TV用LCD価格 (1月度分析)

冒頭部和訳

TV用LCD価格は2022年9月に底を打ち、第4四半期には価格が上昇したサイズもあったが、その上昇は長くは続かなかった。12月から1月にかけて価格に動きは見られず、こう着状態にあるようだ。ほとんどのサイズの価格は第4四半期に上昇したが、値上がり幅はわずかだった。LCD価格の下落スパイラルの最終段階では、FPDサプライチェーンにおける大幅な在庫減少と、それに対応するFPDメーカーの生産ライン稼働率の大幅な低下という特徴が見られた。

しかし、需要のシグナルは弱く、価格上昇は長く続かなかった。中国ではW11 (11月11日) / W12 (12月12日) 商戦の結果が期待外れに終わり、米国と欧州では需要が低調に推移している。中国では最近再び新型コロナ関連の混乱が見られ、中国の消費者が購買ムードに戻るかどうか、さらに疑問視されている。

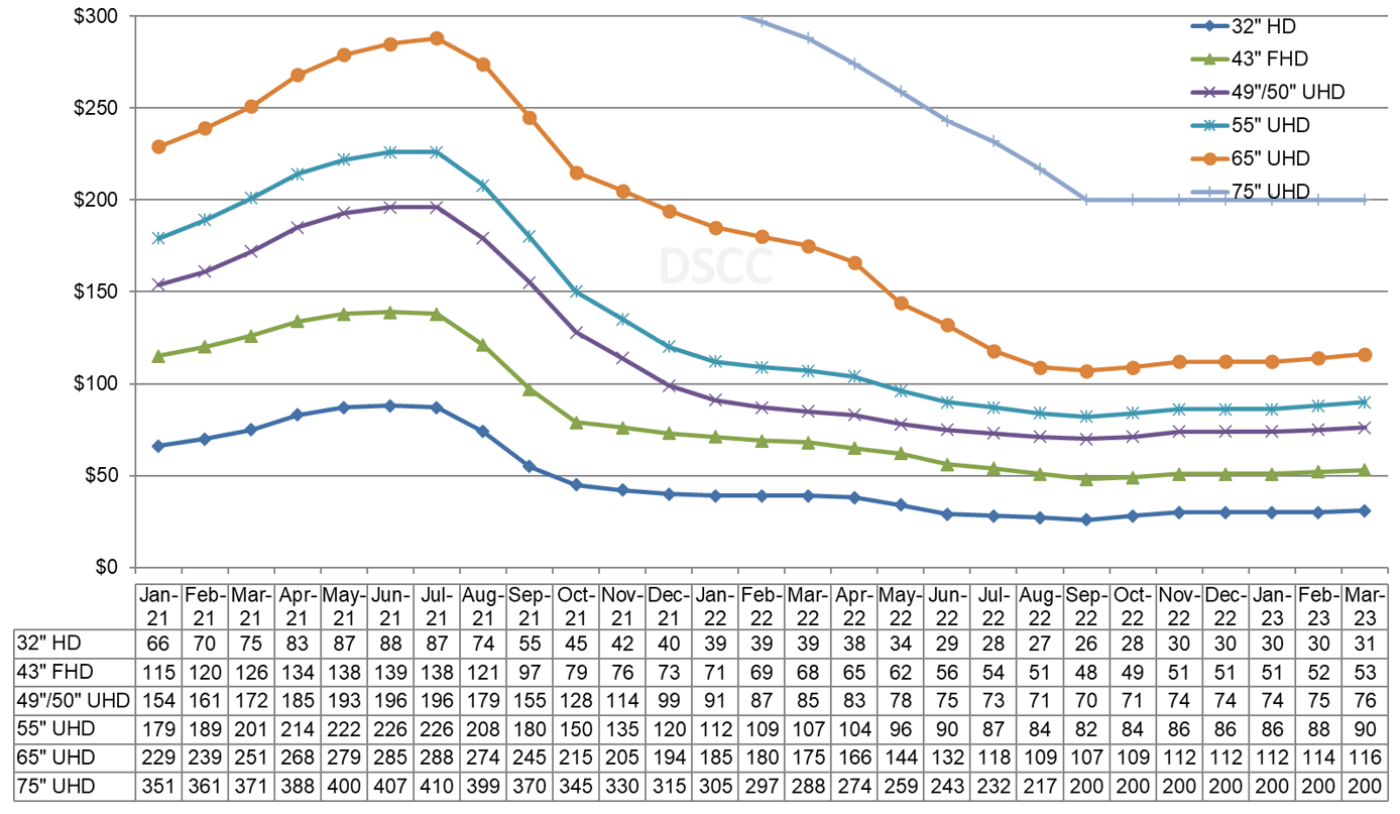

最初のグラフは、TV用LCD価格動向の最新予測だが、予測は先月から変わっていない。2020年中盤から2021年中盤までパンデミックによって価格は急騰、その後半部分がグラフに示されているが、2021年秋になると業界史上最も急速な価格下落が始まった。前月比平均価格下落率は3月の1.9%から6月の8.1%へと、第2四半期を通して毎月拡大し、その後、第3四半期は毎月4%から5%のペースを維持した。第2四半期の平均価格下落率は13.1%だったが、6月の大幅な価格下落によって、第3四半期の平均価格下落率は16.5%とさらに拡大した。

LCD TV Panel Prices in Holding Pattern

※ご参考※ 無料翻訳ツール (DeepL)

After LCD TV panel prices hit bottom in September 2022 and prices for several sizes increased in Q4, the rally in prices proved to be short-lived and prices appear to be in a holding pattern, with no changes in December or January. While prices for most sizes increased in Q4, the increase was modest. The last phase of the downward spiral in panel prices was characterized by a massive inventory drawdown in the display supply chain and a corresponding massive reduction in fab utilization by panel makers.

However, weak demand signals cut the price rally short. Disappointing results from the double 11 and double 12 shopping events in China have combined with continuing tepid demand in the US and Europe. The recent COVID-related disruptions in China cast further doubt that consumers there will return to a buying mood.

The first chart here highlights our latest TV panel price update, which is unchanged from last month, showing the latter part of pandemic-fed surge from mid-2020 to mid-2021 and then the fastest price decreases in the industry starting in the autumn of 2021. The average M/M price decline increased each month during the second quarter, from 1.9% in March to 8.1% in June, and then maintained a pace between 4% and 5% for each month in Q3. The average price decline in Q2 was 13.1%, but because of the big price drop in June, the average price decline in Q3 was even larger at 16.5%.

LCD TV Panel Prices

For the month of December, prices were unchanged for all six screen sizes that we track, following average price increases of 3.4% and 2.6% in November and October, respectively. The average price in December were 6.1% higher than in September, but because of the offsetting patterns in Q3 and Q4 (down during Q3 and up during Q4) the average price for Q4 increased only 0.5% over the average price in Q3.

We expect prices to remain unchanged again in January before beginning a slow increase for the balance of Q1’23 as the excess inventory in the display supply chain is finally drained out of the system. The slow increase applies for all screen sizes except 75”, for which we expect prices to remain flat. On average, we expect March prices to be 3.6% higher than December prices and expect Q1’23 prices to be 2.5% higher than Q4’22 prices.

As we look at pricing on an area basis, the larger screen sizes made efficiently on Gen 10.5 fabs, 65” and 75”, long enjoyed a significant price premium over smaller sizes, but the price premium for 65” was eliminated in Q2’22 and during the second half of 2022 the price premium for 75” panels eroded rapidly. The area premium for 75” is being further reduced in Q4’22 and Q1’23 as the prices for smaller sizes increase while 75” prices stay flat.

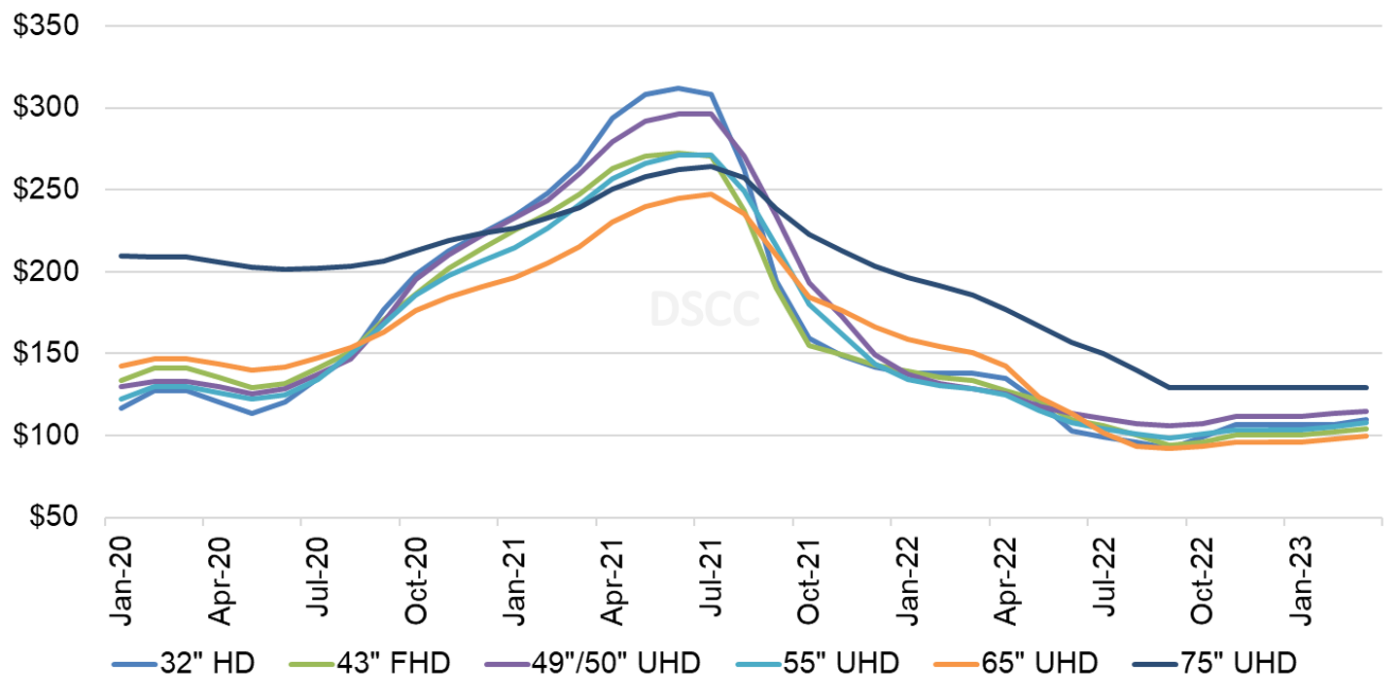

Monthly Area Prices per Square Meter for TV Panels

In June 2022, a 75” panel was priced at $144 per square meter, a $41 or 40% premium over the 32” area price. In September 2022 when the market hit bottom, the 75” premium over 32” had dropped to $37 but was still the same in percentage terms at 40%. While prices for 65” and smaller panels increased in October and November, 75” prices stayed flat, so the area premium of 75” panels over 32” has fallen to $23 or 21% in December, and we expect it to deteriorate further to $19 or 17% in March 2023.

As we expected, the lower panel prices and soft demand led to operating losses for panel makers relying on LCD production in Q3’22. The average operating margin across the flat panel display industry in Q3, excluding SDC, was a 13% loss. With panel prices increasing in the fourth quarter, it is possible that the results improved, but not by much. We will see earning results starting at the end of January.

While it appears that the worst may be over for panel prices, the industry’s capacity still far outstrips the likely demand for the foreseeable future. After the excess inventory has been removed from the display supply chain, we expect that the industry will recover to some extent, but we cannot say with confidence that panel prices will continue to increase.