TV用LCD価格、9月に底打ちQ4'22に反発

冒頭部和訳

15ヵ月間にわたる下落の後、TV用LCD価格は9月にようやく底を打ち、10月には価格が上昇したサイズもいくつか見られた。現時点の予測では、価格は年末にかけて緩やかに上昇し、Q1'23には史上最低価格より上のレベルで横ばいになる見通しだ。LCD価格の下落スパイラルの最終段階では、LCDサプライチェーンにおける在庫の大幅な取り崩しと、それに対応したLCDメーカーの生産ライン稼働率の大幅な低下という特徴が見られた。一部のLCDメーカーは価格が上昇するまで生産の再開を遅らせており、業界では価格がキャッシュコストレベルに向かってジリジリと上昇している。

価格の下落はQ2'22に加速しQ3'22も急速なペースで続いたが、Q4'22には大半のサイズのLCD価格が緩やかに上昇する見通しである。Q3'22のLCDメーカーとTVメーカーの決算発表によると、在庫は夏季の四半期に減少し、価格に対する下げ圧力もある程度取り除かれたようだ。

LCD TV Panel Prices Hit Bottom in September, Rebounding in Q4

After fifteen months of decreases, LCD TV panel prices finally hit bottom in September 2022 and prices for several sizes increased in October. We now expect to see a modest increase in prices through the end of the year with prices plateauing in the first quarter above their all-time lows. The last phase of the downward spiral in panel prices was characterized by a massive inventory drawdown in the display supply chain and a corresponding massive reduction in fab utilization by panel makers. With some panel makers delaying to resume production until prices increase, the industry has seen prices edge up toward cash cost levels.

Price declines accelerated in Q2 and continued at a rapid pace in Q3, but prices for most panel sizes will increase modestly in the fourth quarter. Based on panel maker and TV maker earnings reports for Q3, inventory decreased in the summer quarter, removing some of the downward pressure on prices.

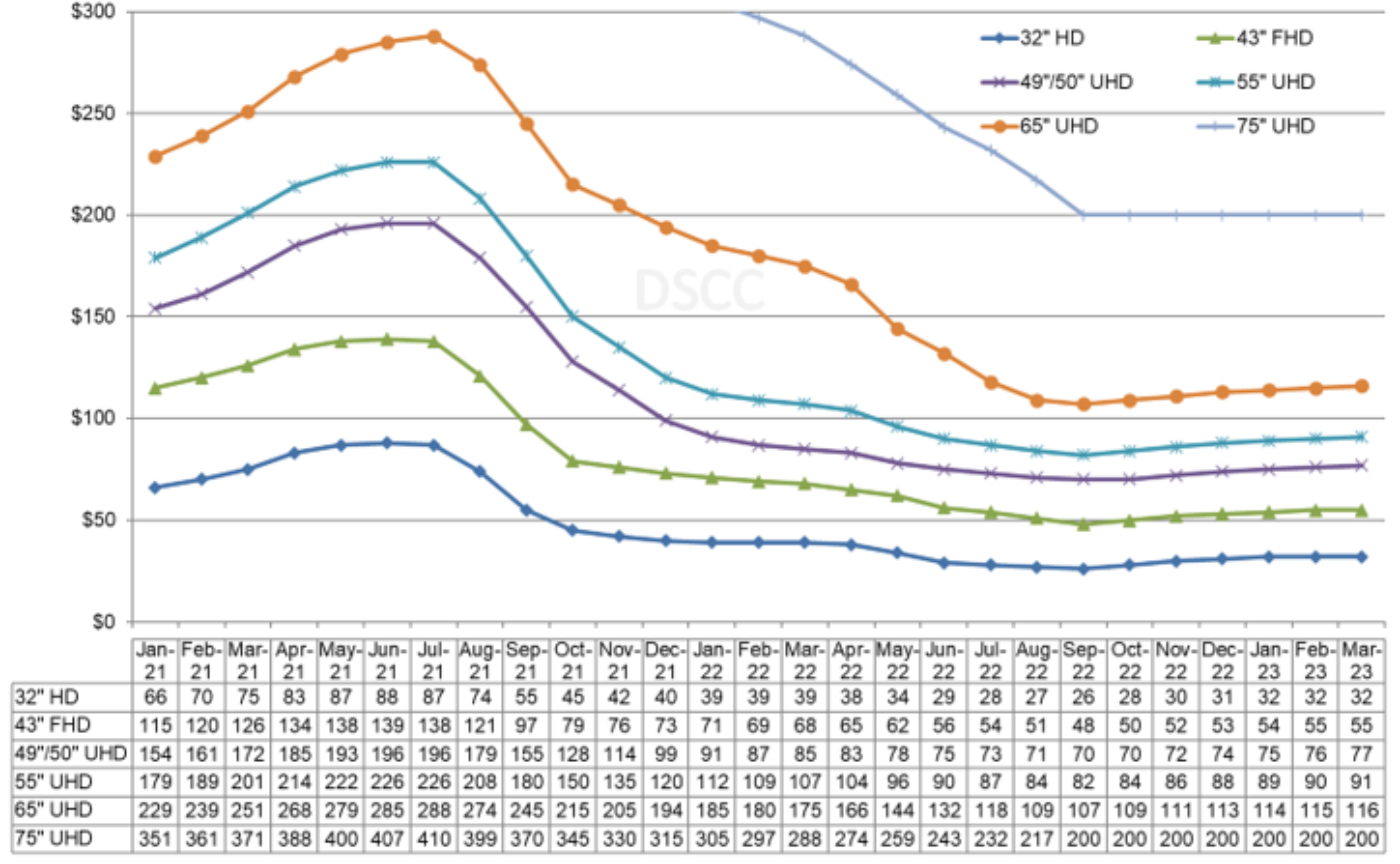

The first chart here highlights our latest TV panel price update, showing the latter part of pandemic-fed surge from mid-2020 to mid-2021 and then the fastest price decreases in the industry starting in the autumn of 2021. The average M/M price decline increased each month during the second quarter, from 1.9% in March to 8.1% in June, and then maintained a pace between 4% and 5% for each month in Q3. The average price decline in Q2 was 13.1%, but because of the big price drop in June, the average price decline in Q3 was even larger at 16.5%.

LCD TV Panel Prices

For the month of October, four of the seven sizes that we track saw price increases and the other three had flat prices, resulting in an average price increase of 2.3%. We expect similar small price increases in November and December, so that in December the average prices will be 8.5% higher than in September. Because of the offsetting patterns in Q3 and Q4 (down during Q3 and up during Q4) the average price over the quarter will increase only 0.7%, but the benefit of rising prices in Q4 means that the average price in Q1 will be 4.8% higher than Q4, even though we expect most prices to be close to flat in the first quarter.

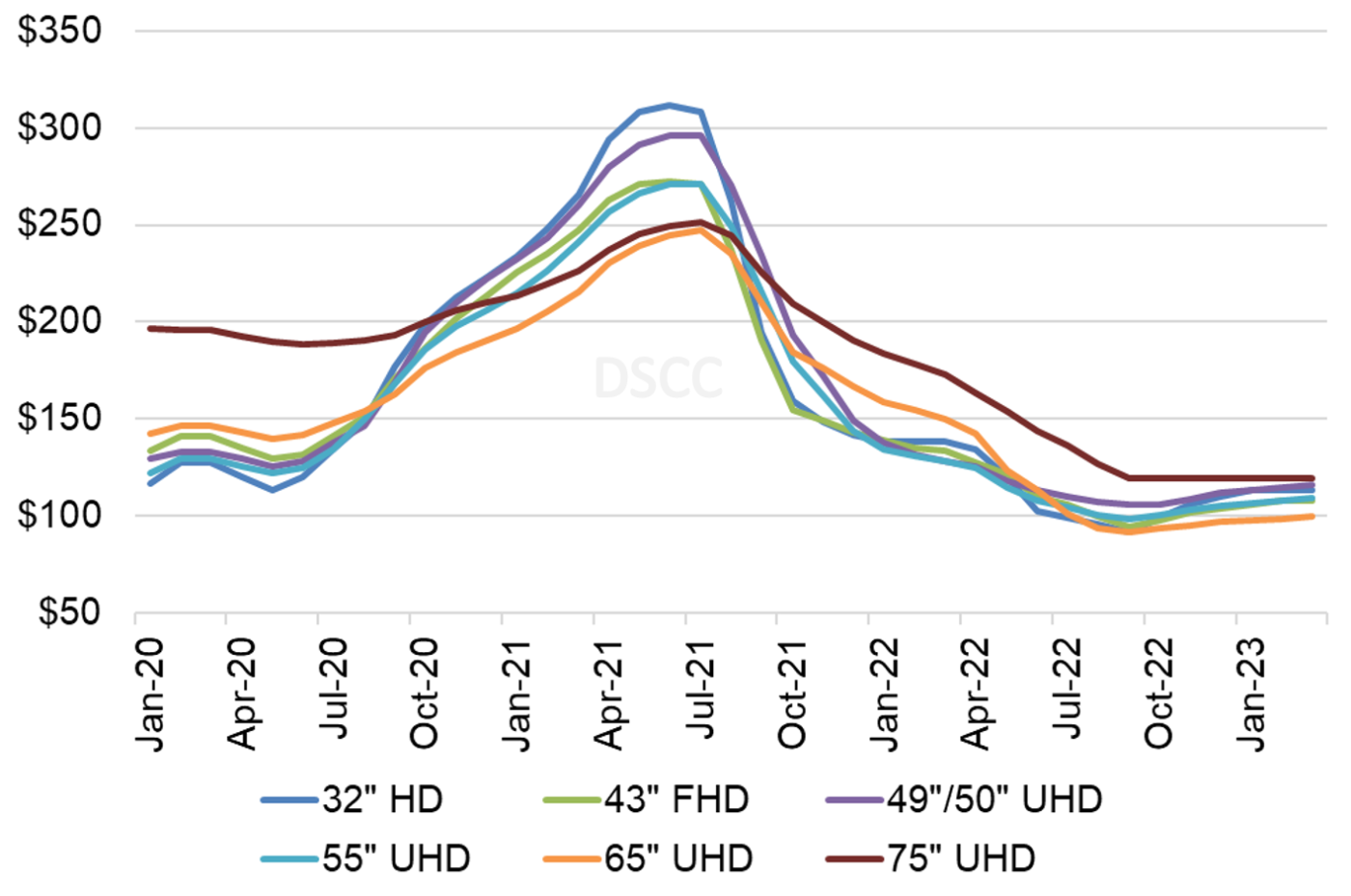

As we look at pricing on an area basis, the larger screen sizes made efficiently on Gen 10.5 fabs, 65” and 75”, long enjoyed a significant price premium over smaller sizes, but the price premium for 65” was eliminated in Q2 and in the second half of 2022 the price premium for 75” panels is eroding rapidly. In January 2022, the area price for 65” panels was 14% higher than the area price for 43” panels, but by June 2022, that premium dropped to zero.

Monthly Area Prices per Square Meter for TV Panels

In September, area prices for all screen sizes up to 65” fell in a range from $92 to $106 per square meter, with the 65” area price tied with 32” for the lowest in the industry at $92 per square meter. The largest screen size in our survey, 75” panels, continues to have a premium but that premium has eroded steadily. In June 2022, a 75” panel was priced at $144 per square meter, a $41 or 40% premium over the 32” area price. By September, the 75” premium over 32” had dropped to $27 and 29%. While prices for 65” and smaller panels increased in October, 75” prices stayed flat, and we expect that pattern to continue through Q4 and Q1.

Throughout the many cycles in the industry, we have seen that the most commoditized screen size is 32”, because this screen size can be efficiently produced on every Gen size fab from Gen 6 through Gen 10.5. Thus, when prices go down, 32” prices go down fastest, but when prices increase, the 32” price increase fastest as well. This was true in October as 32” prices increased by $2 or 7% for the month; the area price increased from $92 per square meter in September to $99 in October.

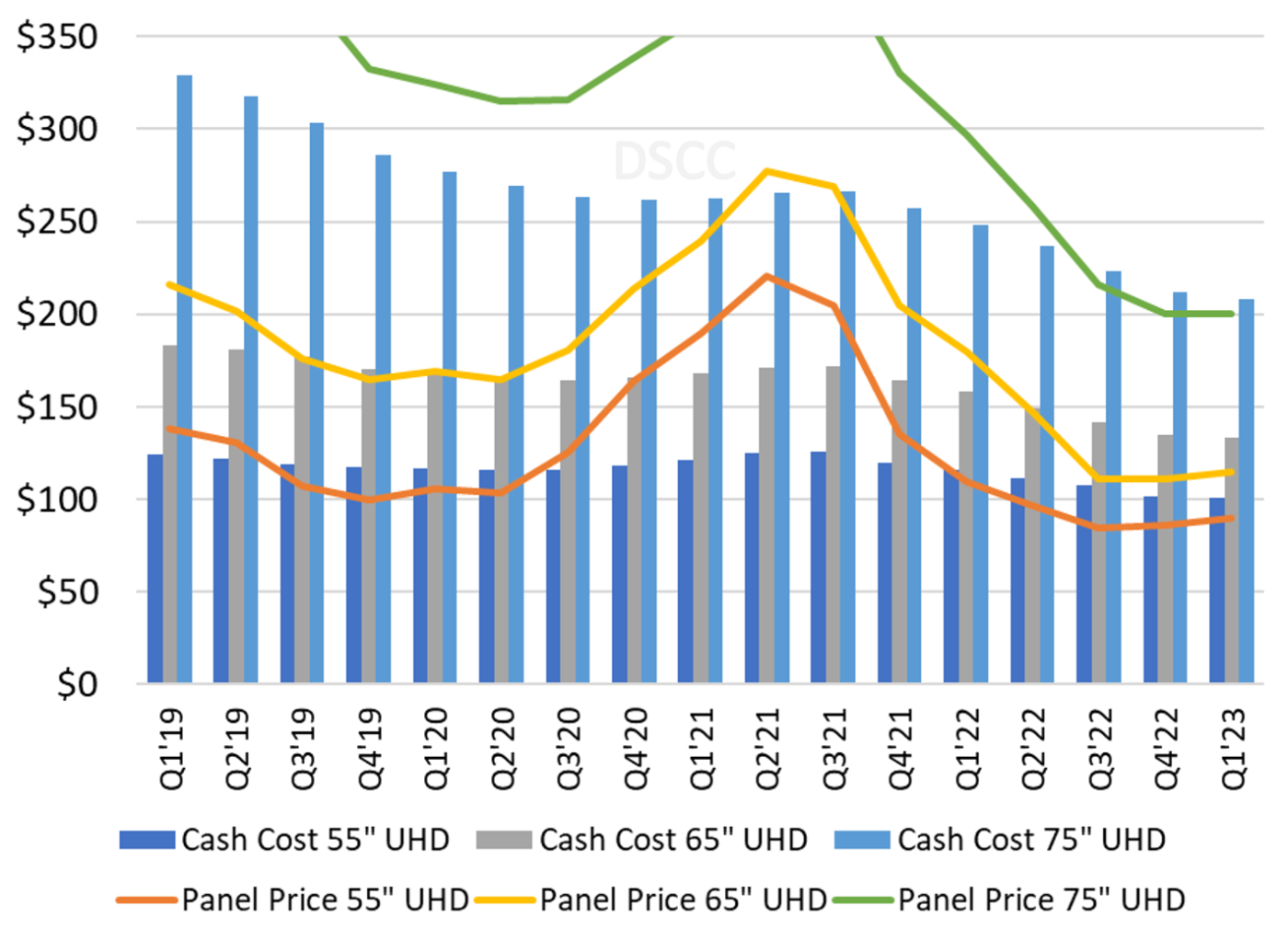

The next chart shows our estimates of cash costs vs. panel prices for large TV panels. While 55” panels have been below cash costs for most of the year, 65” prices reached cash costs in Q2 and for the first time 75” panel prices fell below cash costs in Q3. We expect that 55” and 65” panel prices will increase in Q4 and Q1 2023 but will remain slightly below cash costs.

LCD TV Panel Prices vs. Cash Costs

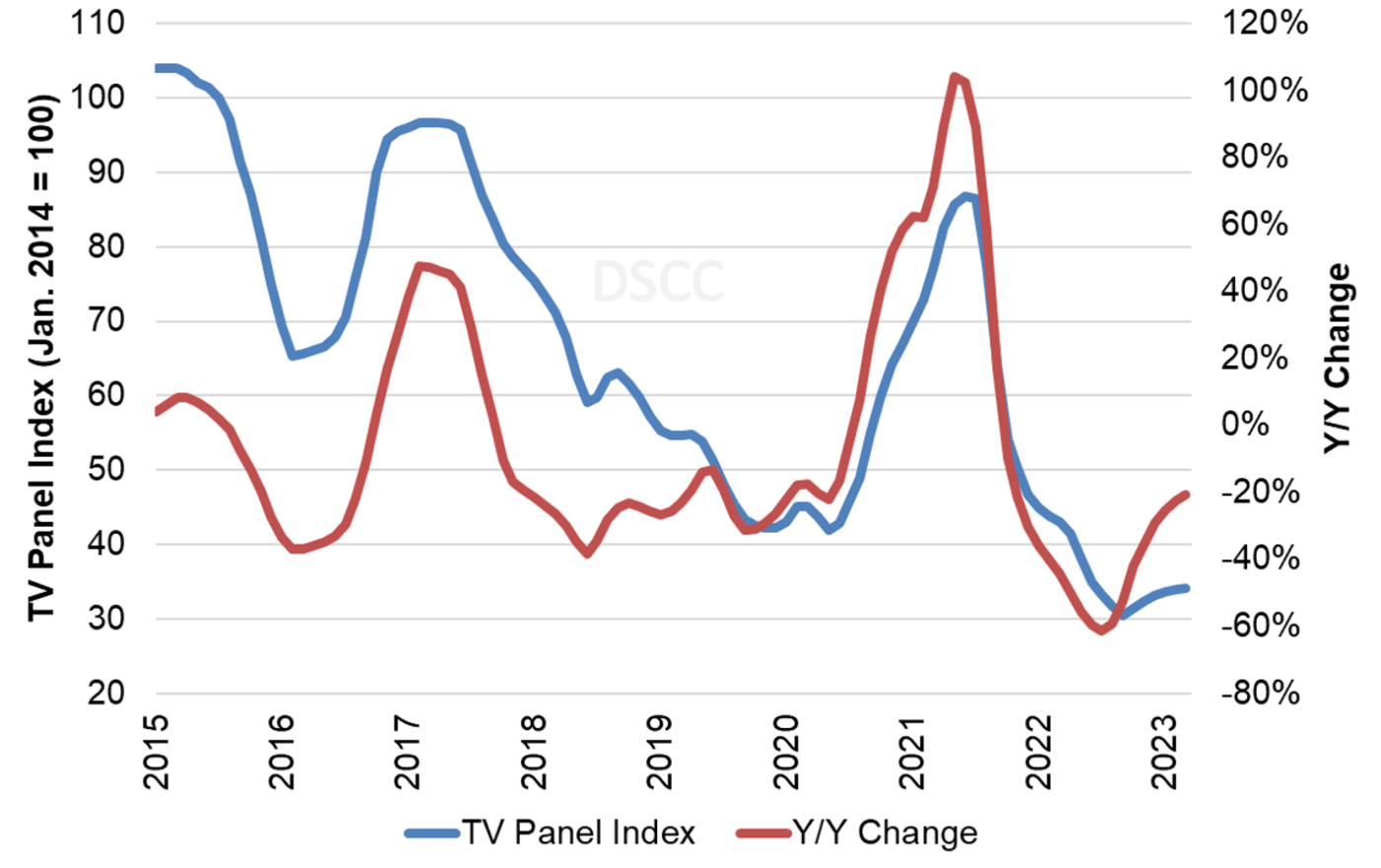

The last chart here shows our TV panel price index, set to 100 for prices in January 2014, and the Y/Y change of LCD TV panel prices. Our index increased from its all-time low of 42 in May 2020 to 87 in June 2021, but prices hit a new all-time low at 41.4 in April and have declined further to 30.5 in September. We now expect the index to rebound to 33.1 by December, 8% higher than the September 2022 nadir but 62% lower than the pandemic peak of June 2021.

TV Panel Price Index and Y/Y Change

As we expected, the lower panel prices and soft demand led to operating losses for panel makers relying on LCD production in Q3 2022. The average operating margin across the flat panel display industry in Q2 was 2%, down from 18% in Q2 2021, but excluding SDC, the operating margin of the industry was a 2% loss. With most companies reporting Q3 results, the average operating margin excluding SDC is -14%. With panel prices increasing in the fourth quarter, it is likely that the results will improve, but not by much.

While it appears that the worst may be over for panel prices, the industry’s capacity still far outstrips the likely demand for the foreseeable future. After the excess inventory has been removed from the display supply chain, the industry may recover to some extent, but we cannot say with confidence that panel prices will continue to increase. As the TV price index chart shows, In the long down-cycle from 2017 to 2020 there were several false recoveries before prices hit a bottom. Unless we see a significant demand driver emerge, the current increase in prices might follow a similar pattern.