水準になると予測されている。

DSCC Sees Display Capacity Down 2% in 2023 on Delays and LGD/SDC Shutdowns – LCDs Down 3%, OLEDs Up 6%

※ご参考※ 無料翻訳ツール (DeepL)

DSCC sees display capacity down 2% Y/Y in 2023 as Korean manufacturers LG Display and Samsung Display shut down or convert LCD capacity in China and/or Korea and other manufacturers delay capacity additions on weak market conditions. As indicated in DSCC’s Quarterly Display Capacity and Equipment Market Share Report (一部実データ付きサンプルをお送りします), DSCC sees LCD capacity falling 3% in 2023, with OLED capacity up 6%. Despite the 2023 decline, LCDs will still dominate display capacity on an area basis with a 91% share in 2023, down from 92%.

LCDs have proven unprofitable for all manufacturers of late and companies are pushing out new investments to try and improve the supply/demand and pricing situation with panel prices below cash cost in 2022. As indicated in the first figure, capacity rose rapidly in 2021 and 2022 and with demand pulled in during the COVID bubble as shown in the second figure, it has led to a large mismatch in supply and demand in 2022 and 2023 and very poor LCD utilization as shown in the third figure. For this reason, manufacturers are slashing capex in 2023, with equipment spending expected to be the lowest since 2012 as we recently reported here.

Display Capacity and Growth

Display Demand Pulled in During COVID

LCD Fab Utilization

DSCC estimates that LG Display is cutting its LCD capacity by 41% in 2023, which will reduce its LCD capacity market share from 10% in 2022 to 6% in 2023. DSCC believes LGD is cutting capacity at Fab 1 in Guangzhou, China as well as at P5, P6 and P7 in Korea. Its LCD capacity in China is expected to fall by 48%, with its Korea LCD capacity falling by 37% on an area basis. In 2023, Korea will account for 68% of its LCD capacity, up from 63% in 2022.

In SDC’s case, they stopped LCD production at its T8-2 line in Q2’22, so their LCD capacity will be down 100% in 2023.

We would not be surprised to see more shutdowns or industry consolidation until the industry rebounds.

For more information on display, LCD and OLED capacity, fab schedules and equipment spending, please see DSCC’s Quarterly Display Capacity and Equipment Market Share Report (一部実データ付きサンプルをお送りします).

本記事の出典調査レポート

Quarterly Display Capex and Equipment Market Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。