2023年のOLED出荷額は前年比13%減~IT、スマートフォン、TVの成長で2024年は回復見込み

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

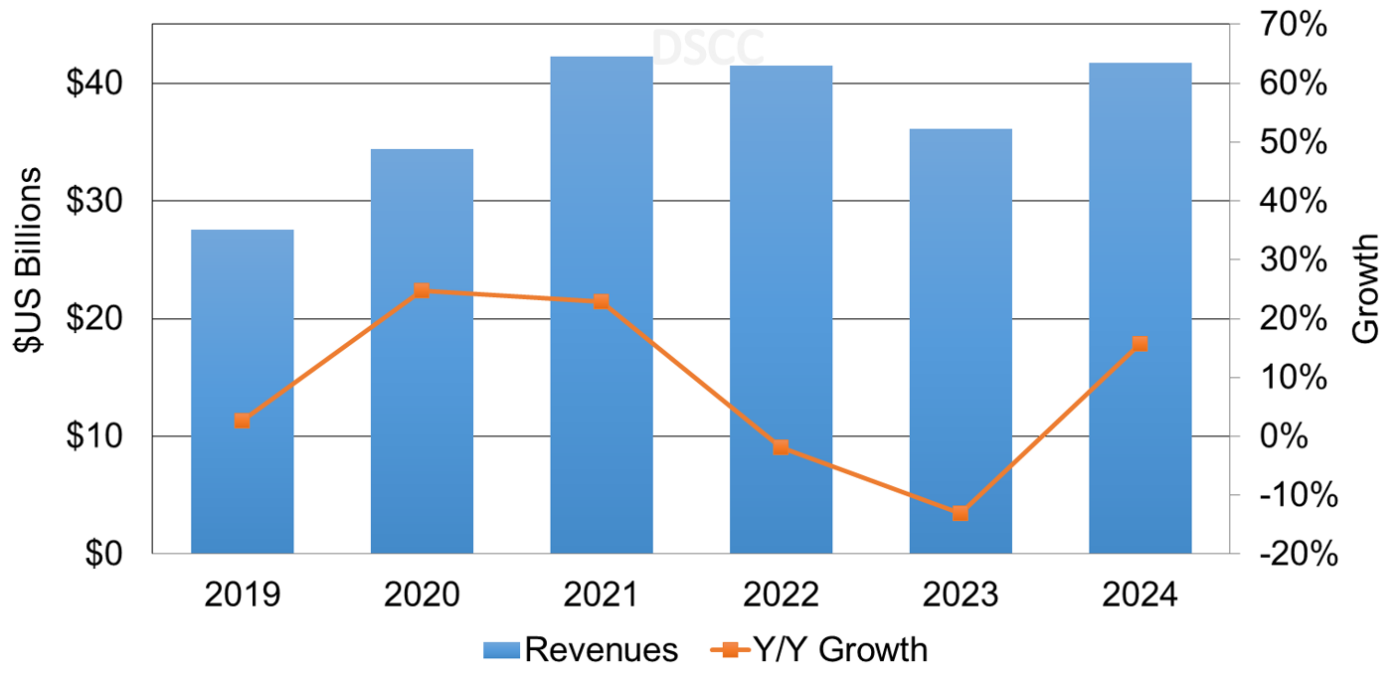

2023年のOLED出荷数は前年比5%減、出荷額は前年比13%減の361億ドルになる見通しだ。DSCCが Quarterly OLED Shipment Report 最新版で明らかにしている。

2023年の主要OLED用途別の出荷状況は以下の通り:

- OLEDスマートフォンの出荷数は前年比横ばい、出荷額は前年比11%減になると予測されている。フレキシブル型の出荷数が前年比14%増、フォルダブル型の出荷数が前年比33%増となるものの、フレキシブル型OLEDスマートフォンのパネル平均価格が2桁の下落となるためである。

- OLED TVは出荷数が前年比31%減、出荷額が前年比28%減になると予測されている。

- OLEDノートPC は、マクロ経済環境や上半期の在庫調整、平均価格の下落などの影響で、出荷数が前年比32%減、出荷額が前年比38%減になると予測されている。

他のOLED用途は2023年に出荷数、出荷額とも増加が予測されている。ここにはAR/VR、車載、モニター、タブレットが含まれる。2024年にはIT用を含む大半の用途で成長が見込まれており、AppleのOLEDタブレット参入によってタブレットは3桁成長、モニターとノートPCでは2桁成長が予測されている。OLEDスマートフォンも前年比で2桁成長が見込まれており、パネル平均価格の下落により、フレキシブル型およびフォルダブル型OLEDスマートフォンがともに2桁成長を示すと見られる。

OLED Panel Revenues to Decline 13% Y/Y in 2023 – Recovery Expected in 2024 Fueled by Growth in IT, Smartphones & TVs

※ご参考※ 無料翻訳ツール (DeepL)

As revealed in DSCC’s latest release of Quarterly OLED Shipment Report, OLED panel revenues are expected to fall by 13% Y/Y in 2023 to $36.1B on a 5% Y/Y panel shipment decrease.

In 2023, by select OLED applications:

- We expect OLED smartphone units to remain flat Y/Y and decline 11% Y/Y in revenues on 14% Y/Y unit increases for flexible and 33% Y/Y unit increases for foldable OLED smartphones with double-digit panel ASP declines for flexible OLED smartphones panels.

- We expect OLED TVs to decline 31% Y/Y in units and 28% Y/Y in revenues.

- We expect OLED notebook PCs to decline 32% Y/Y in units and 38% Y/Y in revenues as a result of the macroeconomic environment, inventory correction in the first half in addition to lower blended ASPs.

We expect other OLED applications to have unit and revenue growth in 2023. These include AR/VR, automotive, monitors and tablets. In 2024, we expect growth for most applications that include IT applications with triple digit growth for tablets as a result of Apple entering the OLED tablet category and double-digit growth for monitors and notebook PCs. For OLED smartphones, we expect double-digit Y/Y growth fueled by double digit growth for flexible and foldable OLED smartphones on lower panel ASPs. Further details can be found in the report.

AMOLED Panel Revenue and Y/Y Growth

In 2023, smartphones are expected to remain the dominant application with an 80% unit and revenue share. OLED smartwatches are expected to remain the #2 application with a 13% unit share, down from 16% in 2022 and a 5% revenue share, down from 6% in 2022. In 2027, on a panel revenue basis, we expect OLED smartphones to decline to a 55% revenue share as a result of gains from OLED notebook PCs, monitors, tablets, AR/VR and automotive applications.

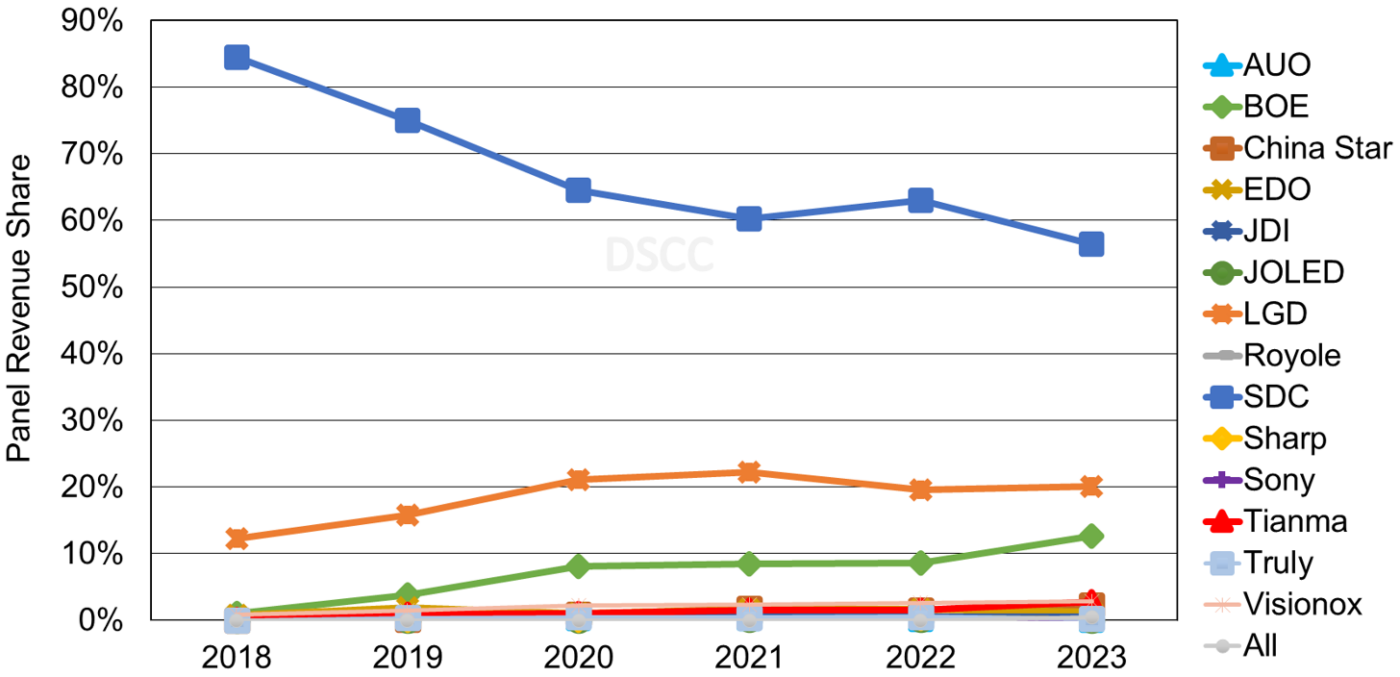

In 2023 for panel revenue by panel supplier for all applications:

- We expect SDC to have the majority panel revenue share as a result of triple-digit Y/Y growth for monitors and double-digit growth for automotive and tablets. As a result of SDC being the only panel supplier providing all four iPhone 15 panels in 2023, we expect SDC to have a 72% share of the iPhone 15 series panel shipments in 2023.

- We expect LGD’s revenue share to increase to 20%. LGD is the panel supplier for the iPhone 14 and iPhone 14 Pro Max. We expect LGD to account for 23% of the iPhone 15 series panel shipments in 2023, up from 17% for the iPhone 14 series as a result of LGD supplying panels for only the LTPO OLED panels for the iPhone 15 Pro and iPhone 15 Pro Max. LGD is also a key panel supplier for the growth areas of monitors and automotive applications. For OLED monitors, LGD is expected to have a 44% unit share, up from 34% in 2022 and a 40% revenue share, up from 30% in 2022. For OLED TVs, LGD is expected to have an 83% unit share and 78% revenue share.

- We expect BOE to be the #3 panel supplier with a 13% revenue share in 2023, up from 9% in 2022. The increase in panel revenue share is the result of a 39% Y/Y unit increase for smartphones and triple-digit growth for automotive applications. For Apple OLED smartphones, BOE provides panels for the iPhone 12, iPhone 13, iPhone 14 and is expected to supply panels for the iPhone 15 and iPhone 15 Plus. In 2023, BOE is expected to have a 16% share of iPhone panel shipments, up from 14% in 2022.

AMOLED Panel Revenue Share by Panel Supplier

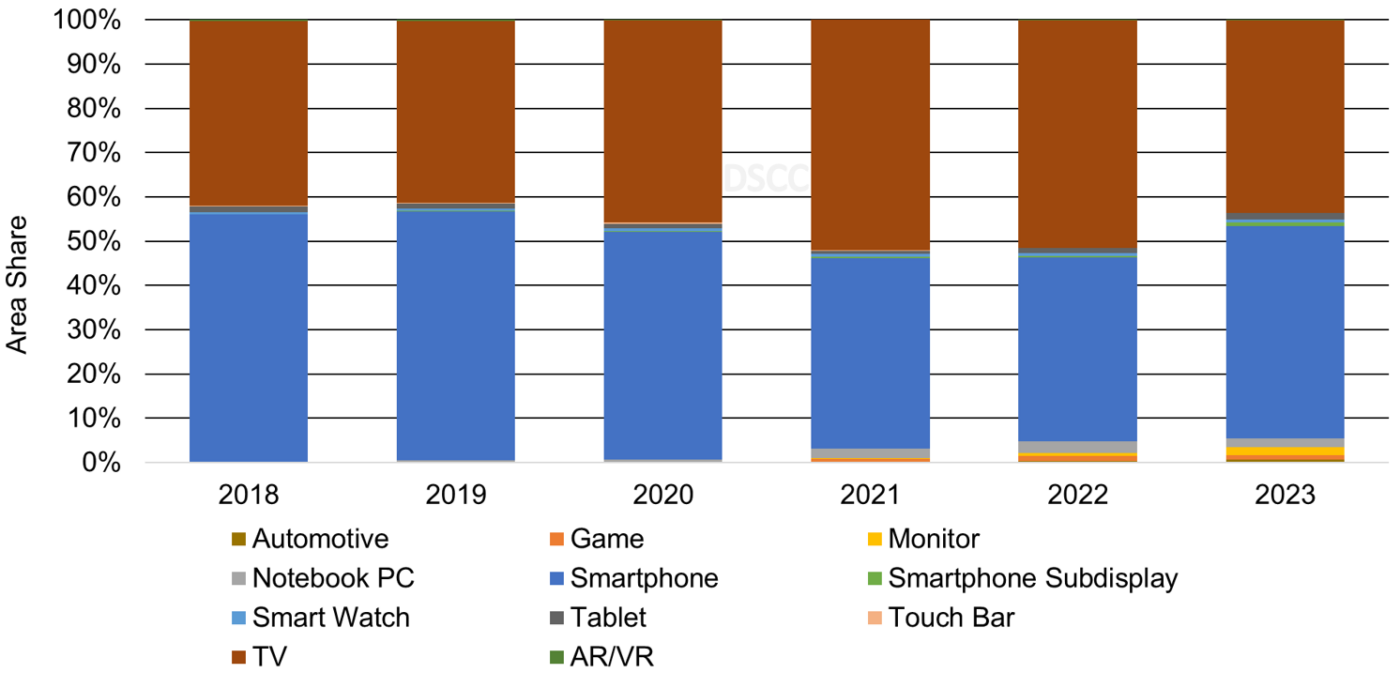

On an area basis, OLED TVs are expected to have a 44% area share in 2023, down from 51% in 2022 as a result of gains from smartphones, automotive applications and monitors. In 2023, we expect OLED smartphones to grow to a 48% area share, up from 42% in 2022 as a result of a 29% unit increase for the 6.6” to 8” category.

Annual OLED Area Share by Application

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。