2021年のAdvanced (OLEDまたはMiniLED LCD搭載) ノートPC用FPD出荷は629%増で820万枚到達~Appleがシェア54%でQ4'21をリード

冒頭部和訳

DSCCの Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) では、OLEDまたはMiniLED LCDを搭載したタブレット、ノートPC、モニターの出荷データを、四半期/ブランド/サイズ/解像度/リフレッシュレートの項目別に、またその他のディスプレイおよび非ディスプレイ機能別に提示している。

DSCCは先週、AdvancedノートPC用ディスプレイ出荷の実績と最新予測を発表した。驚くには当たらないが、OLEDとMiniLEDの両方とも急速に増加しており、展望も明るく、著しい成長を遂げている。

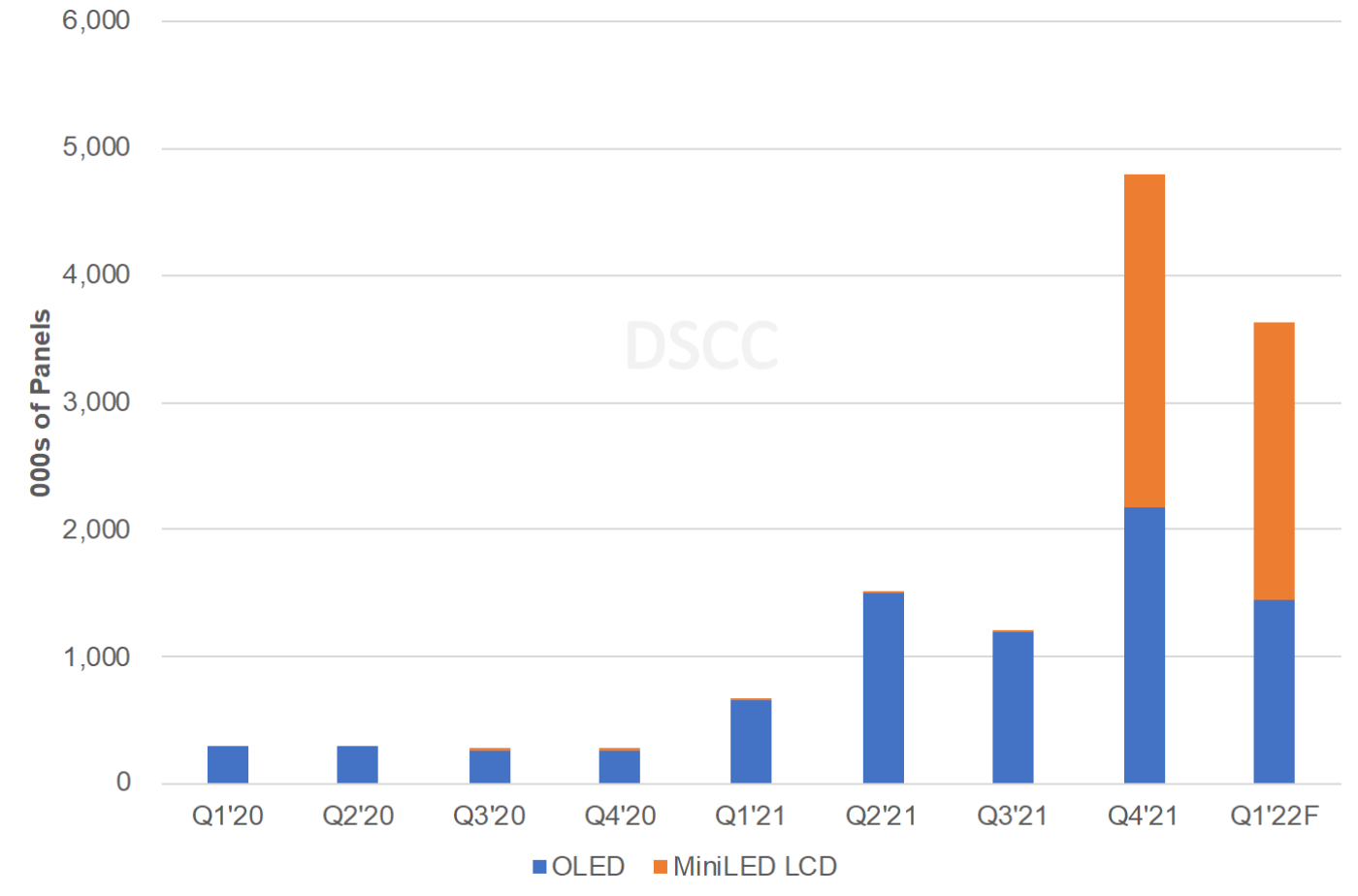

Q4'21はAdvancedノートPC用ディスプレイ出荷が前期比298%増・前年比1717%増の480万枚に到達、過去最高を記録した。年間ベースで見ると、2021年出荷は前年比629%増の820万枚となっている。AppleのMiniLED搭載MacBook ProとOLEDの両方がQ4'21に予測以上の実績を記録したことから、2021年出荷は予測より10%高い水準となった。Appleの14.2インチと16.2インチのMacBook Pro発売が成功したため、MiniLEDのシェアがQ4’21に54%へと急上昇し、その年間シェアは32%となった。120HzのOLED搭載ノートPCがまだ見られない状況のなか、Appleは120Hz実装で競合他社を驚かせた。Appleとそのパートナー企業による問題解決が予想を上回る成果を示したことから、MiniLEDの2021年実績はサプライチェーンの制約を物ともせず、最終的に予測を30%上回った。

DSCC’s Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) reveals OLED vs. MiniLED LCD tablet, notebook and monitor shipments by quarter, brand, size, resolution, refresh rate and many other display related and non-display features as well.

Last week, we released the Advanced Notebook display results and our latest forecast, and not surprisingly, we see massive growth as both OLEDs and MiniLEDs are growing rapidly and have a bright outlook.

Q4’21 was a record quarter for Advanced Notebook displays rising 298% Q/Q and 1717% Y/Y to 4.8M panels. On an annual basis, 2021 was up 629% Y/Y to 8.2M panels. 2021 was 10% higher than predicted as both Apple’s MiniLED MacBook Pro’s and OLEDs outperformed in Q4’21. MiniLEDs surged to a 54% share in Q4’21 and earned a 32% share for the year on Apple’s successful launch of its 14.2” and 16.2” MacBook Pro’s. Apple surprised its competition with the 120Hz implementation with no OLED notebooks yet available at 120Hz. 2021 MiniLED results ended up being 30% above our forecast despite supply chain constraints as Apple and its partners worked through these issues better than expected.

Advanced Notebook Display Shipments by Technology

Looking just at OLEDs, Asus led each quarter of 2021 and is expected to lead in each quarter of 2022. OLEDs came in 3% better than expected in 2021 at 5.5M units. Asus’ unit share is expected to fall from 55% in 2021 to 46% in 2022. In 2021, Samsung was #2, followed by Lenovo. In 2022, we expect Lenovo and Dell to round out the top three.

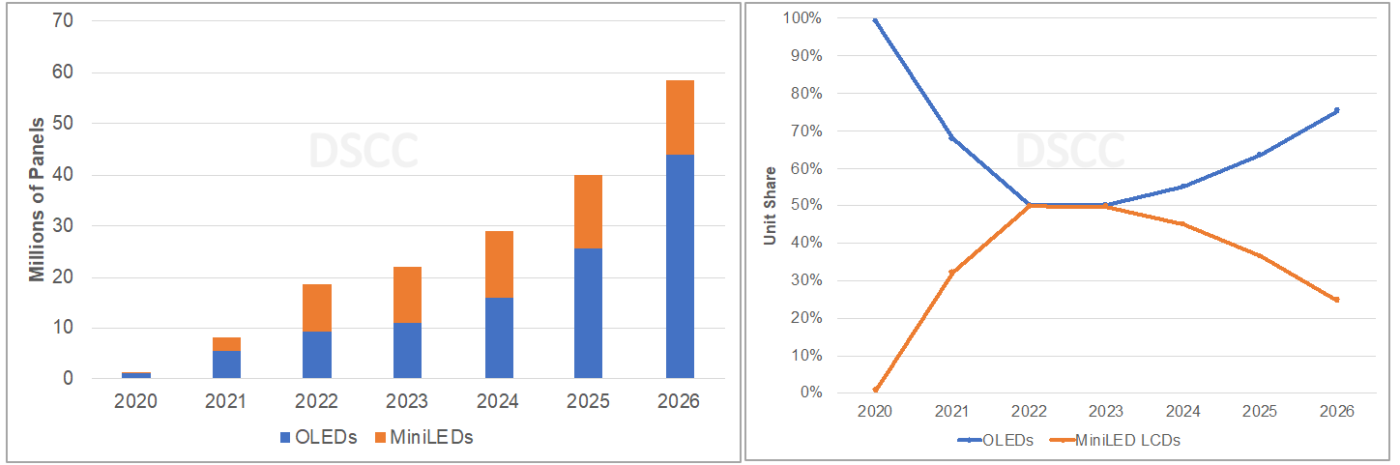

For 2022, we expect Advanced NBs to rise 126% Y/Y to 18.4M units, split 50% for MiniLED and 50% for OLED. Apple is expected to lead this category from Q4’21 to Q4’22 with at least a 41% share on a unit basis and a 56% share on a revenue basis each quarter.

SDC has been the dominant OLED panel supplier with the MiniLED market split between LGD and Sharp and AUO serving other MiniLED brands. SDC led in Q4’21 with a 46% share and is expected to lead in each quarter through Q4’22. On a $US basis, LGD led in Q4’21 and is expected to lead through Q3’22 on higher prices for MiniLEDs than OLED, given Apple’s high-end implementation, with SDC reclaiming the top spot in Q4’22 on higher volumes.

By size in Q4’21, 14.2” MiniLED led with a 28% share followed by 16.2” MiniLED at 26% and 14” OLED with a 17% share. 14.2” and 16.2” are expected to lead each quarter of 2022 as well. On an annual basis, 13.x” led in 2020, 14.x” led in 2021 and is expected to lead in 2022 followed by 16.x”.

Looking forward, we see impressive growth for both MiniLEDs and OLEDs in notebooks with OLEDs eventually gaining the upper hand on enormous capacity coming online targeting the IT market as well as a number of improvements, which will boost the OLED value proposition including:

- Tandem structures which will boost brightness, lifetime and efficiency and lower power consumption;

- A phosphorescent blue OLED emitter which is now expected to hit the market from 2024 which will also boost brightness and efficiency and significantly reduce power;

- Larger G8.5 OLED fabs which will reduce manufacturing costs for larger panels;

- A lower cost IGZO backplane used on G8.5 substrates which will significantly reduce capex per square meter as well as the number of process steps while potentially significantly boosting yields and enabling significantly lower costs at larger sizes;

- Rigid + thin film encapsulation (TFE) substrates which should reduce costs vs. flexible substrates found in mobile displays and offer thinner and lighter solutions than rigid substrates;

- Foldable displays for notebooks on G6 flexible OLED fabs.

MiniLED LCDs also have a significant cost reduction opportunity ahead of them and also benefit from a greater number of suppliers to choose from than in OLEDs. MiniLED LCD costs should fall from:

- Decline in the number of MiniLEDs per device due to efficacy improvements, optical improvements and higher yields;

- Decline in transfer costs from faster transfer equipment with higher yields coming to market in the near future and will also benefit from fewer MiniLEDs per device;

- Lower MiniLED backplane costs from fewer MiniLEDs per device as well as the use of discrete driver ICs should result in simpler PCB backplanes with fewer layers;

- New multi-function optical films are being developed to reduce optical film costs.

Due to the amount of optimized OLED capacity coming online, the cost and performance improvements expected and brands such as Apple eventually migrating from MiniLED to OLED in notebooks, we expect OLEDs to outperform in the notebook market, growing at a 51% CAGR from 2021 to 2026 to 44M units vs. MiniLED LCDs growing at a 40% CAGR to 14M units. OLEDs are forecasted to account for a 76% share of this rapidly growing market in 2026 vs. 50% in 2022. Advanced Notebook displays are expected to grow from a 3% unit and 7% revenue share of the notebook market in 2021 to a 23% unit share in 2026 and a majority of display revenues.

MiniLED LCD vs. OLED Notebook Panel Shipments and Share

For more insights into Advanced Display shipments by brand, size, resolution, refresh rate, backplane, substrate, OLED stack, touch, etc. as well as panel and product roadmap, cost and technology advancements, please see the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) or contact info@displaysupplychain.co.jp.