Q4’22のOLED出荷速報&Q1'23の市況見通し~OLED調査レポート「速報版」より

冒頭部和訳

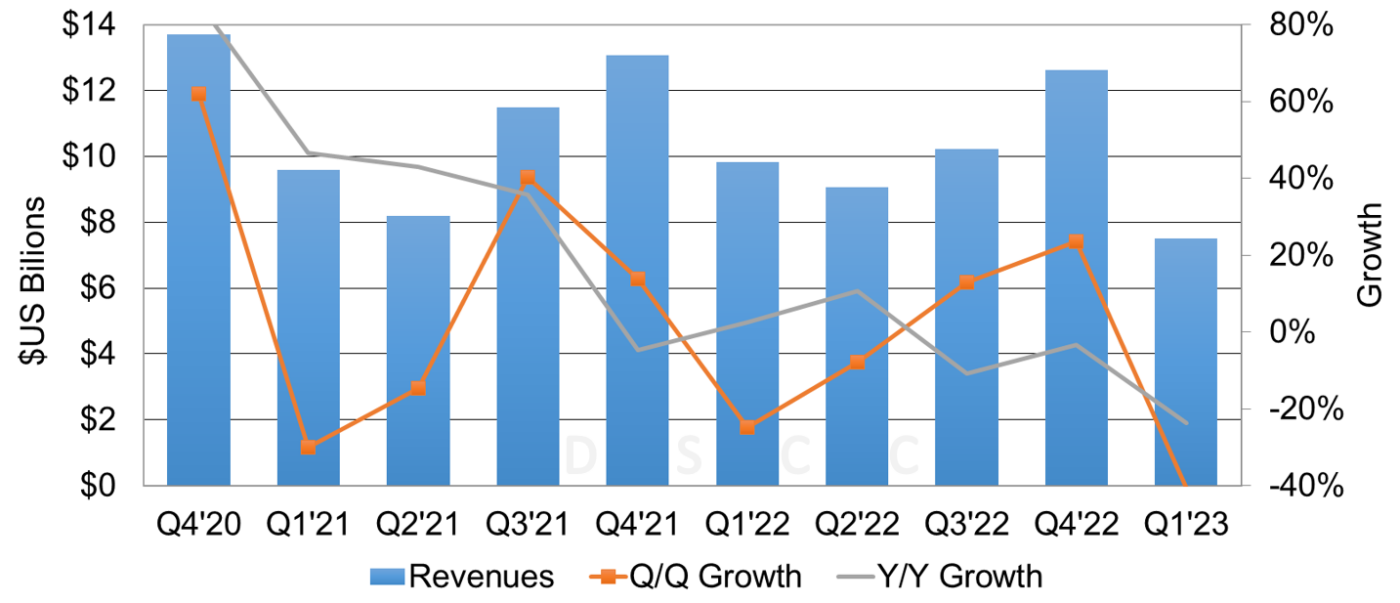

DSCCが Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) 最新刊の「速報版」を発行した。Q4’22のOLED出荷額は前年比3%減の126億ドル、出荷数は前年比7%減だった。

Q4'22におけるOLEDの用途別では、

・スマートフォン用は出荷数と出荷額ともに前年比3%増

・TV用は出荷数が前年比4%減、出荷額が前年比12%減となった。

2022年全体におけるOLED出荷額は前年比1%減の417億ドルで、用途別ではスマートフォン用が前年比1%減、TV用が前年比9%減という結果だった。2022年にはAR/VR、車載、モニター、タブレット、ゲーム端末など、複数のOLED用途がプラス成長を示した。詳細はレポートをご確認いただきたい。

Q1’23のOLED出荷額は、スマートフォン用とTV用の大幅な減少により、前年比24%減の75億ドルになると予測される。スマートフォン用は前年比21%減、TV用は前年比39%減、その他のカテゴリーも2桁減となる見通しだ。

OLED Revenues Fall 3% Y/Y in Q4’22

※ご参考※ 無料翻訳ツール (DeepL)

As revealed in DSCC’s latest release of the Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) - Flash Edition, OLED panel revenues decreased 3% Y/Y in Q4’22 to $12.6B as a result of a 7% Y/Y shipment decline.

In Q4’22, by select OLED applications:

- Smartphones increased 3% Y/Y in units and in revenues;

- TVs decreased 4% Y/Y in units and 12% in revenues.

For 2022, OLED panel revenues declined 1% Y/Y to $41.7B as a result of a 1% Y/Y decline for OLED smartphones and a 9% Y/Y decline for OLED TVs. Several OLED applications had growth in 2022. These included AR/VR, automotive, monitors, tablets and game platforms. Further details can be found in the report.

In Q1’23, we are estimating that OLED panel revenues will decline 24% Y/Y to $7.5B as a result of significant declines for OLED smartphones and OLED TVs. We expect panel revenues for OLED smartphones to decline 21% Y/Y and OLED TVs to decline 39% Y/Y as well as other categories declining by double-digits.

AMOLED Panel Revenue and Y/Y Growth

In Q4’22, smartphones remained the largest OLED application with an 82% unit and 81% panel revenue share, up from 68% and 74% respectively in Q3’22. This lift was the result of Q/Q unit growth for the majority of smartphone brands. Apple had 51% Q/Q growth fueled by the iPhone 14 Pro Max with 197% growth followed by the iPhone 14 Pro up 97% and the iPhone 14 up 83%. Some of the top Chinese brands also had triple-digit Q/Q growth. Oppo had 204% Q/Q growth fueled by the new A1 Pro series and GT Neo, followed by Xiaomi with 158% Q/Q growth fueled by the Mi13 and Redmi Note 12 series.

In Q1’23, we expect smartphones to continue with a >80% unit and revenue share as a result of weakening demand from other categories and the focus of brands to drive more flexible and foldable OLED smartphones during the traditionally slower selling season.

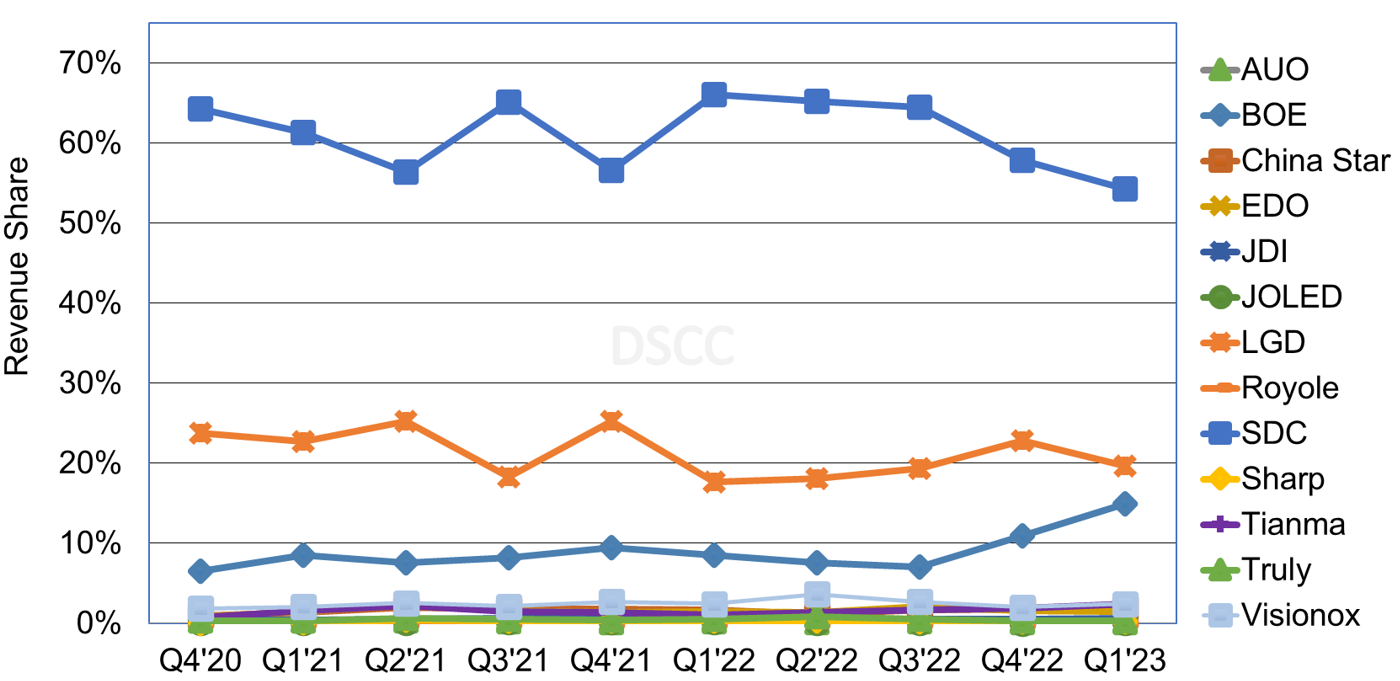

SDC continue to lead in OLED revenues with its share falling to 58% in Q4’22, down from 64% in Q3’22, followed by LGD with 23%, up from 19% in Q3’22 and BOE with 11%, up from 7% in Q3’22. For SDC, OLED smartphone units were up 30% Q/Q with significant growth for Apple, Xiaomi and other brands. For LGD, OLED smartphones units were up 140% Q/Q as a result of growth for Apple. For BOE, OLED smartphones were up 119% Q/Q as a result of growth for Apple, Honor and others.

In Q1’23, we expect SDC to continue to lead with a 54% revenue share helped by continued growth in tablets and monitors. We expect BOE to increase to a 15% revenue share on a smaller total market and a 22% Q/Q unit decline driven primarily by Q/Q declines for OLED smartphones. For LGD, we expect a 20% revenue share on a 57% Q/Q unit decline with OLED smartphones declining 41% Q/Q and OLED TVs declining 62% Q/Q.

AMOLED Panel Revenue by Panel Supplier

DSCC’s long-term forecast for OLED units, revenues, area, panel supplier share, form factor share, brand share, etc., will be available next month. For more information, please contact お問い合わせ窓口.

本記事の出典調査レポート

Quarterly OLED Shipment Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。