iPhone 14用パネル動向分析~調達量は3月も減少の見通し、LG Displayが成長継続

冒頭部和訳

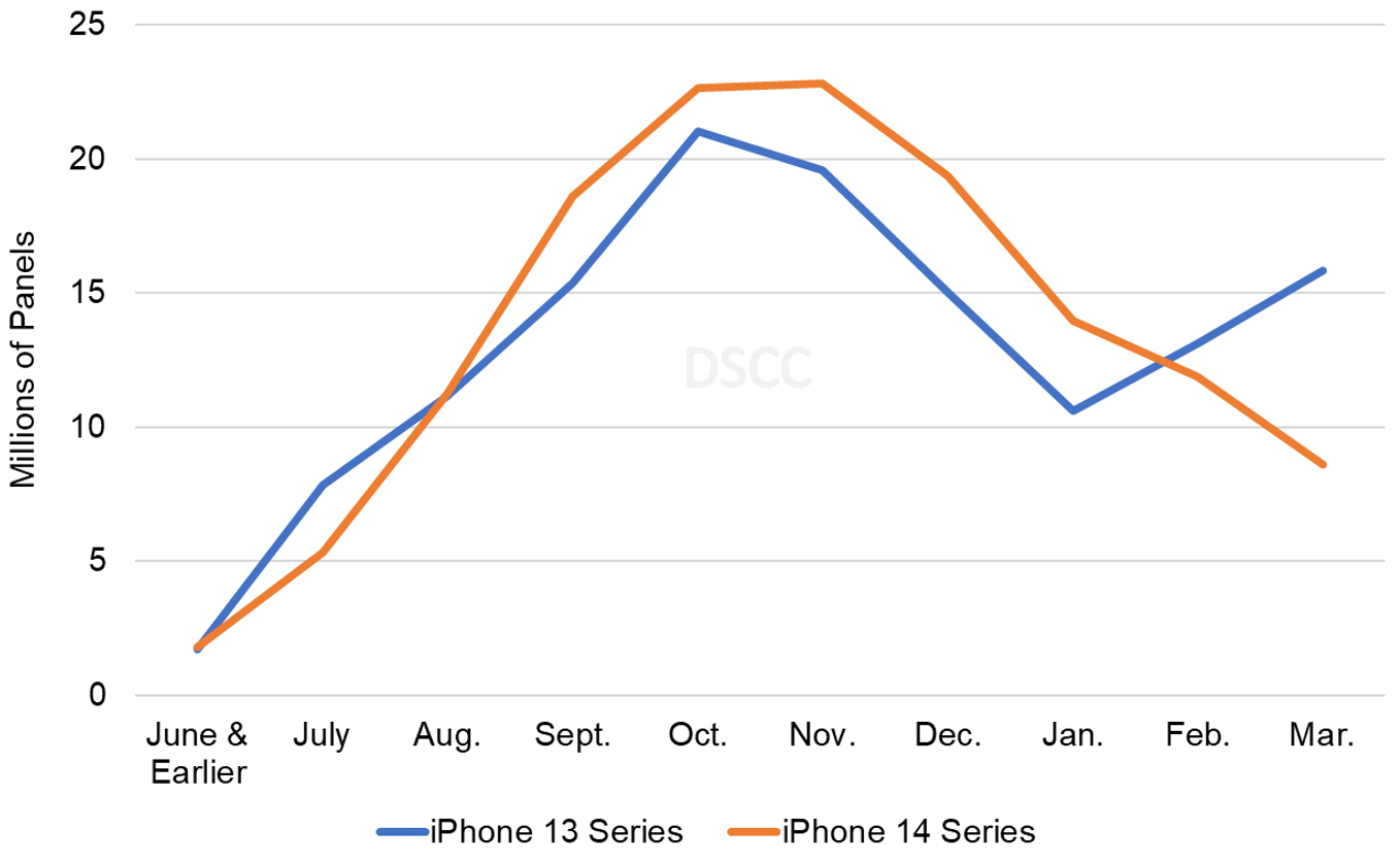

2月も終わろうとしているが、DSCCによる最新のサプライチェーンデータ調査によると、iPhone 14 シリーズ用パネル出荷数は、前年4月から3月までの同期間のiPhone13シリーズ用に比べて4%増であることが明らかになった。この低成長の要因としては、11月の工場閉鎖による影響、需要と在庫の調整、マクロ経済の逆風などが考えられる。

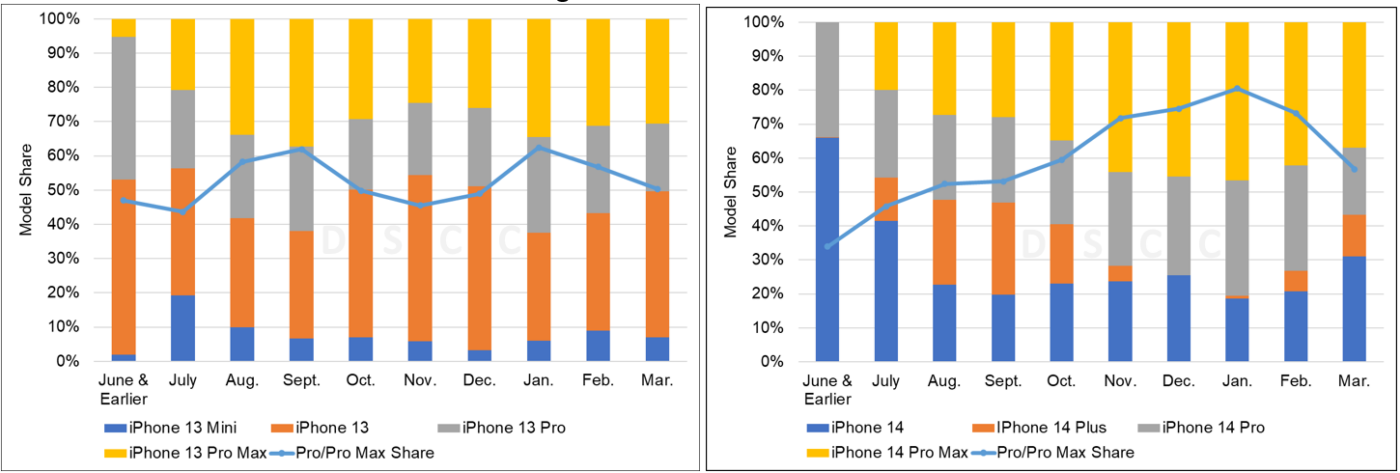

2022年のiPhone 14用パネルの合計出荷数は1億200万枚に到達、2021年のiPhone 13用パネル出荷と比較すると、前年比11%増となっている。モデル別シェアは、iPhone 14 Pro Maxが35%、iPhone 14 Proが 27%、iPhone 14が25%、iPhone 14 Plusが13%だった。Q1’23にはiPhone 14用パネル出荷数が3400万枚に達すると予想される。iPhone 14 Pro Maxがシェア43%で引き続きリード、iPhone 14 Proが29%、iPhone 14が22%、iPhone 14 Plusが6%となる見通しだ。

Monthly iPhone 14 Volumes Expected to Continue to Fall in March, LG Display Continues to Gain

※ご参考※ 無料翻訳ツール (DeepL)

As we approach the end of February, our latest survey of supply chain data shows that panel shipments for the iPhone 14 Series are tracking 4% higher than the iPhone 13 Series during the same time period of April – March. This slower growth is the result of aftershocks from factory closures in November, demand and inventory corrections and macroeconomic headwinds.

In 2022, total iPhone 14 panel shipments reached 102M panels, which represents a 11% Y/Y increase when compared to the iPhone 13 panel shipments for 2021. The iPhone 14 Pro Max had a 35% share, followed by the iPhone 14 Pro with 27%, the iPhone 14 with 25% and the iPhone 14 Plus with 13%. In Q1’23, iPhone 14 panel shipments are expected to reach 34M units, with the iPhone 14 Pro Max continuing to lead the lineup with a 43% share, followed by the iPhone 14 Pro with 29%, the iPhone 14 with 22% and the iPhone 14 Plus with 6%.

As Apple noted in their recent earnings call, supply is no longer an issue despite the factory shutdowns. The broader issue is the overall industry inventory corrections, continued macroeconomic headwinds, inflationary pressures and softening demand. As a result, we now see iPhone 14 Series panel shipments falling 35% in March, when compared to the iPhone 13 Series in the preceding year. March panel shipments are expected to be the lowest since August and the demand outlook remains weak based on Apple’s guidance that this quarter will be similar to the December quarter. The December quarter also benefited from an extra week.

Apple’s iPhone 14 Series vs. iPhone 13 Series Procurement Over 10 Months

The iPhone 14 Pro and iPhone 14 Pro Max continue to perform well versus the iPhone 13 Pro and iPhone 13 Pro Max. The cumulative share for iPhone 14 Pro models through March is expected to be 65% versus a 53% share for the iPhone 13 Pro models. As a result, total panel revenues are 9% higher and blended ASPs 5% higher for the iPhone 14 Series. Also of note, the Plus model has failed to capture share after replacing the Apple 13 Mini. Consumers have spoken with their wallets and are willing to pay the additional $200 for the higher resolution 48MP wide rear camera, Always on Display and a newer chipset for the 6.7” iPhone 14 Pro Max starting at $1099 versus the 6.7” iPhone 14 Plus starting at $899.

In comparing the iPhone 14 Series vs. the iPhone 13 Series through March, we see the following changes in panel shipments by model:

- iPhone 14: Down 37%;

- iPhone 14 Plus vs. iPhone 13 Mini: Up 59%;

- iPhone 14 Pro: Up 22%;

- iPhone 14 Pro Max: Up 31%.

iPhone 13 Series vs. iPhone 14 Series Mix through March 2022 vs. 2023

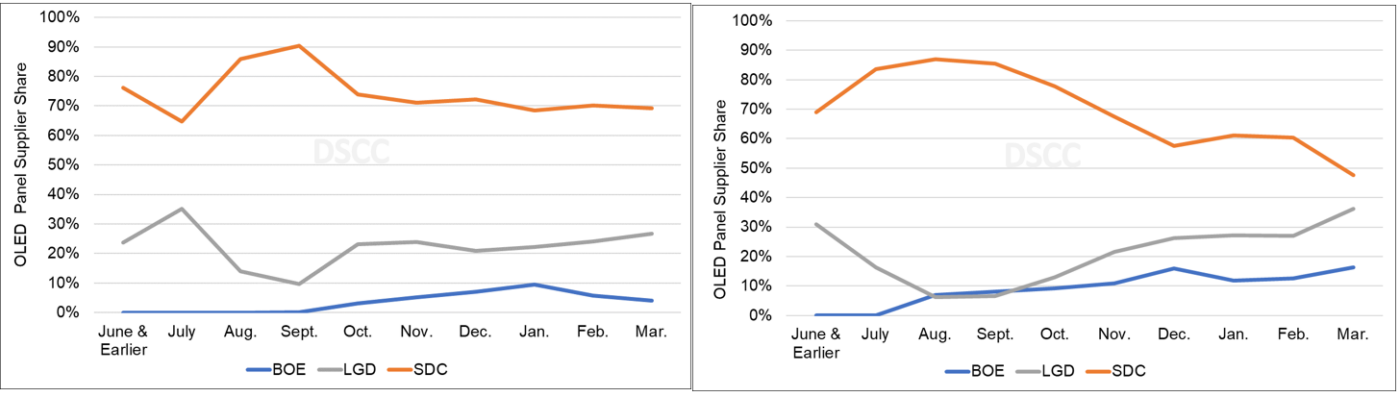

SDC continues to dominate Apple’s OLED business. SDC maintained a 74% cumulative share through December, but its share is expected to fall to 70% through March with LGD gaining share for seven straight months to reach a 36% share in March and a 19% cumulative share. A contributing factor to LGD’s continued share gain is the certification and availability of LTPO panels for the iPhone 14 Pro Max that started shipping in volume in October 2022. BOE is also taking share on the iPhone 14 model due to its aggressive panel prices versus both Korean suppliers. BOE’s share in March is expected to be 16% with a cumulative share of 11%. For the iPhone 13, BOE’s share was 4%.

iPhone 13 and 14 Shipment Share by OLED Panel Suppliers

This content is available for all flexible and foldable OLED smartphones sold to smartphone brands on a monthly basis including actual results and at least a two-month forecast. If interested, please contact お問い合わせ窓口. DSCC also provides quarterly panel shipments for all of the major smartphone brands along with detailed model specifications and trends in the Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします). This report includes all DSCC’s smartphone data from covering all OLED smartphone and panel shipments by brand, model, all display and major non-display parameters, panel and device revenues, regional forecasts for select models and forecasts by quarter and by year through 2027. In addition, it provides insights into technology and innovation trends in OLED display technology, which is applicable to smartphones. There are over 1,100 AMOLED smartphone configurations in our database including variations by substrate, TFT backplane, panel supplier, refresh rate, chipset supplier, design rules, 5G networks and much more. If interested, please contact お問い合わせ窓口.

本記事の関連調査レポート

Quarterly Advanced Smartphone Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。