フォルダブル型FPD調査レポートの分析ハイライト

途中部和訳

DSCCのCEOであるRoss Youngは次のように述べている。「Q4’22はiPhone 14シリーズが発売され市場を席巻、世界経済の低迷もあってフォルダブル市場は失速したが、スマートフォンとディスプレイ市場にとって展望が非常に明るい領域であることに変わりはなく、過去最高を記録しシェアを拡大しようとしている。また、Googleなど新規参入も見られ、既に参入済みの企業からもOppo Find N2およびFind N2 Flipなど新たなデバイスの発売が増えている。これにより競争が激化し、消費者に与えられる選択肢が増え、価格が引き下げられるはずだ。その結果、2023年の出荷数は33%成長の1700万台になるとDSCCでは予測している。Samsungのシェアは2021年の88%から2022年には78%、2023年には72%に低下すると見られる。3%以上のシェアを獲得するスマートフォンブランドは6社になると見られ、2023 年には中国からの新規参入を含む10ブランドがフォルダブルデバイスを出荷すると予測される。一方、Samsungのディスプレイ事業であるSamsung Displayに対しては他ブランドの依存度も高まっており、Samsung Displayのシェアは2022年の83%から2023年には88%に上昇する見通しだ。最大の競争相手はBOEだが、そのシェアは 12%から10%に下がると見られる。」

Q3’22 Foldable Market Reaches Record High, But Will Decline in Q4’22 on US Market Weakness as iPhone 14 Series Dominates

Although Q3’22 was a record quarter for foldable smartphone shipments, it won’t carry into Q4’22 with foldable phones suffering their first Y/Y decline according to DSCC’s Quarterly Foldable/Rollable Display Shipment and Technology Report (一部実データ付きサンプルをお送りします). What happened?

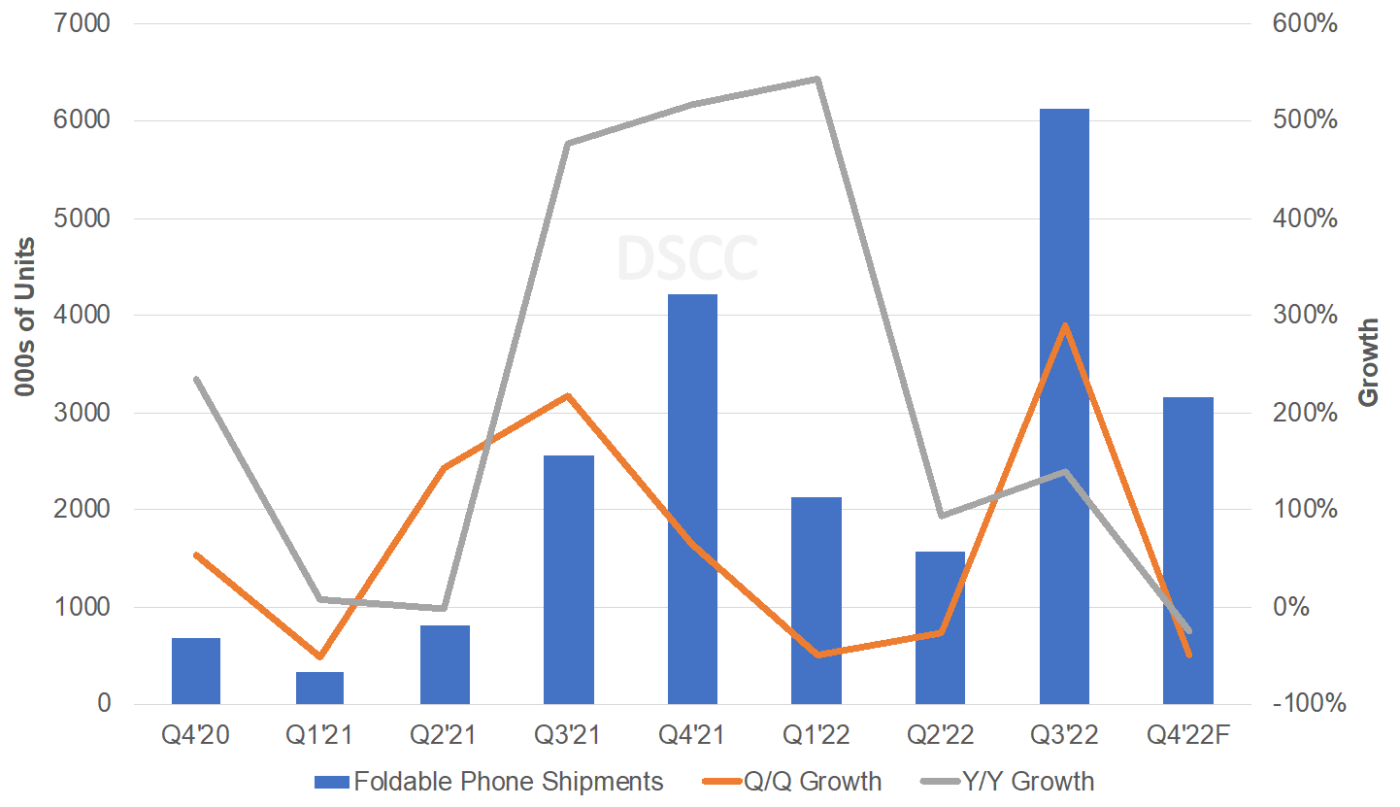

While Samsung’s Q3’22 foldable smartphone shipments were within 1% of expectations and the Korean giant dominated a record Q3’22 foldable smartphone market with an 85% share and 5.2M units on a sell-in basis, it lost its momentum in Q4’22 with its foldable smartphone shipments expected to fall 50% Q/Q and 36% Y/Y to 2.6M units with additional Q/Q declines expected in Q1’23 and Q2’23 and another Y/Y decline in Q1’23. Samsung’s share is only expected to fall to 82% in Q4’22, but the overall foldable smartphone market is expected to drop 48% Q/Q and 25% Y/Y to 3.2M units, its first ever decline on a Y/Y basis. Samsung’s share is expected to fall further in Q1’23 and Q2’23 and fall below 50% in Q2’23 on traditional seasonal weakness on the lack of new products while its competitors launch new devices.

Worldwide Foldable Smartphone Shipments

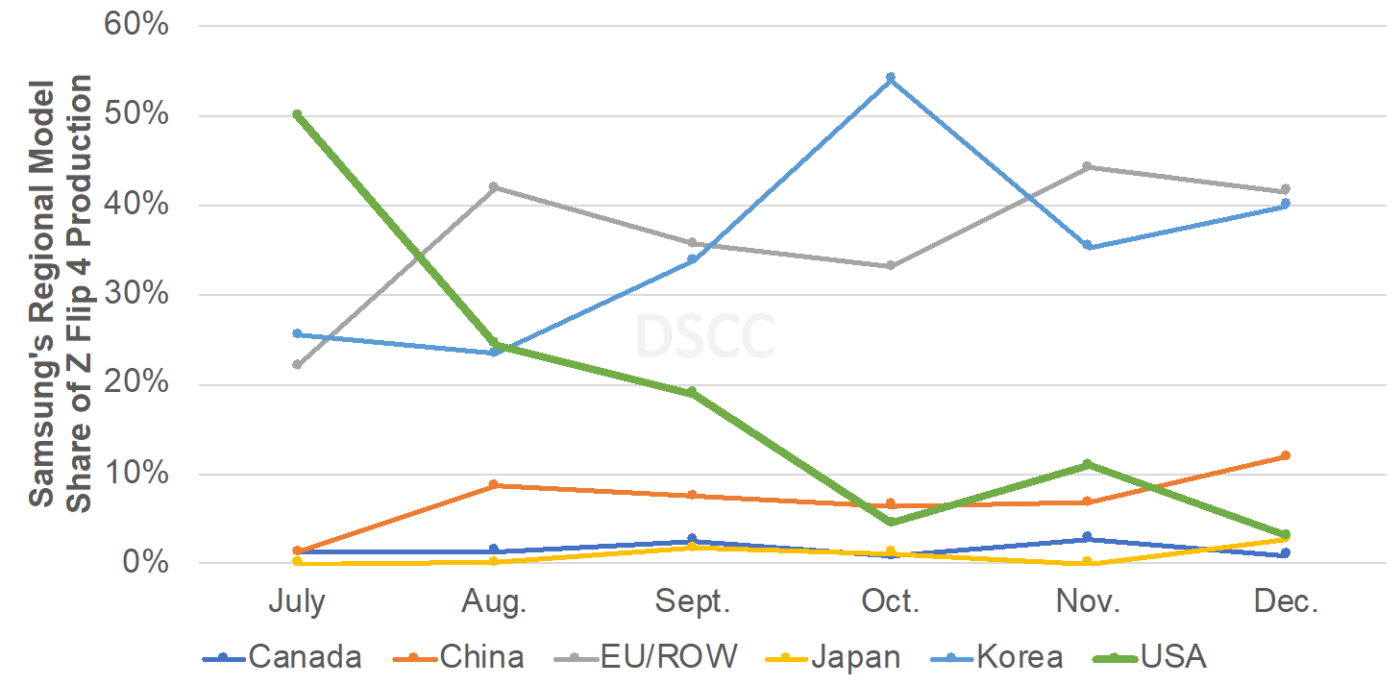

If we look at the regional segmentation, it becomes quite clear that the US market was the problem for Samsung in Q4’22 and it happens right after the iPhone 14 Pro Series launch with its improved cameras and Dynamic Island. While the US accounted for a 29% share of Samsung’s foldable smartphone production in 2021 and a 29% share in Q3’22, it plummeted to just 7% in Q4’22. The US accounted for just 5% of Samsung’s Flip-type phone production in Q4’22, down from 28% in Q3’22, and 11% of its Fold-type phone production, down from 32% in Q3’22. Furthermore, the drop started in October, the month after the iPhone 14 Series launch with the US falling from nearly a 20% share of Z Flip 4 production in September to just a 5% share in October and expected to be even lower in December. Furthermore, Z Flip 4 phone shipments fell behind the pace of Z Flip 3 shipments in October of the previous year and are expected to remain below the pace of previous year’s Z Flip 3 shipments through February. The situation is similar with the Z Fold 4. As a result, Samsung’s Q4’22 shipments are expected to be 45% below our previous forecast with its 2022 shipments up 46% to 10.1M units vs. previous expectations of 77% growth to 12.3M units. As a result of Samsung’s Q4’22 decline, the overall 2022 foldable smartphone market is expected to rise 64% to 13M units vs. previous expectations of 94% growth to 15M units.

Regional Model Share of Samsung’s 2022 Z Flip 4 Phone Production

According to DSCC CEO Ross Young, “While the foldable market stalled in Q4’22, due in part to being steamrolled by the iPhone 14 launch as well as the weak global economy, it is still very much a bright spot for the smartphone and display markets reaching new highs and gaining share. In addition, we are seeing new entrants such as Google and existing entrants bringing more devices to market such as the Oppo Find N2 and Find N2 Flip which should increase competition, give consumers more choice and bring down prices. As a result, we see 33% growth in 2023 to 17M units. Samsung’s share is expected to fall from 88% in 2021 to 78% in 2022 and 72% in 2023. Six different smartphone brands are expected to have at least a 3% share and we see 10 brands shipping foldable devices in 2023 including a new entrant from China. On the other hand, Samsung’s panel business, Samsung Display, is expected to gain share in 2023 as other brands increasingly rely on Samsung’s panel business rising from an 83% share in 2022 to 88% in 2023. BOE is the next closest supplier with its share expected to fall from 12% to 10%.”

For Q3’22, the Samsung Galaxy Z Flip 4 was the best seller with a 52% share followed by the Z Fold 4 at 27%, Huawei P50 Pocket at #3 with a 4.5% share and the Z Flip 3 #4 with a 4.5% share. In Q4’22, the Z Flip 4 is expected to lead followed by the Z Fold 4 with the Huawei Pocket S rising to #3 followed by the Z Flip 3 and P50 Pocket. In Q1’23, the Oppo Find N2 Flip is expected to rise to #4.

For monthly, quarterly and annual shipments on a foldable panel shipment, production and device shipment basis through 2023, as well as panel price and cost forecasts, company roadmaps, UTG developments, forecasts by feature and more, please learn about the Quarterly Display Supply Chain Financial Health Report online or contact お問い合わせ窓口.

本記事の出典調査レポート

Quarterly Foldable/Rollable Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。