ガラスメーカー第2四半期業績比較~FPD業界減速の影響は軽度

冒頭部和訳

2週間前、私たちはCorningの好調な第4四半期業績について取り上げた。本稿では、競合相手である日本企業2社、NEGとAGCを取り上げ、各社の業績を比較する。第2四半期にはFPDメーカーの稼働率低下の影響があったものの、ガラスメーカー3社はいずれも堅調な企業業績を示した。

Glassmakers Shrug Off Display Downturn in Q2

Two weeks ago, we covered Corning’s strong Q2 earnings release, and here we will cover its two Japanese competitors, NEG and AGC, and provide a comparison. All three glassmakers saw the impact of the slowdown of panel maker utilization in the second quarter, but all three showed robust corporate results, nevertheless.

NEG

NEG reported net income of JPY10.1B (US$ 78M) for Q2’22 on revenues of JPY86.8B ($669M). NEG’s revenues and net income soundly beat analysts’ consensus expectations of JPY80.4B and JPY6.5B, respectively. Revenues were up 1% Q/Q and 18% Y/Y, while net income was down 30% Q/Q but up 53% Y/Y in yen terms. NEG commented that although display glass sales were strong in the first quarter, sales were sluggish in the second quarter as customers adjusted inventory. NEG said that demand from home appliance, semiconductor and auto applications remained strong.

NEG does not report operating results of its separate businesses. However, it reports revenue for its electronics and information devices segment, including display glass and NEG’s Dinorex cover glass business, along with businesses for glass for optical and electronic devices. In Q2’22, E&I Device revenue declined 9% Q/Q but increased 3% Y/Y to JPY39.8B ($307M). Its non-display business, Performance Materials, saw revenues increase by 12% Q/Q and by 34% Y/Y.

For the second half of 2022, NEG implied that the downturn would continue, saying that it is expected to take some time for capacity utilization rates to recover. NEG did not revise its forecast for 2022 revenues and net income. NEG expects full year revenues of JPY 330B and net income of JPY 30B, which implies second half revenues and net income of JPY 157B and JPY 5.4B, respectively.

AGC

AGC benefited from strong demand and rising prices in its chemical business segment to improved profits in Q2’2. AGC’s display glass business saw reduced revenue and sharply reduced profit but AGC saw a recovery in its Glass business, which covers architectural and automotive glass.

AGC reported a net profit of JPY53B ($408M) on revenues of JPY506B ($3.9B) in Q2. Revenues increased by 7% Q/Q and by 21% Y/Y and net income increased by 26% Q/Q and by 20% Y/Y. Revenues and net income beat consensus analyst expectations of JPY492B and JPY26.6B, respectively.

AGC’s Electronics segment recorded operating income of JPY1.2B ($9M) on revenues of JPY72.1B ($555M). The electronics segment includes a display subsegment that incorporates both display glass and AGC’s Dragontrail cover glass business and another segment for electronic materials. Electronics revenue decreased by 5% Q/Q but increased by 2% Y/Y. Within the electronics segment, AGC’s electronics materials revenues decreased by 3% Q/Q but increased by 15% Y/Y, while revenues from display decreased 7% Q/Q and by 2% Y/Y at JPY42B ($323M). AGC does not report operating income for its subsegments, but Electronics operating income fell 85% Q/Q and 78% Y/Y.

AGC noted that shipments for both LCD glass substrates and specialty cover glass decreased Y/Y and operating profits declined because of higher depreciation expenses from its new Gen 10.5 facility in China, and manufacturing costs increased, affected by foreign exchange fluctuations. As AGC brought its Gen 10.5 facility online in 2021, its depreciation costs in Electronics increased from JPY47.9B in 2020 to JPY61.1B in 2021.

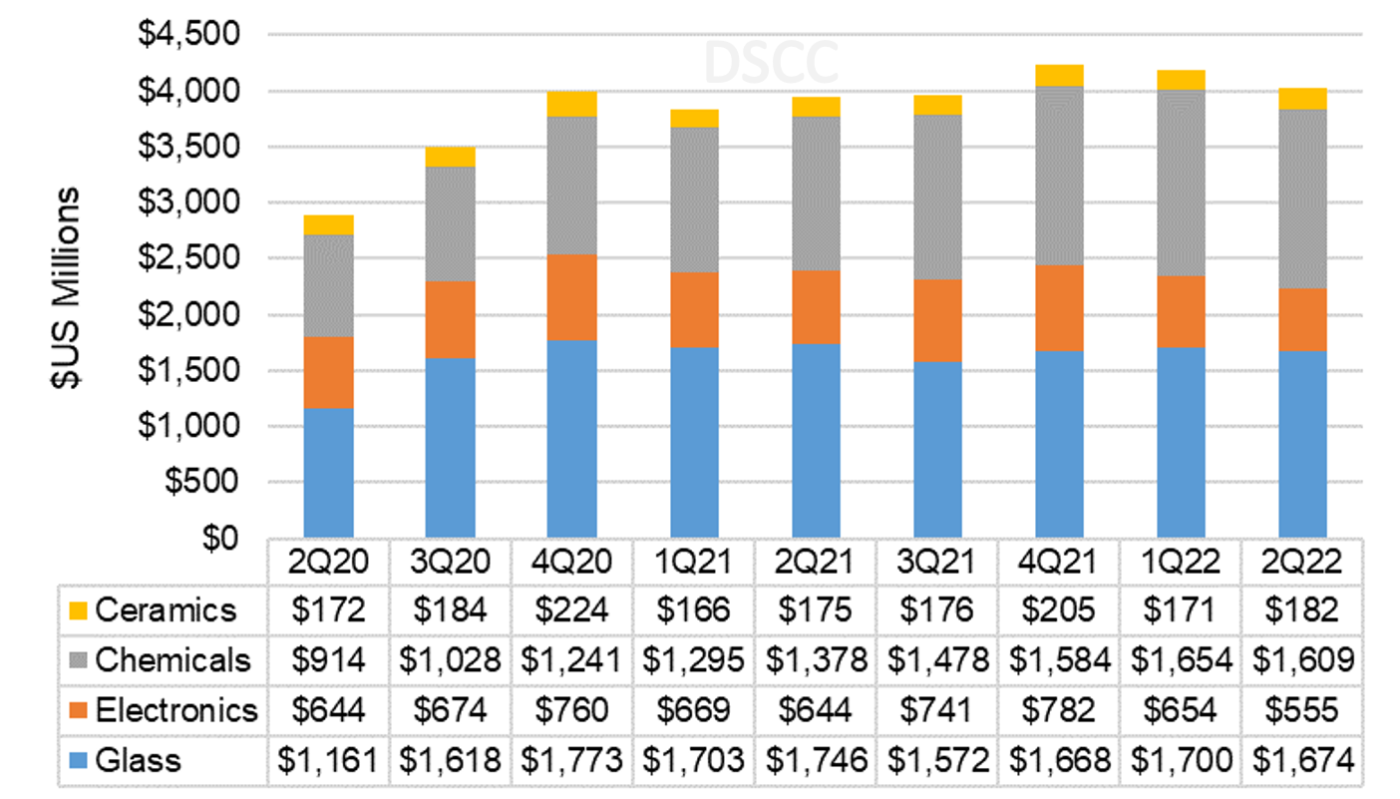

AGC Quarterly Revenue by Business Segment

Among AGC’s other business segments, its chemicals business in Q2 reported a 24% increase in revenues Y/Y and a 39% increase Y/Y in operating profit. AGC highlighted the strength of its chlor-alkali business in Southeast Asia driving the revenue and profit growth.

AGC revised its full year forecast for 2022, expecting higher revenue and profits but not from the display business.

AGC expects total corporate revenues to increase by 21% Y/Y to JPY2.05T (was JPY 1.8T) and operating profit to increase 12% to JPY230B (was JPY 2.17B). The upward revision in revenues and profits came from a positive outlook for its Chemicals and Glass businesses, offsetting weaker performance in its Electronics business. AGC expects Electronics revenues to increase 8% to JPY330B (was JPY 345B) and operating profits to decrease by 18% to JPY30B (was JPY 42B). Although AGC did not give a revenue or profit forecast for its Display subsegment, it expressed concern about LCD panel production adjustments and cited higher fuel and raw material prices and yen depreciation causing the reduced profit outlook

AGC continues to provide investors with updates on its medium- and long-term strategy, including details of revenues from strategic businesses, which does not include display. AGC expects growth in its strategic businesses and targets those for investment, while it expects core businesses to generate cash. In support of the strategy, AGC included a table of return on capital employed (ROCE) by business segment for 2020 and 2021. AGC’s Electronics segment achieved ROCE of 5.8%, well below the corporate average of 10.8% and lagging its Chemical segment at 21.5% and Ceramics at 14.0%.

Glass Maker Comparison

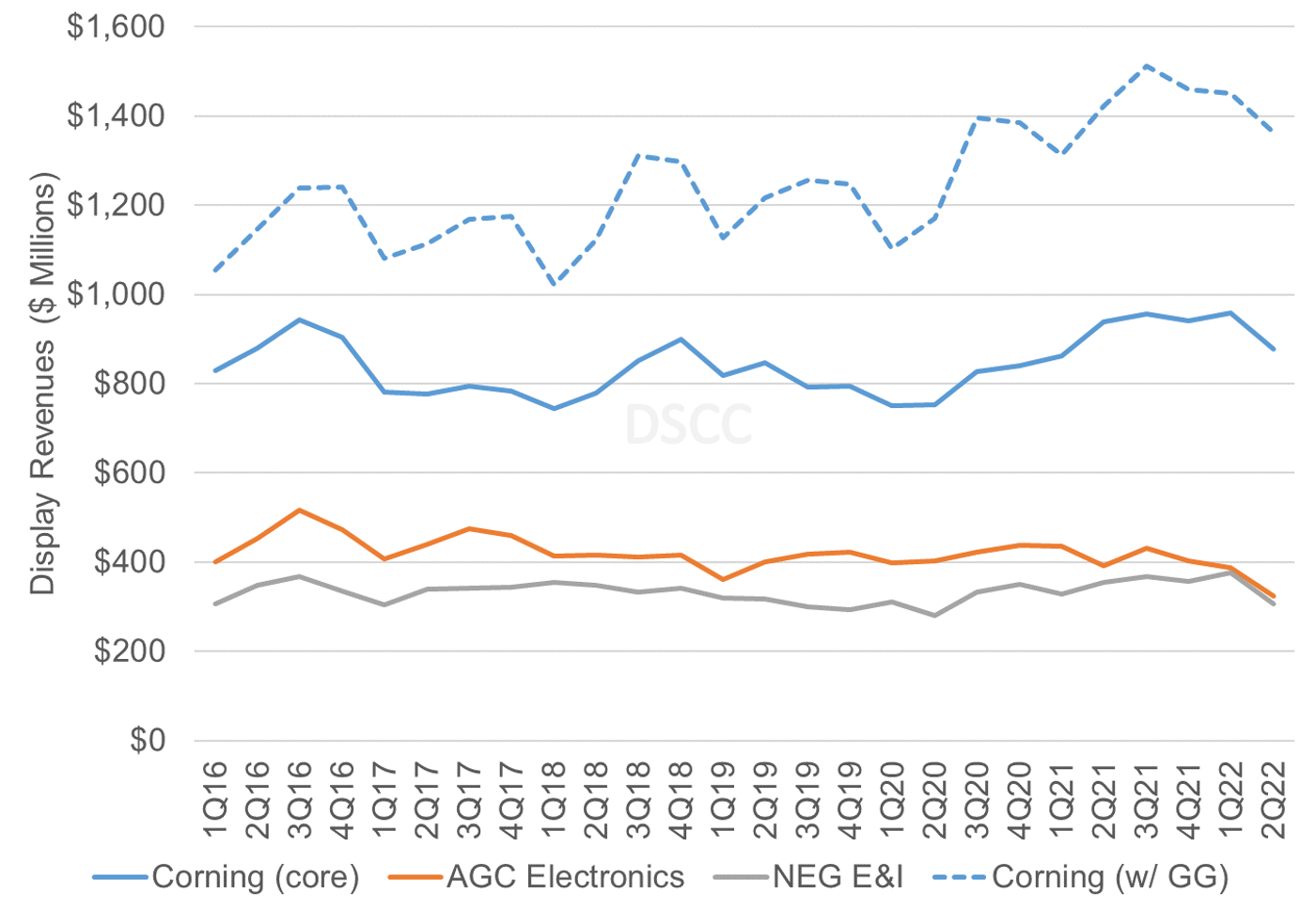

With financial results for the top three glassmakers, we can give a comparison of their results. Since the two Japanese companies include cover glass in their display-related business segments, it makes sense to compare the combination of Corning’s display technologies and specialty materials (Gorilla Glass) businesses, as shown in the chart here.

Glass Maker Revenues from Display Business Segments

Corning’s combined revenue captured 68% of total industry revenues in Q2’22, up 3% from both Q2 2021 and Q1’22. AGC share decreased from 18% to 16%, while NEG share decreased from 16% to 15%. With the sharp reduction in profits in AGC’s Electronics segment, Corning’s share of operating profits increased from 70% in Q1 to 82% in Q2, while AGC’s share decreased from 9% to 1% and NEG’s share fell from 20% to 17%.

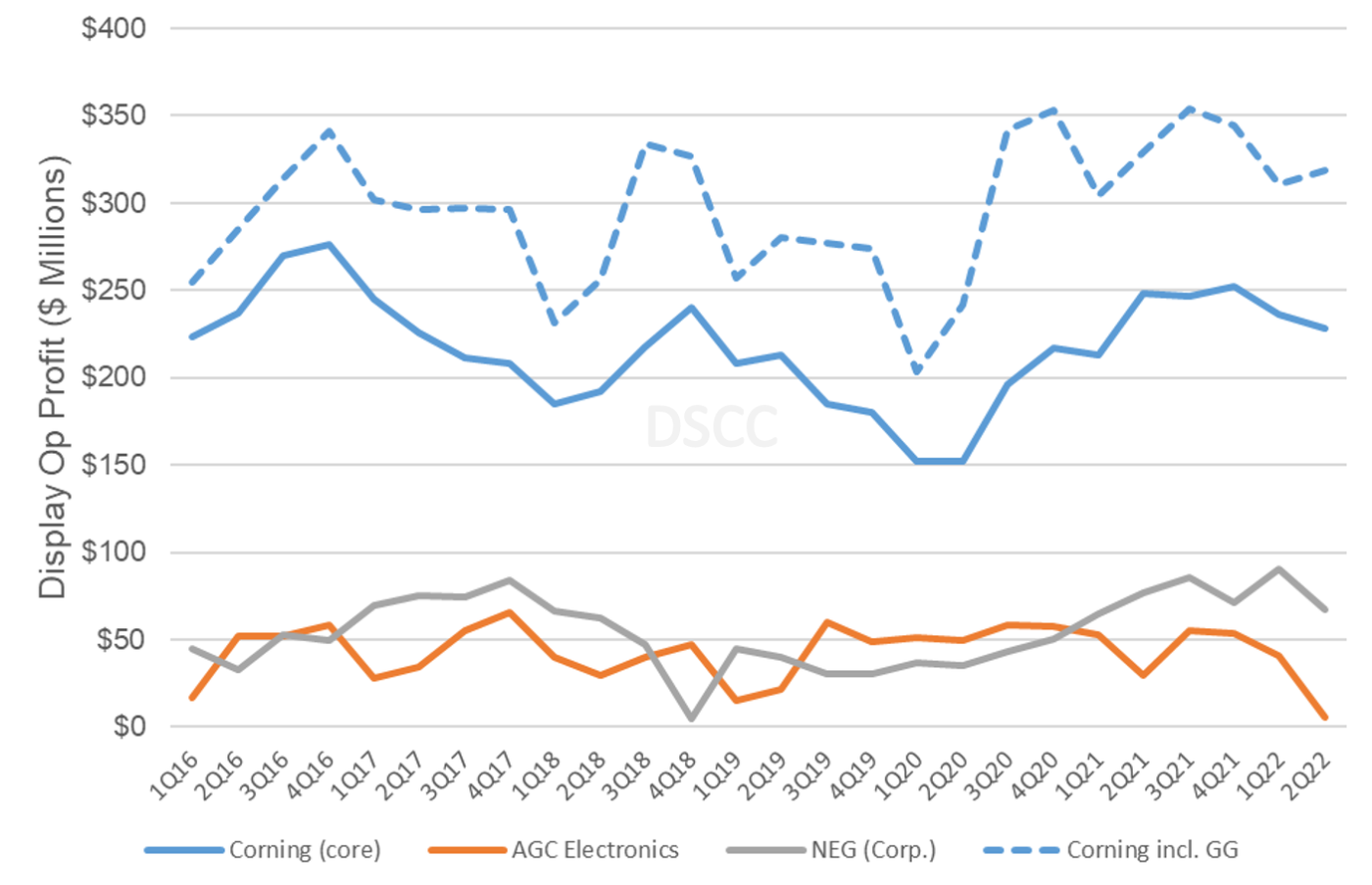

Glass Maker Operating Profits from Display Business Segments

With display glass prices (remember, glass is priced in JPY) increasing in 2021 and holding steady in 2022 but volumes declining in the second quarter, Corning’s profit margin held up but its Japanese competitors saw reduced margins. Corning’s operating margin for display including Gorilla Glass increased from 25% in Q1’22 to 26% in Q2’22, holding steady on a Y/Y basis. While NEG does not break out profit for its business segments, its corporate operating profit margin fell slightly to 11% in Q2’22 from 12% in Q1’22 and 13% a year ago. AGC’s operating margin for Electronics fell sharply from 11% in Q1’22 to only 2% in Q2’22, and that compares with 8% in Q2’21. AGC has stated that within Electronics, AGC’s margin for Display is lower than its margin for Electronics Materials.

In various ways, all three companies acknowledged the slowdown in display utilization which will affect second half results. While the two Japanese companies did not comment on glass prices, they appear to be accepting Corning’s leadership on prices. Corning had commented in its earnings call that glass prices in Q3 2022 are expected to be flat sequentially. The reduced profitability of the two Japanese glassmakers, reinforced by comments about rising costs and higher material prices, suggest that they are not in a position to be aggressive on pricing.

DSCC estimates that glass prices increased by 6% during 2021 in terms of Japanese yen, but this represented a 3% decrease in prices when expressed in US dollars because the yen depreciated by 9% during 2021. That discrepancy has accelerated in 2022 as glass prices have been flat through the first half, but the yen has depreciated by 14%. So, while prices have been flat to glassmakers, to panel makers the costs for glass have decreased by a double-digit % in the first half, helping to alleviate some of the pain of lower LCD panel prices for panel makers.

Even with stable prices (in yen), the display glass business looks headed for a sharp downturn in the second half of 2022. For the three big glassmakers who have all successfully nurtured non-display businesses the downturn is unfortunate but only a speed bump.