2022年のOLEDスマホ出荷金額は前年比16%減見通し~マクロ経済環境と消費者需要の弱体化が要因

冒頭部和訳

DSCCが最近発刊した Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) では、2022年のOLEDスマートフォン出荷金額は前年比16%減の3170億ドルになると予測しており、その要因として、マクロ経済の逆風、消費者需要の冷え込み、中国におけるCOVID-19の封鎖措置によって長引くサプライチェーン問題、在庫製品の蓄積に関する懸念を挙げている。サプライチェーンの情報源によると、主要スマートフォンブランドはいずれも2022年になってスマートフォン用OLEDの調達を1桁または2桁の割合で減らしているという。

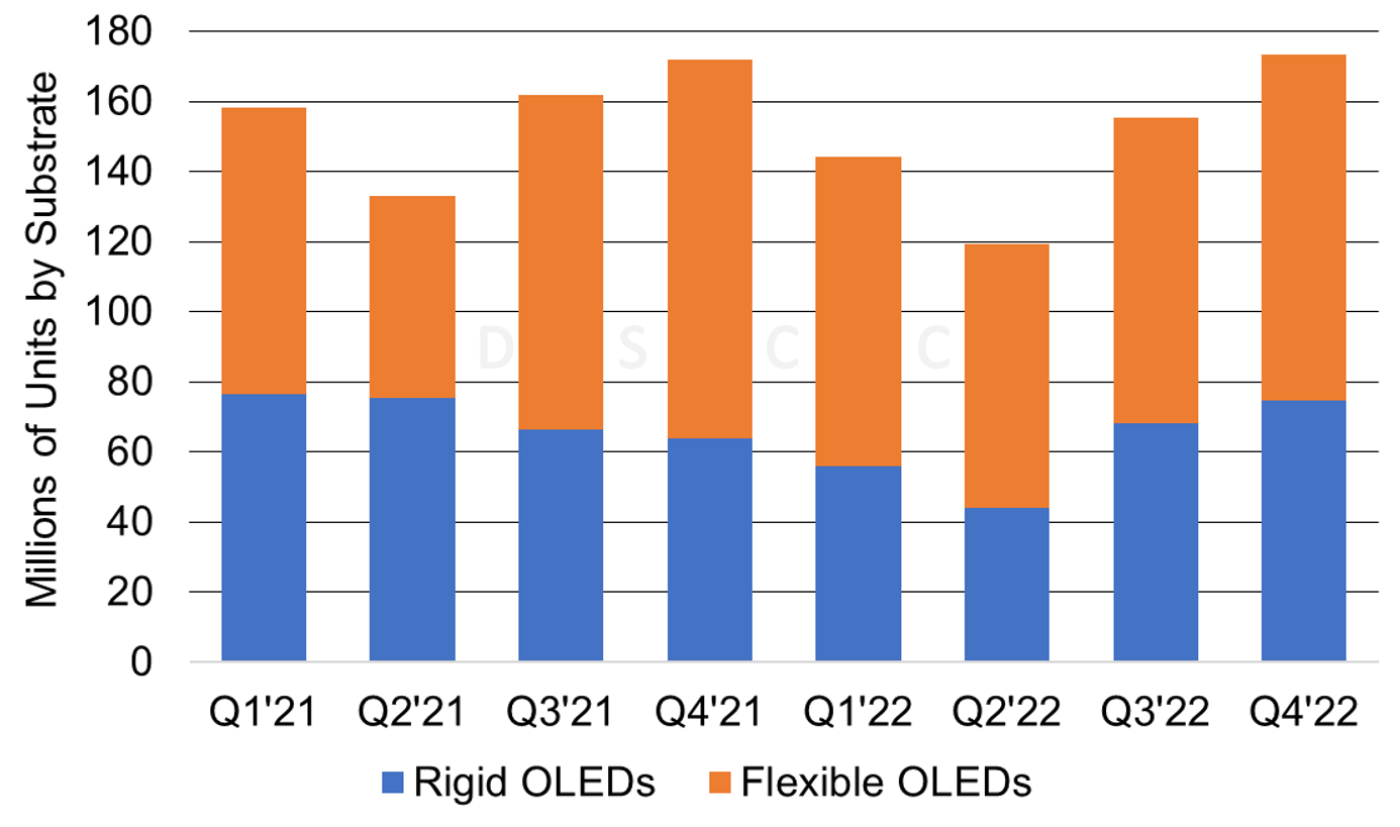

Q2'22については、スマートフォン用OLEDの出荷枚数が前期比17%減・前年比10%減の1億1900万枚、出荷金額が前期比23%減・前年比17%減の630億ドルになると予測される。基板別では、スマートフォン用リジッドOLEDが前期比21%減・前年比42%減、スマートフォン用フレキシブルOLEDが前期比15%減・前年比30%増という予測である。

2022年については、スマートフォン用OLEDの出荷枚数が前年比5%減の5億9200万枚になると予測される。スマートフォン用フレキシブルOLEDは前年比2%増で、数量ベースのシェアは2021年の55%から59%に上昇すると見られている。スマートフォン用リジッドOLEDは前年比14%減で、数量ベースのシェアは2021年の45%から41%に低下すると見られる。

スマートフォンの出荷金額については、リジッドOLEDスマートフォンの出荷金額は前年比32%減で、金額ベースのシェアは2021年の26%から21%に低下すると見られる。フレキシブルAMOLEDスマートフォンの出荷金額は前年比10%減で、金額ベースのシェアは2021年の74%から79%に上昇する見通しである。

2022年OLED調達量の最新推計に基づくと、ブランド各社のスマートフォン用リジッドOLED調達量は以前の推計より10-34%減となっている。スマートフォン用フレキシブルOLEDの場合、ブランド各社の調達量は以前の推計より2-51%減となる。

OLED Smartphone Revenue to Decline 16% in 2022 on Macroeconomic Environment and Weakened Consumer Demand

In the recently released Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします), we reveal that 2022 OLED smartphone revenue is expected to decline 16% Y/Y to $317B as a result of the macroeconomic headwinds, weakened consumer demand, persistent supply chain issues as a result of COVID-19 lockdowns in China and concerns regarding inventory product build up. Based on our supply chain sources, all of the major smartphone brands have reduced their OLED smartphone panel procurements for 2022 by single and double-digit percentages.

For Q2’22, we expect Q2’22 to decrease 17% Q/Q and 10% Y/Y to 119M panels and device revenue to decrease 23% Q/Q and 17% Y/Y to $63B. By substrate, we expect rigid OLED smartphone panels to decrease 21% Q/Q and 42% Y/Y, followed by flexible OLED smartphone panels with a 15% Q/Q decrease and 30% Y/Y increase.

For 2022, we expect OLED smartphone panels to decrease 5% Y/Y to 592M panels. Flexible OLED smartphone panels are expected to increase 2% Y/Y and account for a 59% unit share, up from 55% in 2021. Rigid OLED smartphone panels are expected to decline 14% Y/Y and account for a 41% unit share, down from 45% in 2021.

On a smartphone revenue basis, we expect rigid OLED smartphone revenue to decline 32% Y/Y with a 21% revenue share, down from 26% in 2021. Flexible AMOLED smartphone revenue is expected to decline 10% Y/Y with a 79% revenue share, up from 74% in 2021.

Based on the latest panel procurement estimates for 2022, brands reduced their panel procurement for rigid OLED smartphone panels by 10% to 34% from prior estimates. For flexible OLED smartphone panels, brands reduced their panel procurement by 2% to 51% from prior estimates.

Quarterly OLED Smartphone Panels by Substrate

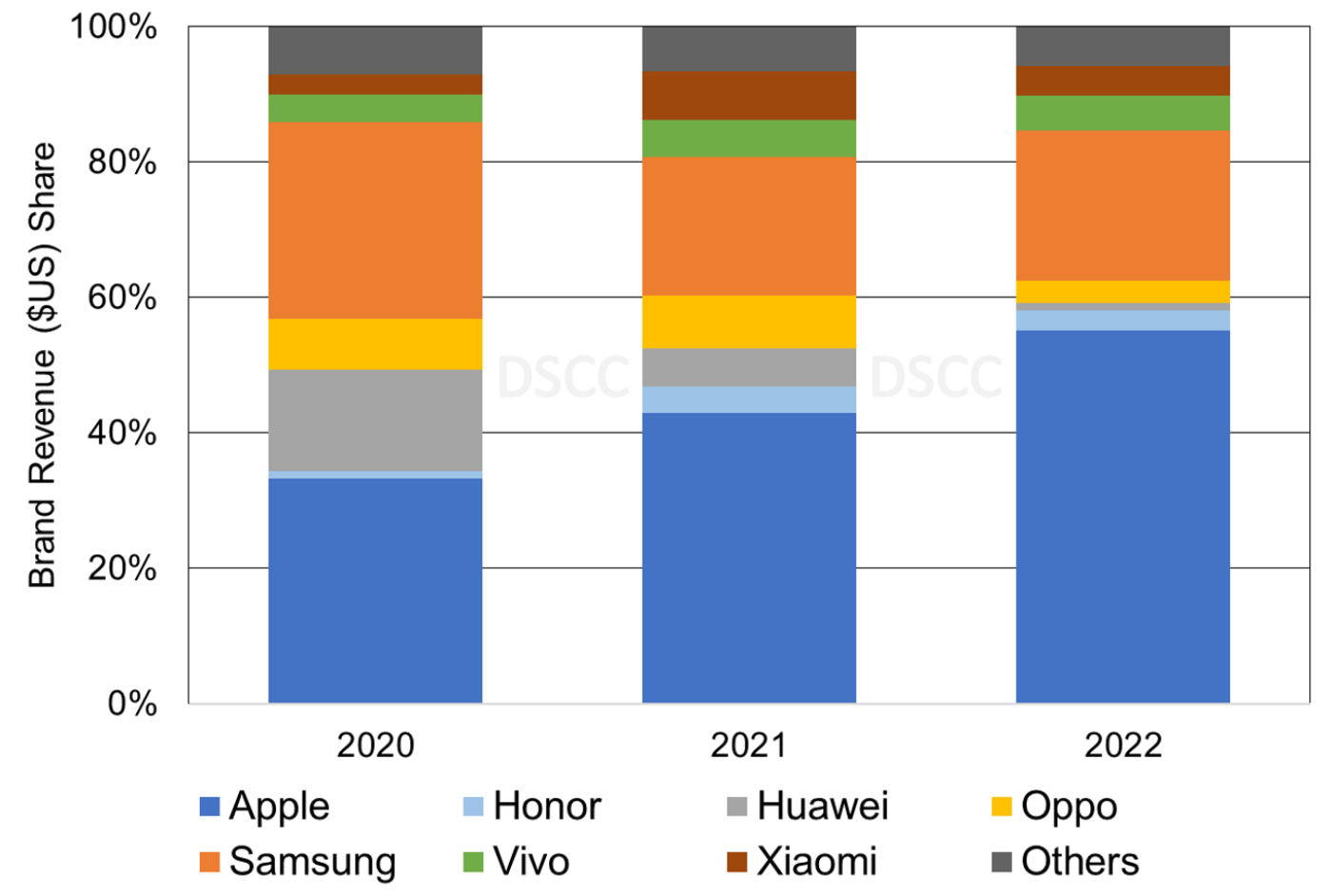

In 2022, for OLED panel procurement by brand, we expect Apple to have a 35% unit share and a 55% revenue share, up from 29% and 43%, respectively in 2021. We expect Samsung to have a 22% unit share and a 22% revenue share, up from 21% and 20%, respectively in 2021.

Annual OLED Smartphone Revenue Share by Brand

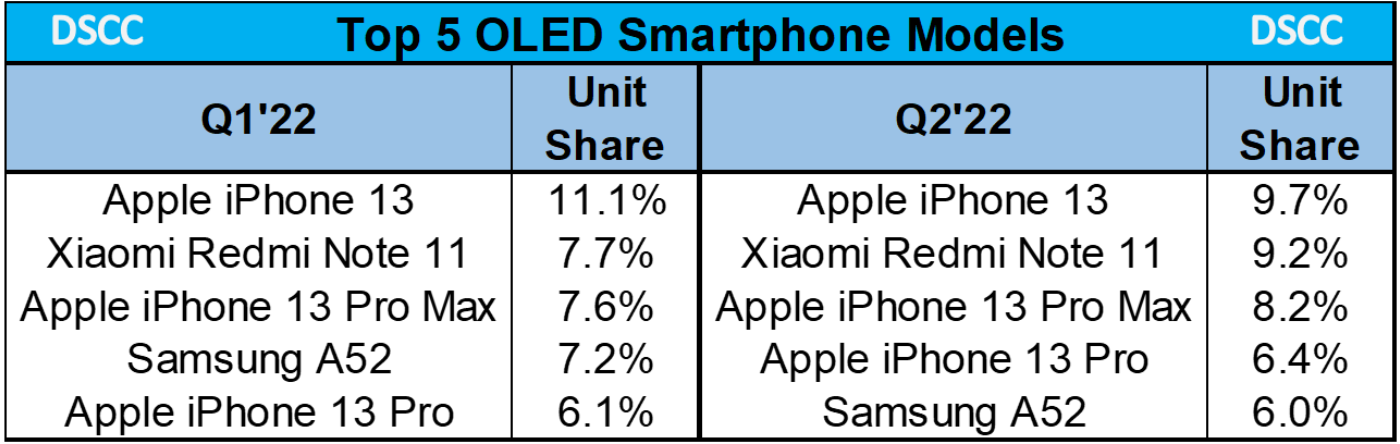

For Q2’22, we expect the top five models to be the Apple iPhone 13, Xiaomi Redmi Note 11, Apple iPhone 13 Pro Max, Apple iPhone 13 Pro and Samsung A52. These five models account for a 40% unit share and 52% smartphone revenue share of all OLED smartphone panels.

Top 5 OLED Smartphone Panel Procurement by Brand

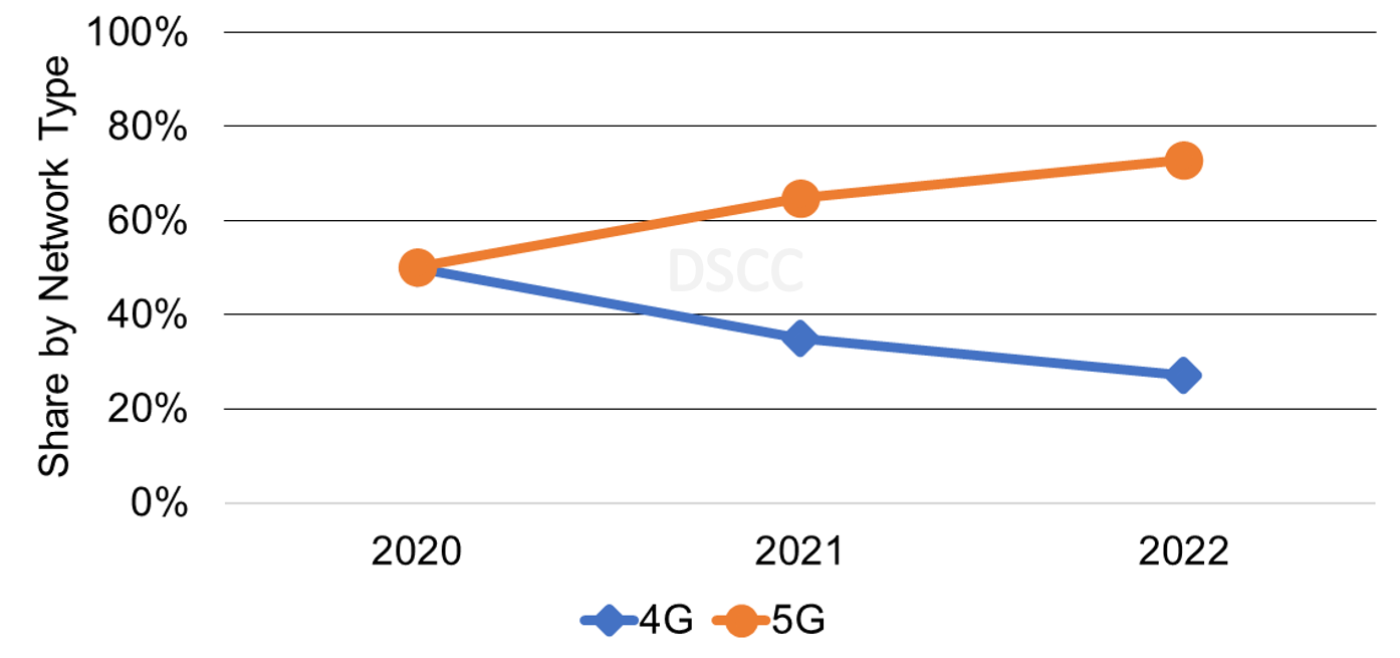

In 2022, as a result of more premium smartphones being introduced with 5G, we expect 5G to increase to a 73% unit share, up from 65%. As a result of the Apple iPhone 13 and Apple iPhone 14 series and other OLED smartphone brands supporting 5G mmWave + Sub-6GHz, we expect this network band to increase to a 36% share, up from 30% in 2021.

Annual Network Type Unit Share

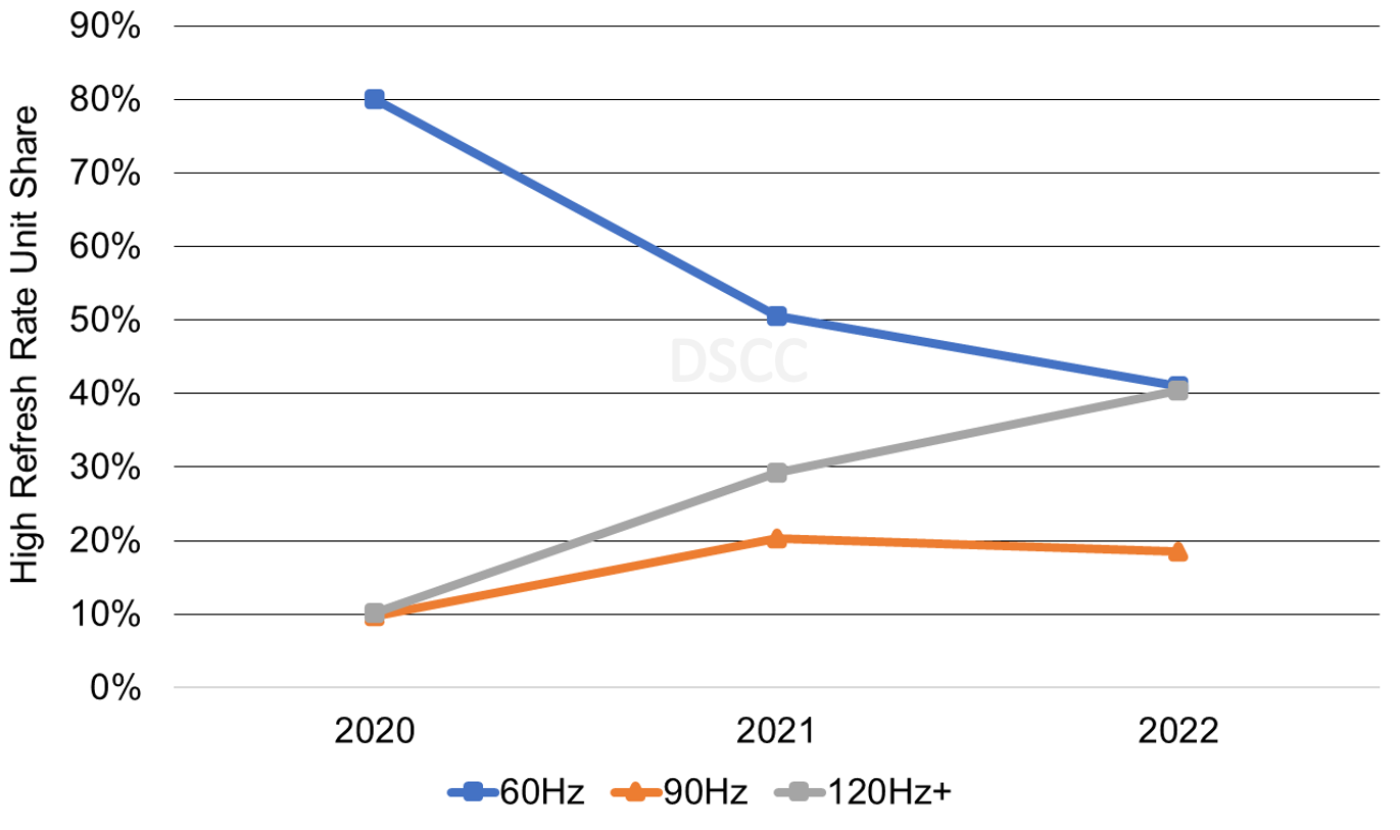

In 2022, we also expect 120Hz and higher refresh rates to have unit share gains. As more use cases for gaming, AR/VR, along with variable refresh rates and more efficient power consumption, we expect 120Hz+ refresh rates to increase to a 40% unit share, up from 29% in 2021.

Annual Refresh Rate Unit Share

Readers interested in subscribing to the Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced Smartphone Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。