Q1'22のAdvancedノートPC用FPD出荷が前期比26%減少~年間では前年比120%増の見通し

冒頭部和訳

DSCCが先週発行した Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) において、Advanced (※OLEDまたはMiniLED=先端技術FPD搭載) ノートPC用FPDの出荷実績と最新予測を発表した。驚くまでもないが、2022年のノートPC市場は全体的に減少傾向あり、AdvancedノートPC市場の成長もやや減速しており、その要因として、インフレ懸念、消費者需要の弱体化、COVID-19の封鎖措置によるサプライチェーンの混乱が挙げられる。

AdvancedノートPC用FPDのQ1'22出荷は前期比26%減で、サプライチェーンの混乱、ロシアとウクライナの紛争、中国におけるCOVID-19の封鎖措置、消費者需要の冷え込みがその要因となっている。このカテゴリーの出荷枚数は前年比では438%増の360万枚だった。前述のマクロ経済問題を考慮し、DSCCはAdvancedノートPC用FPD市場の2022年予測をわずかではあるが2%引き下げた。現時点の2022年のAdvancedノートPC用FPD出荷枚数は前年比120%増の1800万枚と予測され、これまでの予測値である1840万枚から下方修正、また内訳はMiniLEDがシェア49%、OLEDがシェア51%になると見られる。消費者需要は弱いものの、DellとHPは最近の決算発表で、「2-3年の交換サイクルとオフィスに戻る従業員の増加を背景に、産業需要は引き続き力強い」と報告している。また、高級ゲーミングノートPCや周辺機器といった分野では、消費者需要の成長が見られる。DellとHPはいずれも、高級製品としてOLED搭載ノートPCを提供している。

Advanced Notebooks Decline 26% But Remain Poised for 120% Y/Y Growth

Last week, we released the Advanced Notebook display results and our latest forecast in the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします). Not surprisingly, we see declines in the total notebook market and slightly slower growth in the advanced notebook display market in 2022 as a result of inflationary concerns, weakened consumer demand and supply chain disruptions amid COVID 19 lockdowns.

For advanced notebook PC displays, Q1’22 was down 26% Q/Q as a result of supply chain disruptions, the Russia-Ukraine conflict, China COVID-19 lockdowns and weakening consumer demand. The category was up 438% Y/Y to 3.6M panels. We have slightly lowered our 2022 forecast by 2% for the advanced notebook display market as a result of the aforementioned macroeconomic issues. For 2022, we expect advanced notebook PC displays to rise 120% Y/Y to 18M units versus 18.4M from our prior forecast, with MiniLEDs at a 49% share and OLEDs at a 51% share. Although consumer demand is weakening, Dell and HP reported during their most recent earnings call noted that commercial demand remains strong as a result of the two-to-three-year replacement cycle and more employees returning to the office. In addition, the area where consumer growth is occurring is in premium gaming notebooks PC segment and peripherals. Both Dell and HP offer OLED notebook PCs as premium products.

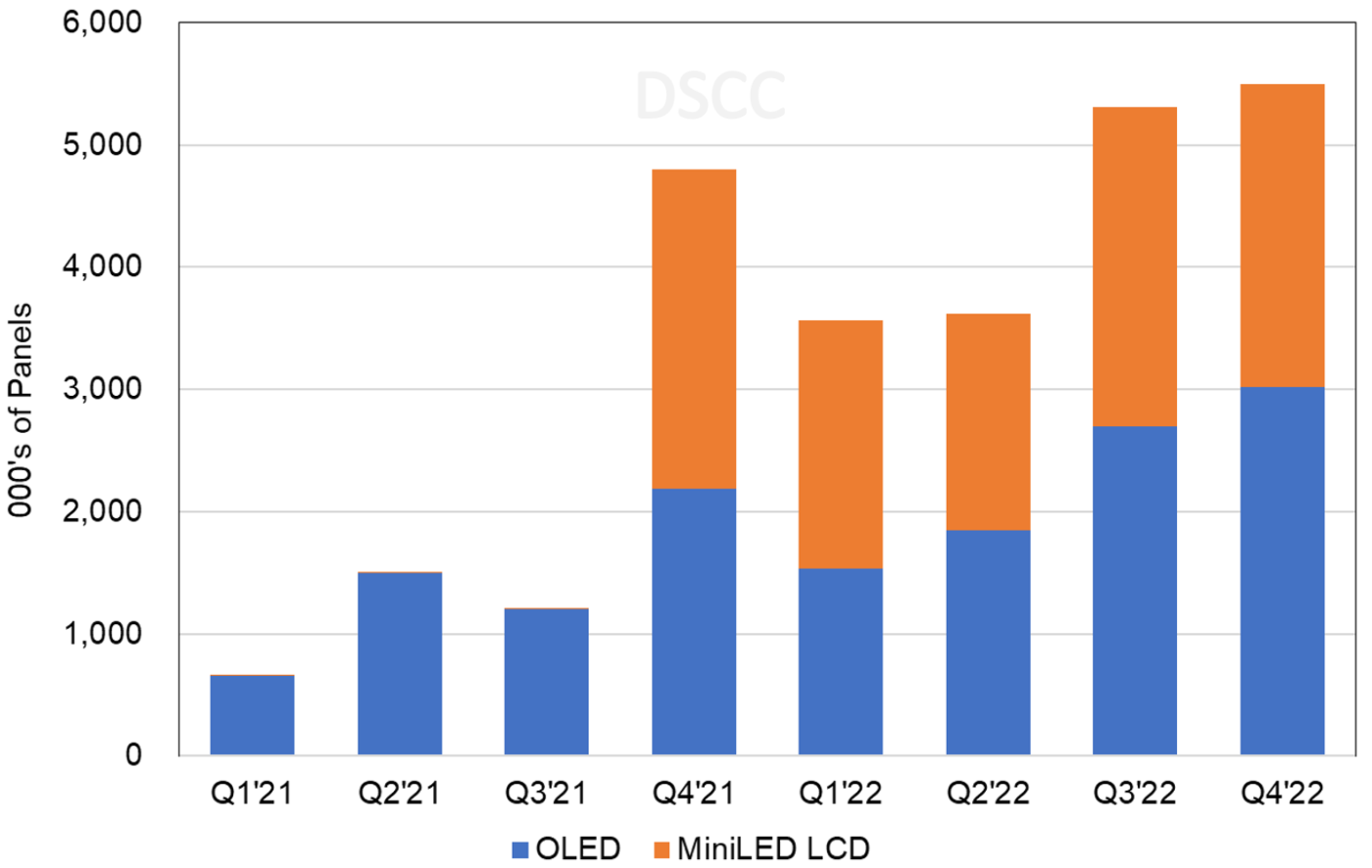

Advanced Notebook PC Display Shipments by Technology

Within the advanced notebook PC display category, MiniLED LCDs continue to lead the category in Q1’22 as a result of the Apple 14.2” and 16.2” MacBook Pro models. With the launch of new OLED notebook PCs by several brands and SDC’s continued efforts to grow the OLED notebook category, we expect OLEDs to retake the majority share in Q2’22 with a 51% share. In 2022, on a seasonality basis, OLEDs are expected to be weighted 37% in the first half vs. 63% in the second half. MiniLEDs are expected to be seasonal at 43% in the first half vs. 57% in the second half.

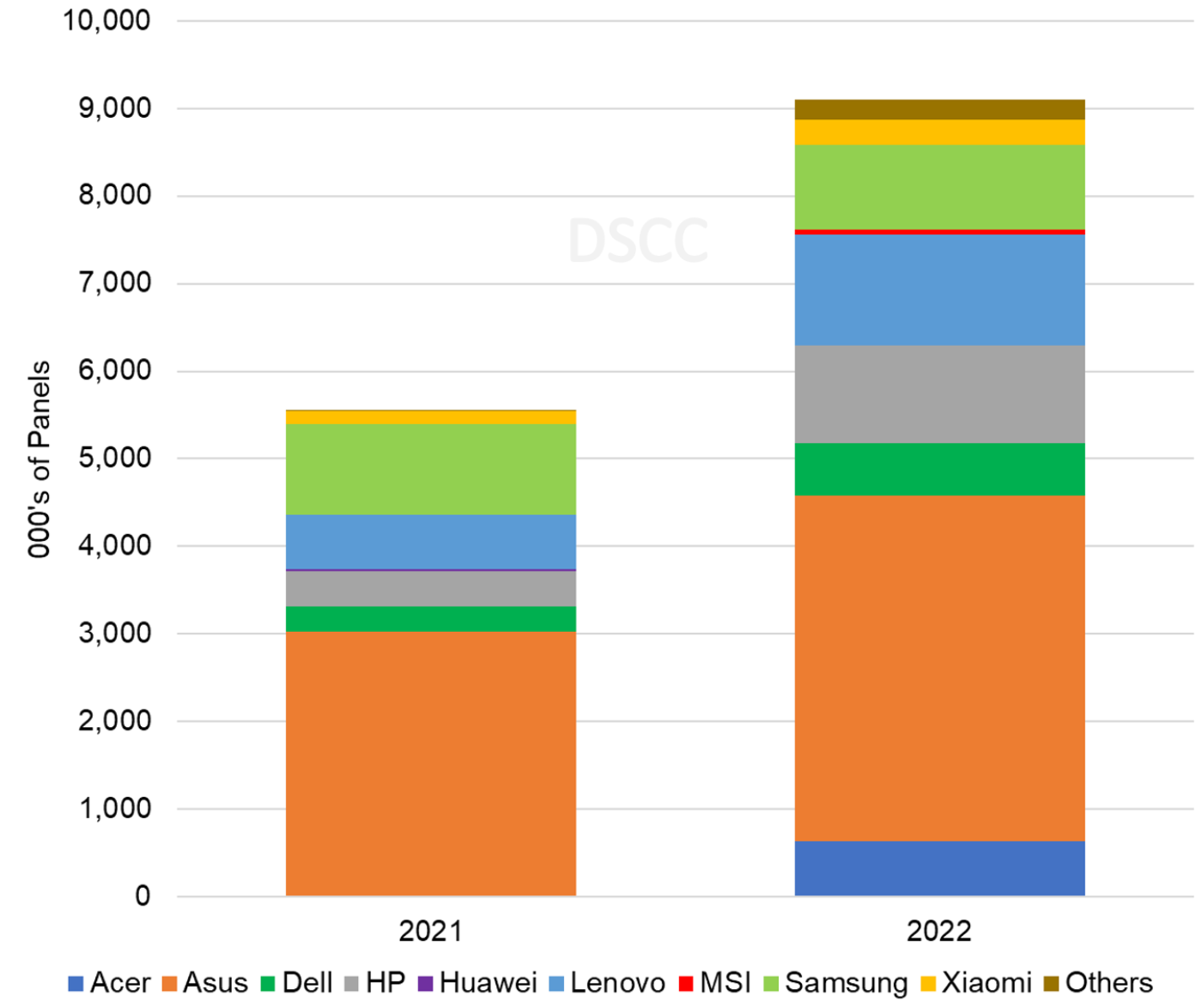

In Q1’22, for OLED notebook PC displays, Asus led with a 55% share, followed by Lenovo at 17% and Samsung and HP at 11% each. Asus is expected to lead in each quarter from Q2’22 to Q4’22 and decline to a 44% share in Q2’22 as other brands introduce new models. For 2022, we expect Asus to have a 43% share followed by Lenovo at 14%, HP at 12% and Samsung at 11% each. For MiniLED notebook PC displays, Apple dominates the category with a 99% share. Asus, MSI, GIGABYTE and Lenovo have introduced new MiniLED notebook PCs and are expected to increase share. As such, we expect Apple’s share to decline to a 96% share in 2022

OLED Notebook PC Display Shipments by Brand

SDC remains the dominant OLED panel supplier while the MiniLED notebook PC display market is currently split between LGD and Sharp for Apple products, while AUO, BOE and other panel suppliers provide other brands. SDC led in Q1’22 with a 43% share and is expected to lead in each quarter through Q4’22 and rise to a 53% share in Q4’22. On a panel revenue basis, LGD led in Q1’22 and is expected to lead through Q4’22. SDC is expected to have a revenue share of 33% in Q4’22 as a result of OLED models outpacing MiniLED models by ~22% in units in Q4’22.

By size in Q1’22, 14.2” MiniLED led with a 28% share followed by 16.2” MiniLED at 28%, up from 26% in Q4’21 and 15.6” OLED with a 21% share, up from 14% in Q4’21. The 14.2” and 16.2” MiniLED models from Apple are expected to lead each quarter through Q4’22. For 2022, 14.x” is expected to lead with a 38% share followed by 16.x”.

Advanced notebook PC displays are poised for long term growth and achieve double digit share of the overall notebook PC display category as a result of more capacity coming online, performance and costs improvements and the expectation that Apple will enter the OLED notebook PC category in 2024.

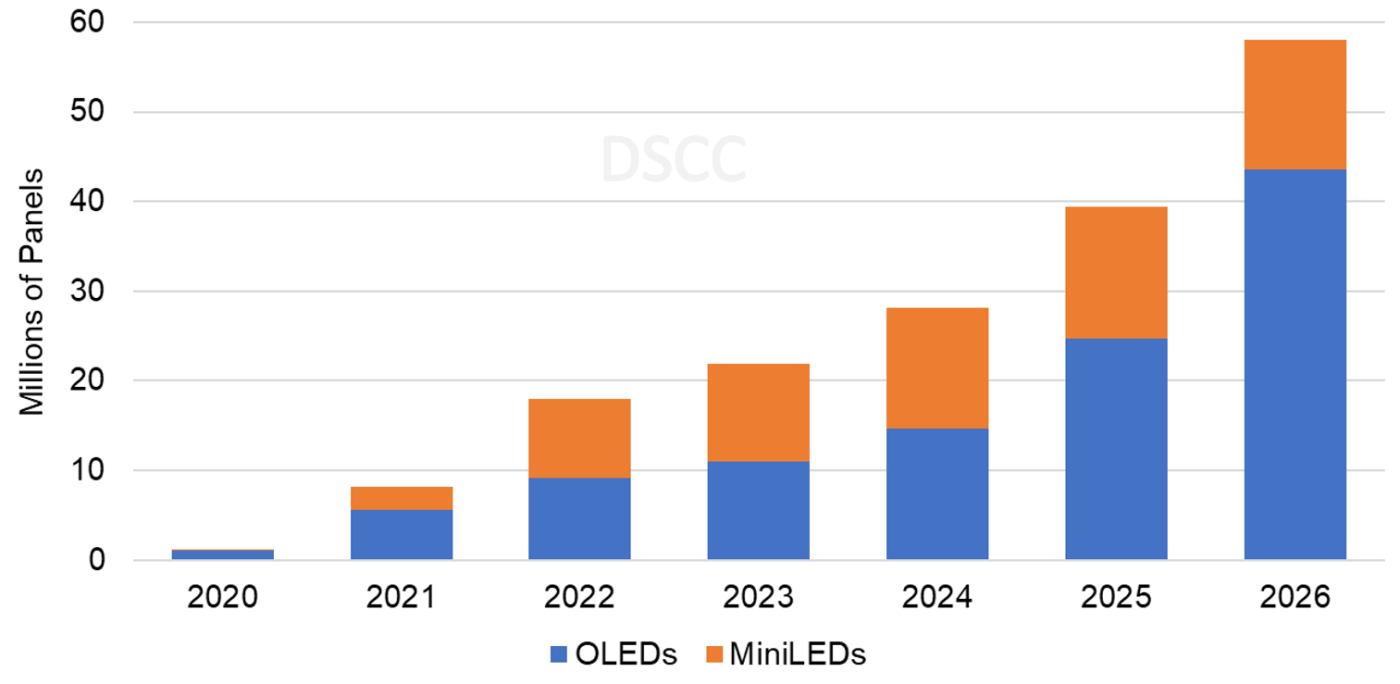

We expect advanced notebook PC displays to achieve a 23% unit share of the overall notebook PC market on a 50% CAGR with OLED notebook PC displays at a 54% CAGR and MiniLED notebook PC displays at a 40% CAGR from 2021 – 2026.

Some of these performance and costs improvements include:

- Tandem structures which will boost brightness, lifetime and efficiency and lower power consumption;

- A phosphorescent blue OLED emitter which is now expected to hit the market from 2024 which will also boost brightness and efficiency and significantly reduce power;

- Rigid + thin film encapsulation (TFE) substrates which should reduce costs vs. flexible substrates found in mobile displays and offer thinner and lighter solutions than rigid substrates;

- Decline in the number of MiniLEDs per device due to efficacy improvements, optical improvements and higher yields;

- Lower MiniLED backplane costs from fewer MiniLEDs per device as well as the use of discrete driver ICs should result in simpler PCB backplanes with fewer layers.

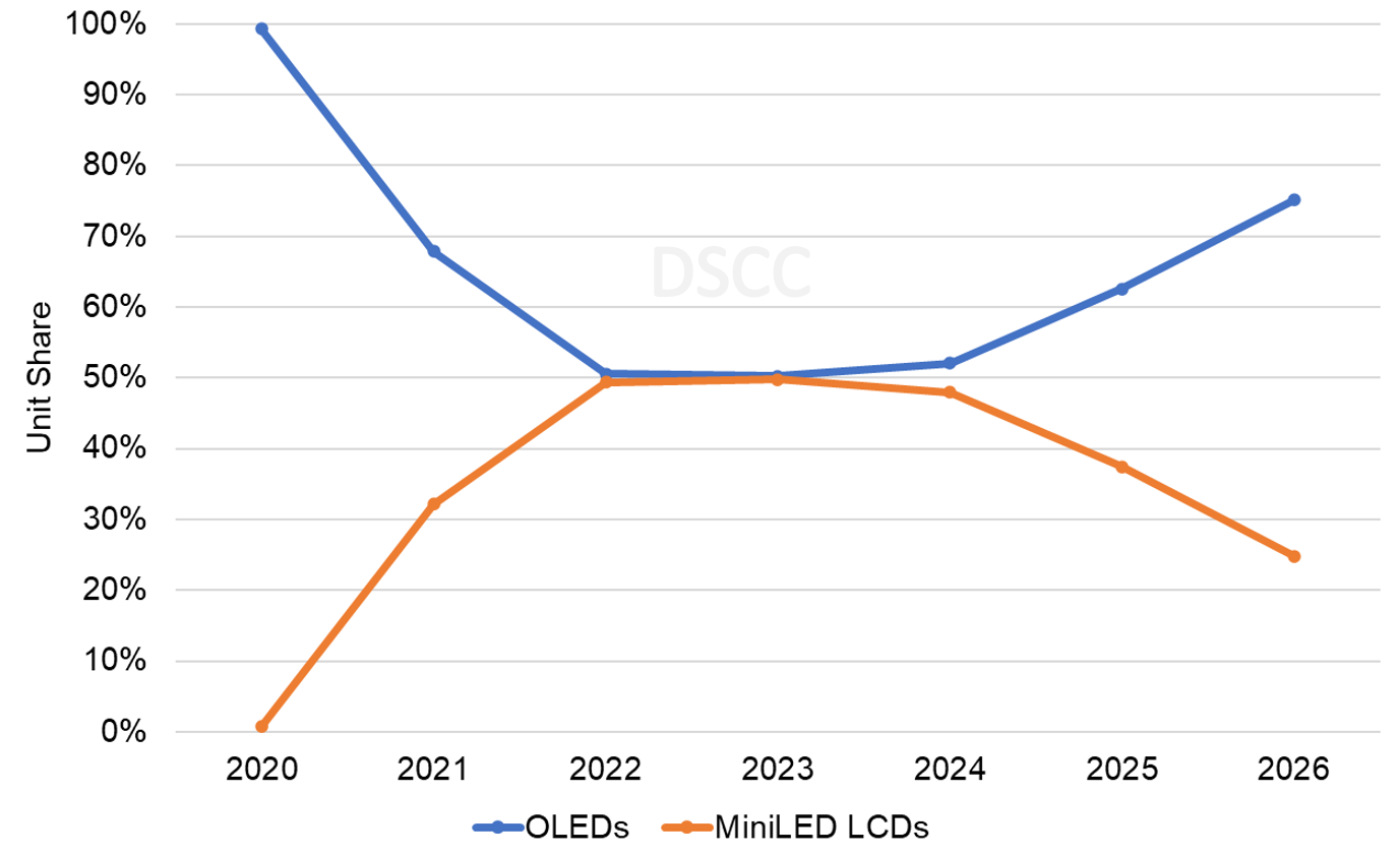

OLEDs are forecasted to account for a 75% share of the advanced notebook display market in 2026 vs. 51% in 2022. Advanced notebook displays are expected to grow to a 23% unit share and a 42% revenue share of notebook PC display market in 2026 vs, an 8% unit share to a 19% revenue share in 2022.

MiniLED LCD vs. OLED Notebook Panel Shipments

MiniLED LCD vs. OLED Notebook Unit Share

For more insights into Advanced Display shipments by brand, size, resolution, refresh rate, backplane, substrate, OLED stack, touch, etc. as well as panel and product roadmap, cost and technology advancements, please see the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) or contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced IT Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。