SID/DSCC 2022ハイライト~スマートフォン用FPD市場と技術動向

冒頭部和訳

DSCCのスマートフォン市場講演

著者 (注: DSCC創業者兼CEO・Ross Young) からは、本講演で以下のテーマを取り上げた。

* 出荷実績最新情報:スマートフォンセット、フォルダブル製品、スマートフォン用FPD

* 技術動向:FPDとFPD以外

* ロードマッププレビュー:Apple、Samsung、その他フォルダブル製品

* 長期市場予測

最初に、最新のスマートフォンセット出荷実績と2022年地域別予測について説明した。2021年のスマートフォン出荷台数は4%増で14億台に到達、地域別では中国が最大で、中東とアフリカが最も急成長している。2022年市場は1%減少の見通しで、アジア太平洋地域が中国を追い抜くと予測される。東欧と中国の減少が最も大きくなる見通しだ。ただし、中国のロックダウン、戦争の継続、インフレなどの行方によっては、市場は10-15%減少の可能性もあるという懸念が高まっている。LCDが強い中国と東欧が弱いため、LCDの出荷枚数に最も大きな影響が出そうな見通しだ。LCDの出荷枚数を最大30%削減するブランドもあるという噂も聞かれる。

スマートフォン用FPDも2021年出荷枚数は4%増の15億枚で、現時点の市場予測は1%減少の見通しである。2021年のAMOLED出荷枚数は26%増の6億3400万枚で、SID 2021での予測の精度は99.24%だった。各企業が旗艦製品に重点を置くことから、2022年のAMOLED出荷枚数はさらに10%増の6億9400万枚になり、AMOLEDのシェアは42%から46%に上昇すると現時点で予測されている。DSCCのOLED市場予測は、Q1’22には前年比6%減、2022年下半期には成長となっている。ただし、2022年のフレキシブルOLED出荷枚数が大幅に減少する可能性についてヒアリングしたところ、中国のロックダウン期間次第では14%減少の可能性もある。LCDは2021年に8%減少したが、中国と東欧の影響を受けて2022年にはさらに8%減少が予測される。ただし、注文のキャンセルや遅延が大きいという話も聞かれることから、実際の2022年出荷はさらに悪くなる可能性もある。

SID/DSCC 2022 BUSINESS CONFERENCE HIGHLIGHTS - Smartphone Display Market and Technology Outlook

The smartphone session consisted of talks from myself and OTI Lumionics Co-Founder and Vice President Jacky Qiu.

DSCC on Smartphones

In my talk I covered the:

- Latest smartphone, foldable and display results

- Display and non-display technology trends

- Roadmap previews for Apple, Samsung and other foldables

- Long term forecast

I started by covering the latest smartphone set shipment results and a 2022 forecast by region. Smartphone unit shipments were up 4% in 2021 to 1.4B units, with China the largest region and Middle East and Africa growing the fastest. For 2022, we forecast the market to fall 1% with Asia Pacific expected to overtake China. Eastern Europe and China are expected to decline the most. But there are growing concerns that the market could be down a lot more, 10% - 15%, if China shutdowns are extended, war persists, inflation, etc. LCD volumes appear to be most affected due to weakness in China and Eastern Europe where LCDs are stronger. Some brands are rumored to be cutting up to 30% of their LCD volumes.

In the case of smartphone panels, we also saw a 4% increase in 2021 to 1.5B panels and currently forecast a 1% decline. In 2021, AMOLED shipments rose 26% to 634M vs. our SID 2021 forecast, meaning we were 99.24% accurate. In 2022, we are currently showing AMOLEDs rising another 10% to 694M boosting their share from 42% to 46% as companies prioritize flagships. Our Q1’22 OLED forecast is down 6% Y/Y, with growth in 2H’22. But hearing about the possibility for larger declines for 2022 flexible OLED volumes, as much as 14% depending on the length of China shutdowns, etc. LCDs fell 8% in 2021 and are expected to fall another 8% in 2022, impacted by China and Eastern Europe. However, actual 2022 results may be worse with talk about larger order cancellations/delays.

In terms of smartphone panel procurement share, most of the leading brands gained share at the expense of Huawei for the second year in a row. Huawei’s demise also slowed down flexible OLED penetration as their flexible OLED penetration share was higher than Oppo, Vivo and Xiaomi, which was quantified in the slides that showed OLED share of total panel procurement and each company’s flexible OLED penetration rate. Also provided was the rigid vs. flexible vs. foldable share. Rigid OLEDs held onto their 45% share in 2021, growing 25% after a big drop in 2020. Flexible actually grew slower than rigid at 24%. Foldable grew 200% to 10M panels, but remains a niche with only Samsung driving large volumes.

I also showed the top brands for flexible OLEDs, which represents flagship share with all flagships using flexible OLEDs. Apple maintains a large advantage in flexible OLEDs and accounted for 53% of flexible OLED panels in 2021, up from 42% in 2022, taking share from Huawei, Samsung and Oppo. Apple had the top six best selling models, seven of the top 10 and eight of the top 16. The iPhone 12 Mini and 13 Mini had the lowest volumes in their responsive product families, which is why they are replacing it with the 6.7” iPhone 14 Max. DSCC expects Apple to maintain more than a 50% share in 2022 as well.

We also shared the outlook by brand as well as the possible downside based on discussions we have had within the supply chain. In total, we showed that 2022 flexible OLED panel volumes could be 60M units or 14% lower than expected. Xiaomi appears to be lowering their volumes the most in both OLEDs and LCDs. Oppo is seeing the smallest decline as Realme takes share.

In the case of rigid OLEDs, Samsung led with a 30% share in 2021 with Xiaomi (Redmi) rising from #5 to #2, earning a 21% share with the #1 model and three models in the top 10. Oppo was close behind at 20%.

In foldables, Samsung has completely dominated with more than an 80% share annually from 2019-2021. In 2021, the Samsung Galaxy Z Flip 3 led this segment with a 51% share followed by the Z Fold 3 with a 26% share. I also shared the final results for Q1’22 foldable panel shipments and the Z Flip 3 led in Q1’22 as well with a 53% share followed by the Huawei P50 Pocket with a 23% share. In total, clamshells had an 80% share. Q1’22 volumes rose 264% Y/Y and was 1% below our forecast at 2.6M. We also have good visibility into Q2’22 and we see 3.3M panels shipped, up 154% Y/Y, as Samsung begins its Z Flip 4/Fold 4 ramp.

By panel supplier, SDC is completely dominant with an 86% share in 2021, with no other supplier with more than a 7% share. SDC is also dominant in flexible OLEDs with a 57% share in 2021. BOE gained share for five straight quarters after recovering from Huawei’s situation. LGD earned its highest share yet in Q4’21 at 17% on strength at Apple. Besides SDC, LGD and BOE, no other supplier has earned a double-digit share in a quarter nor is expected to in the near future.

Other than one quarter when it was in between product launches, SDC has had no less than a 70% share each quarter with >90% share in 2H’21. BOE has consistently been #2 with its customer Huawei the only other brand besides Samsung looking to drive larger volumes to date.

We also shared our 2022 forecast by panel supplier and expect SDC to only lose a small amount of share to 67%, benefiting from BOE’s challenges at Apple. SDC’s largest two customers remain Samsung and Apple who account for around a 60% of their unit volume. Xiaomi and Oppo are its next two largest customers. BOE was expected to gain share on its iPhone 14 design win and also growth at Honor, Oppo, Samsung and Vivo. BOE’s reliance on Huawei has declined from 73% in 2020 to 36% in 2021 to <10% in 2022. Apple is still expected to be its largest customer in 2022. LGD is almost entirely reliant on Apple. Visionox is seeing growth at Honor and Huawei. China Star and Tianma look to Xiaomi for majority of their volumes.

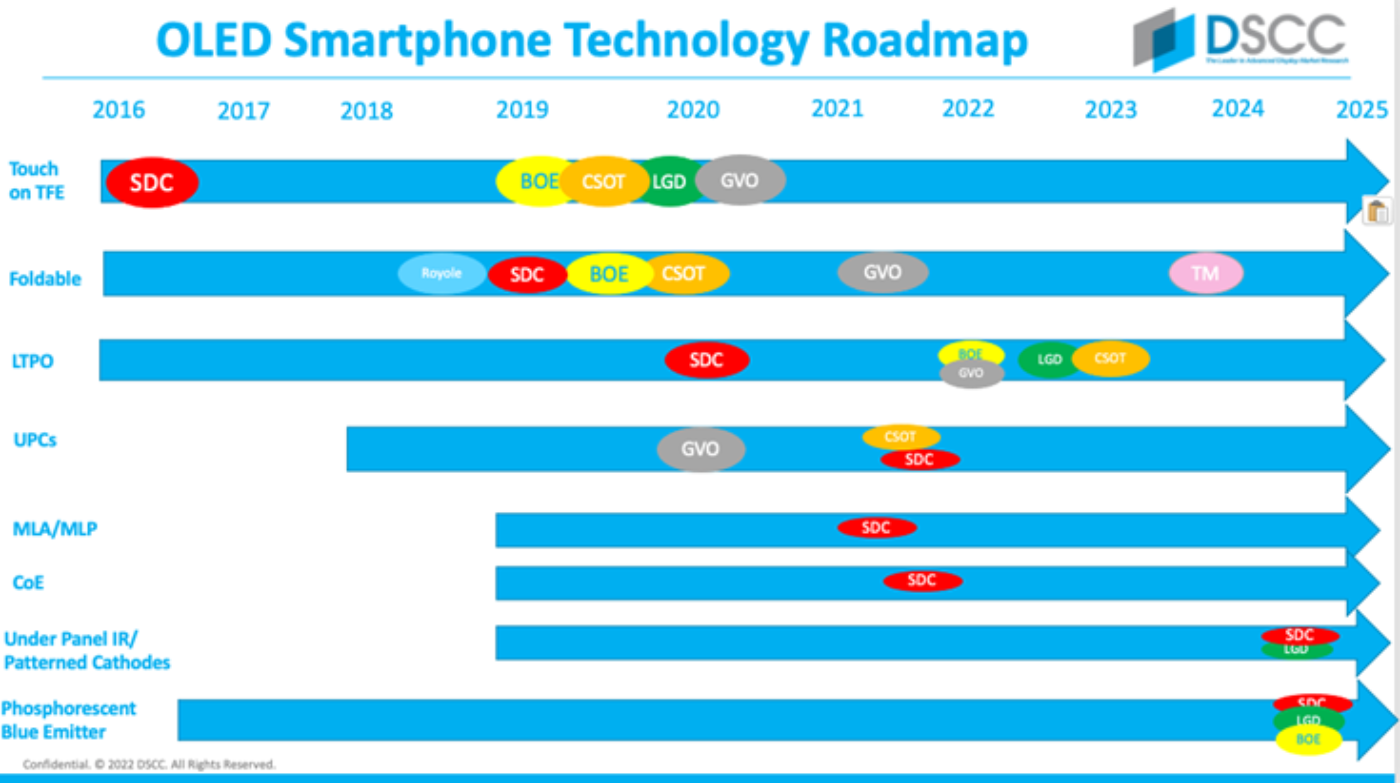

DSCC’s smartphone display technology roadmap is shown below. As indicated:

- SDC had a three-year lead on touch on TFE;

- SDC had a two-year lead in smartphone LTPO;

- SDC’s lead in CoE and MLA/MLP is at least one year;

- It was not first to market with foldables or under panel cameras.

We can say that SDC’s lead in bringing new innovations to market has declined, but it continues to innovate and manufacture at the industry’s highest yields, which has kept its market share and margins high. We expect under panel face ID with patterned cathodes and phosphorescent blue OLED emitters to come to market in 2024 with SDC and LGD likely to be first for the Apple Pro models for under panel Face ID and most suppliers looking to take advantage of phosphorescent blue.

I also discussed where we are with:

- LTPO penetration

- Panel supplier share for LTPO

- Penetration by refresh rate

- Brand share by refresh rate

In regards to foldable, I covered the recent developments with water drop hinges and wide aspect ratios. I then covered what is coming, revealing product roadmaps. In particular, I covered:

- iPhone 14 Series detailed specs including larger panels for the 14 Pro and Pro Max due to the unique pill + hole shape. Replacing the lower priced Mini with the higher priced Max should ensure a blended higher ASP per unit on the iPhone 14.

- Apple’s long term roadmap for the front of the panel including pill+hole vs. under panel face ID+hole vs. the timing for the completely notch-less and hole-less iPhones.

- What to expect for the Z Flip 4 and Z Fold 4 as well as initial production for the Flip 4 and Fold 4 vs. the Flip 3 and Fold 3 through August. It looks like foldable smartphones will have another high growth year based on the initial ramp plans.

- Display specs and form factor for foldables from other brands. Currently showing up to four new clamshells coming in 2H’22 from Motorola, Oppo, TCL and Vivo.

I then shared our longer term smartphone forecast revealing LCD vs. OLED share with OLEDs finally overtaking LCDs in 2024. I also covered panel unit and revenue share by type, flexible vs. rigid vs. foldable and our brand unit share forecast through 2026. We expect the Chinese brands to gain share from 2023, as they strengthen overseas and enjoy higher growth in China than others. I also broke out our brand unit share forecast for just OLED smartphones with Apple expected to continue to lead as well as for just flexible/foldable/rollable smartphones with Apple enjoying an even more dominant position. In summary:

2022 – A Challenging Year

- Smartphone and smartphone panel shipments are currently predicted to fall 1% in 2022 but are challenged as the China shutdowns, Russia-Ukraine war, higher inflation and rising interest rates linger. Q2’22 is expected to be much weaker than previously expected. Will be a volatile year.

OLEDs to Outperform

- OLEDs to outperform LCDs due to greater weakness in China and Eastern Europe where LCDs are stronger. In addition, companies tend to be more focused on growing their flagship (i.e. flexible OLED) products. Flexible OLEDs to gain share every year through 2025. Rigid suffering from slower capacity growth, allocation shift to IT.

Apple Dominating OLED Market

- Apple dominates the OLED smartphone market despite no rigid or foldable offering.

- Expected to lose share as the category grows and prices reach lower and lower price points

- iPhone 14 Series should boost its revenue share by replacing a 5.4” model with a 6.7” model.

Foldables to Surge in 2022

- Should be a good year for foldables with around 100% growth to over 20M panels and over 16M phone shipments on aggressive plans at Samsung and SDC and more brands launching more products, especially lower priced clamshells.

Smartphones to Remain #1 Category for Display Revenues

- Smartphones to remain the top category for display revenues.

- Brands will look to continue to differentiate their devices through advanced technologies to minimize commoditization – LTPO, MLP, UPCs, foldables, rollable, CoE, etc.

OTI Lumionics

At last year’s conference, OTI Lumionics shared a technology roadmap for the OLED industry, revealing all the performance and functionality enhancements that could be accomplished by pattering cathodes using their proprietary materials and self assembly process. It was one of the best talks of the event. This year, they focused even more on the status and outlook for under display cameras and near infra-red sensors (Face ID) for mobile devices as well as the status of the commercialization of their patterned cathode process.

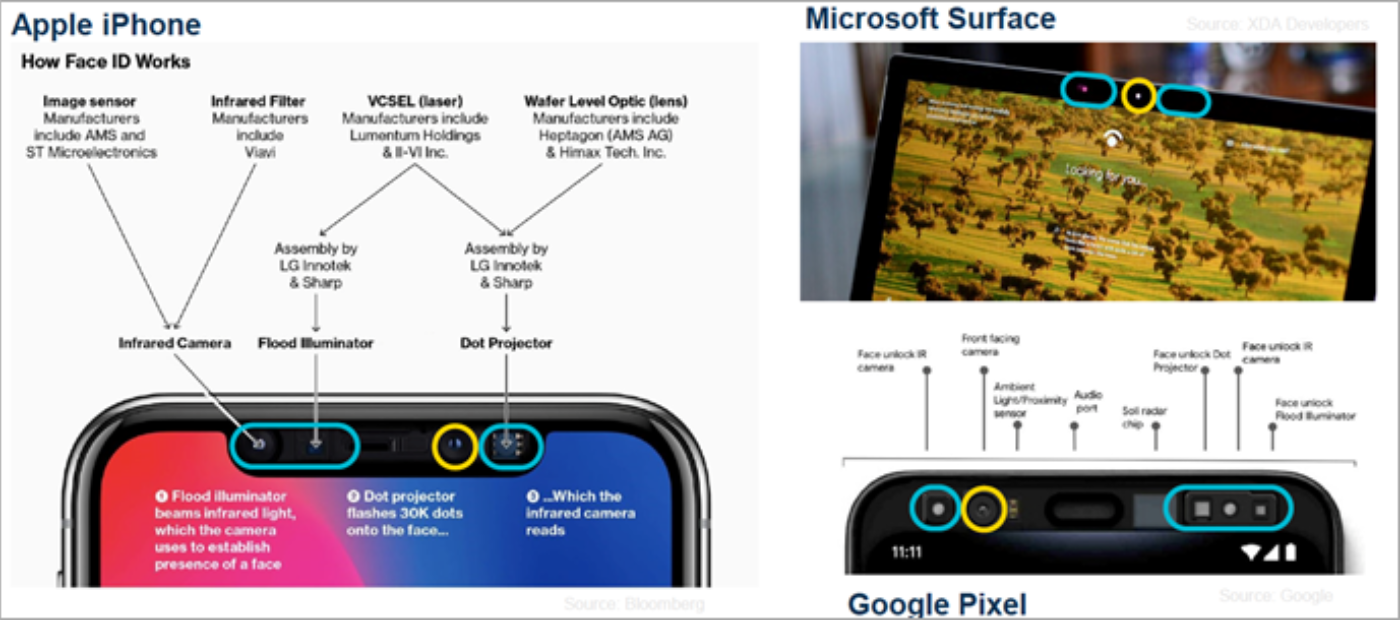

This year’s talk was given by Co-Founder and VP, Jacky Qiu. He started his talk by arguing that market trends are converging to drive demand for the seamless integration of cameras and sensors with displays. The average smartphone display size has been growing annually but has now likely plateaued, so the cameras and sensors need to move under the display to continue to maximize display area. In addition, he argued that the shift to remote work is requiring demand for better video call experience and more secure authentication. He cited sources indicating that 3D facial recognition may be the future of secure authentication with even the IRS requiring it to access your taxes online and that more tablets and laptops are adding 3D facial recognition. The problem is that front facing cameras and sensors need a lot of space. Their solution, which they went into great detail on, was to put the cameras and sensors under the panel through their CPM materials and patterning holes in the cathode through an additional fine metal mask (FMM) step.

Front Facing Cameras/Sensors Take a Lot of Space

Jacky then went into great detail in regards to the current performance of smartphones with under panel cameras (UPCs), which deliver a poor user experience at a high cost. He indicated that the problems with UPCs can be segmented into six areas:

1. Image Blur/Diffraction

2. Low Light Performance

3. Video Conferencing

4. System Integration

5. Pixel Lifetime/Burn-in

6. 3D Facial Recognition

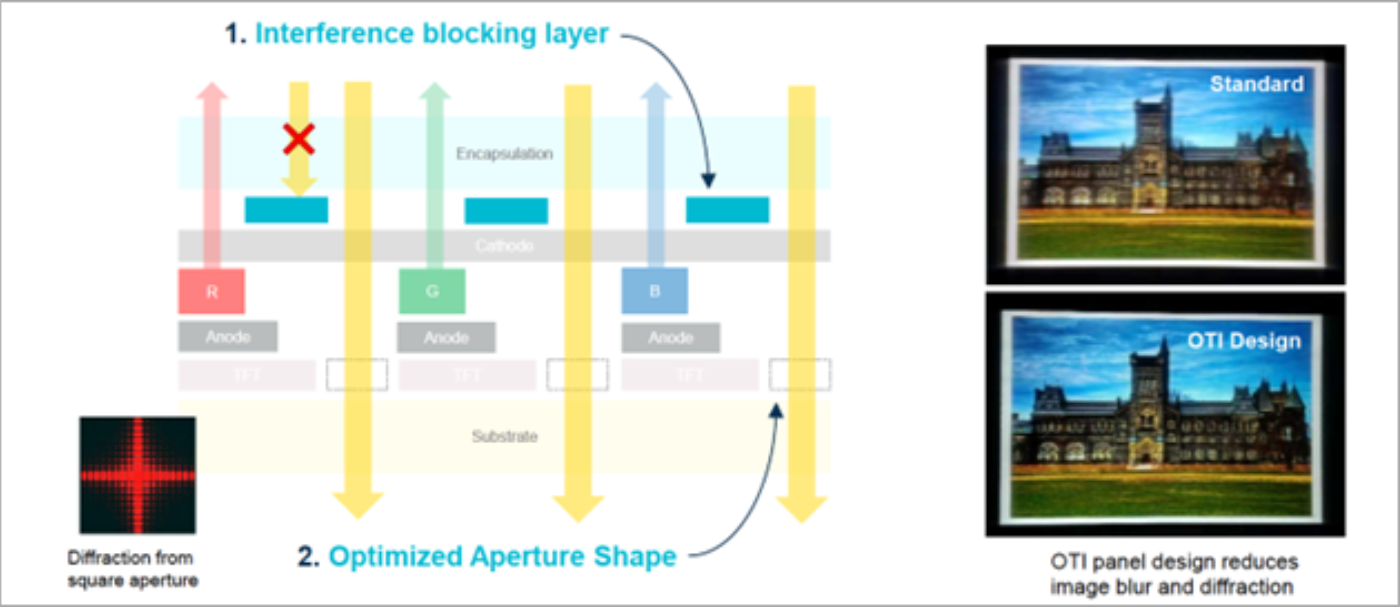

For #1, image blur is being caused in today’s UPCs from:

- Diffraction from polygonal apertures;

- Interference from different areas of the panel.

To minimize this issue, OTI has developed an interference blocking layer patterned in between the cathode and encapsulation layer which boosts performance as shown below:

Solving the Image Blur Diffraction Issues with an Interference Blocking Layer

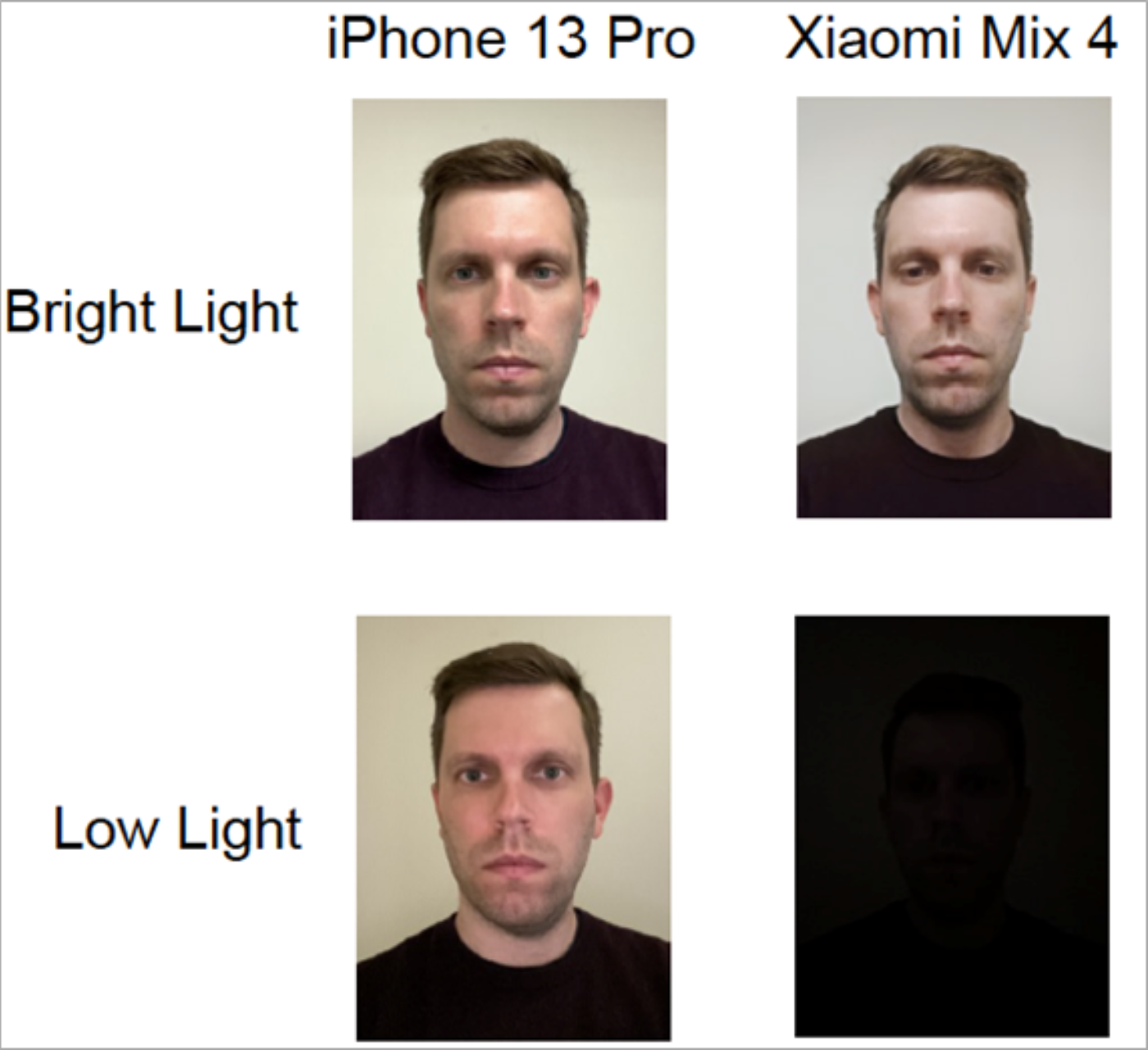

In regards to #2, they compared the low light performance on the Xiaomi Mix 4, which has an UPC with the iPhone 13 Pro as shown here and it is obviously not good. The Xiaomi UPC is limited by 10% transparency. They also cited user complaints, which also commented that facial authentication for apps such as banking, etc., don’t work well, particularly in low light.

UPC Low Light Performance

Improved transparency can help with this issue and OTI can solve this by patterning the cathode.

For #3, poor video conferencing performance, he indicated that software-based image compensation is a challenge for real-time video on mobile devices with limited power. AI image compensation requires considerable computational overhead and power and can’t keep up with real-time video at full resolution. They believe new AI image processing software and or hardware is required for delivering high quality real time video from UPCs and sensors. He indicated that Qualcomm may need to get involved and it may require space on 3nm processors to accomplish the real time processing required. A separate ISP may also be needed to solve the issue.

For #4, system integration, he indicated that the tight integration of the camera, sensor, display teams are needed which could limit device reparability and delay introduction. Already we have seen Face ID stop working if a third party replaces the phone’s display. The pairing of the camera/sensor models and display could be required if each device requires unique calibration. Also, we saw that Samsung has disabled the Z Fold 3’s camera if you unlock its bootloader, which means access to raw camera data could be blocked to prevent analysis of image compensation methods.

For #5, pixel lifetime and burn-in, he showed examples of the Z Fold 3, which uses larger pixels resulting in the camera area looking noticeable and bad while the Xiaomi Mix 4 uses smaller pixels and increased the potential for burn-in. Weibo users have reported that the Xiaomi Mix 4 has visible pixel burn-in after only 100 hours at full brightness, which can be attributed to the smaller pixels. OTI has developed ways to minimize burn-in by adding a second cathode with the cathode thickness optimized for each color which can also significantly improve color performance.

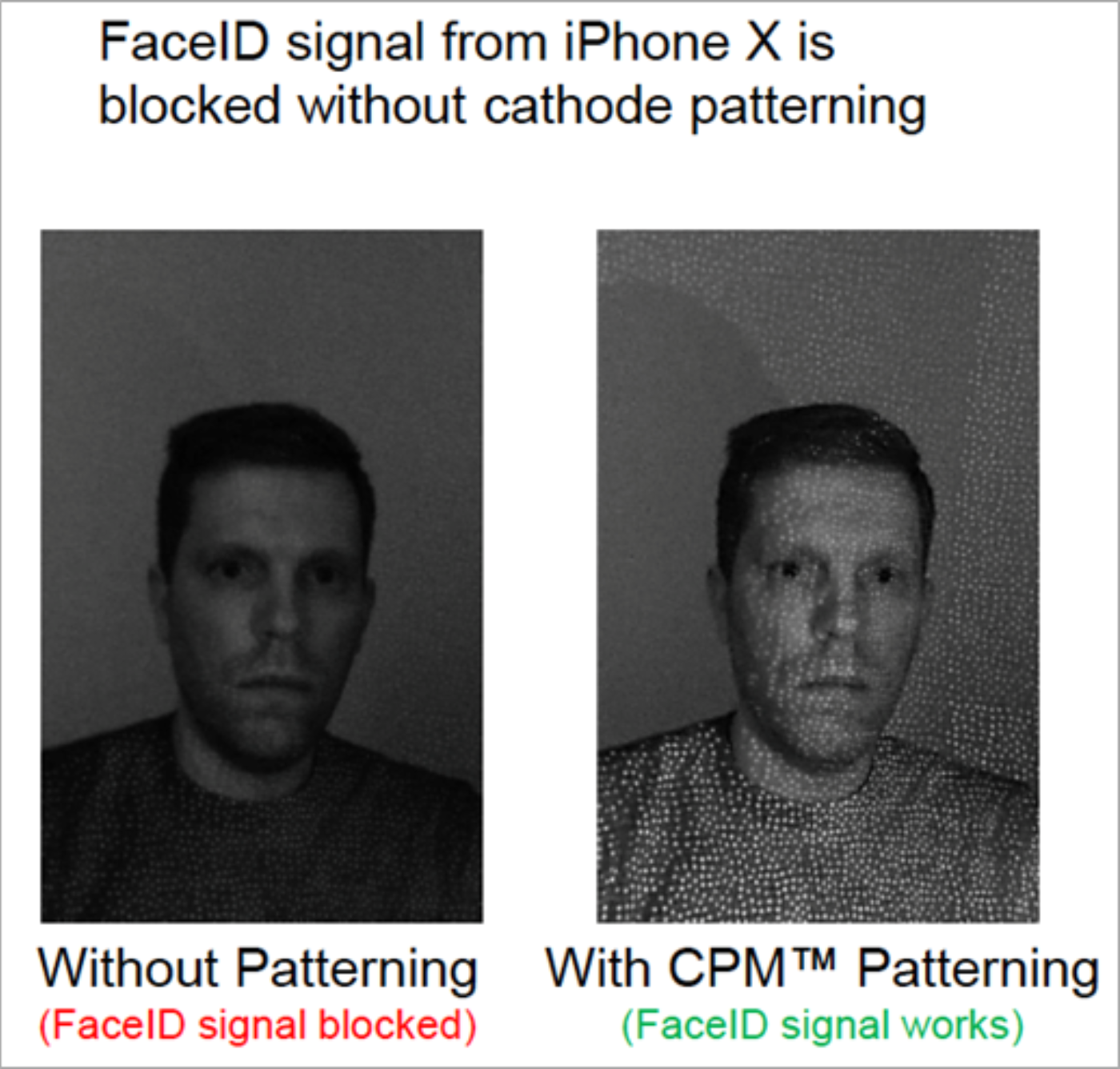

In regards to #6, 3D facial recognition using near infrared, performance is significantly reduced without cathode patterning as the cathode blocks the infrared transmission letting only 10% of the light through. They demonstrated this using a modified iPhone X with a transparent OLED panel area and Face ID failed.

Jacky also revealed that their cathode patterning process is now qualified by two panel suppliers for G6 and showed a render with an additional chamber added to the Canon Tokki FMM VTE system for their process. We believe these suppliers are SDC and LGD.

At SID, OTI also announced that they had partnered with FMM market leader DNP on both evaporation mask manufacturing and cleaning. The DNP developed cleaning processor for OTI’s CPM materials provides customers with a new option for a potentially faster and more efficient evaporation mask cleaning protocol at CPM deposition cycles during OLED panel production processes. The DNP solution will be available in the near future. According to DNP GM of their Fine Optronics Division Minoru Nakanishi, “We are very pleased that DNP could establish evaporation mask cleaning technology together with OTI’s CPM materials which bring new design innovation to panel makers. DNP will continue to provide new solutions to panel makers.”