TV用LCD価格月報~新年に向けて下落継続

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

年末が近づくなか、TV用LCD価格が下落基調を強めている。第2四半期から第3四半期にかけての価格上昇に対応し、LCD生産ライン稼働率も供給が需要を上回る地点まで上昇した。TVサプライチェーンには第4四半期の大商戦を支えるに十分な在庫が蓄積されているため、現在、需給バランスは供給不足から供給過剰へと移行しており、第4四半期はすべての画面サイズで価格が9月のピークから下落、Q1’24も価格は下がり続ける見通しだ。

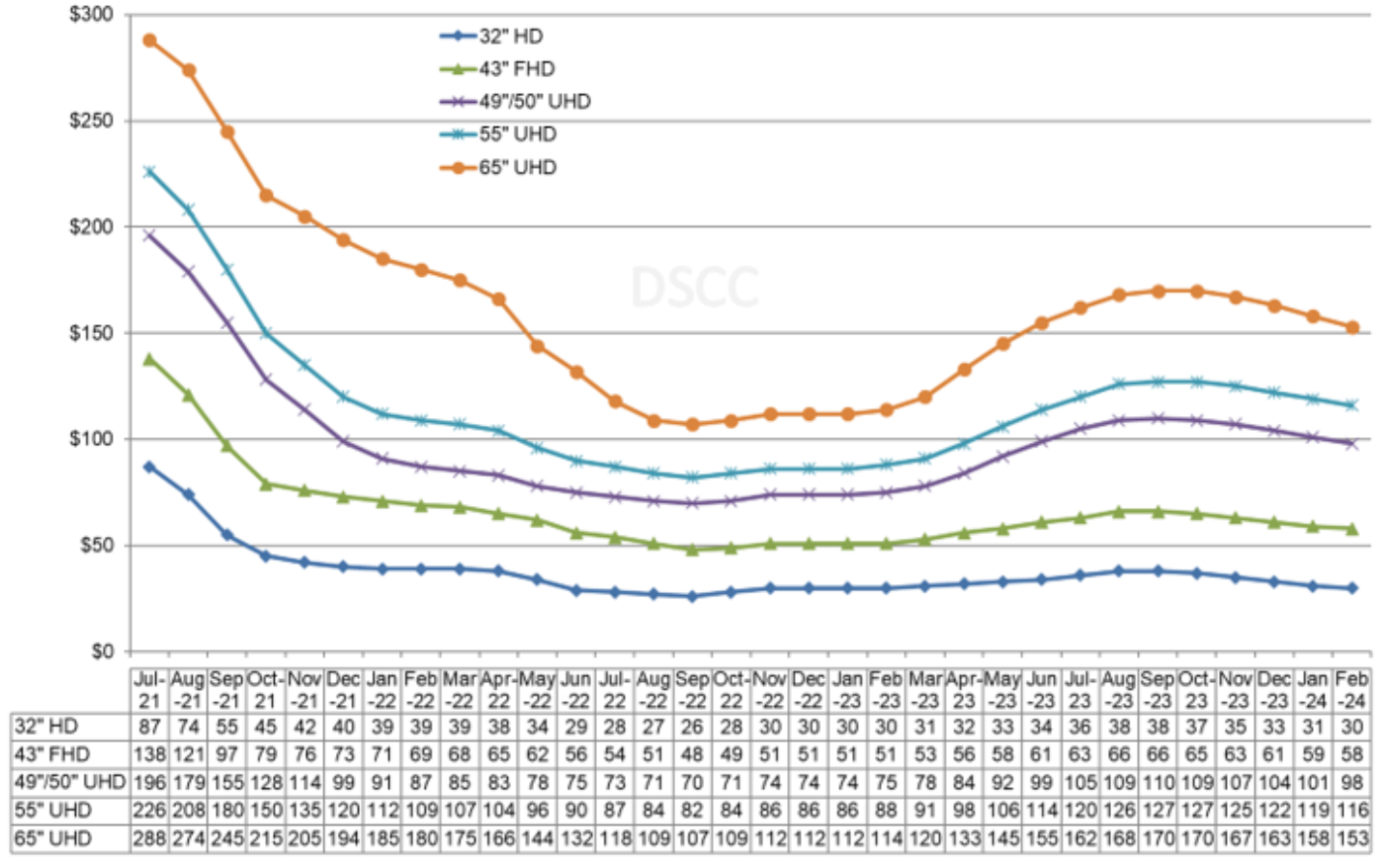

一つ目のグラフは2024年2月までのTV用LCD価格動向の最新予測である。2021年中盤から2022年夏にかけてのパンデミック後の価格急落がグラフに示されている。価格は2022年9月に過去最低値を記録し、Q4’22からQ1’23にかけて緩やかに上昇した後、Q2’23とQ3’23に大幅な上昇を示した。11月の実勢価格はDSCC予測と同等あるいはそれ以下となったため、12月の価格予測は引き下げとなった。価格下落は少なくとも2024年2月まで続くと予測される。

LCD TV Panel Prices Falling as New Year Approaches

※ご参考※ 無料翻訳ツール (DeepL)

As we approach the year-end, LCD TV panel prices are firmly on a downward path. As prices increased during Q2 and Q3, LCD fab utilization increased correspondingly to a point where supply exceeded demand. The TV supply chain has accumulated enough inventory to support the big selling season in the fourth quarter, so we are now seeing a shift in the supply/demand balance from shortage to oversupply, with Q4 prices for all screen sizes coming down from the September peak, and our outlook is that prices will continue to decline in the first quarter of 2024.

The first chart here highlights our latest TV panel price update with a forecast to February 2024, starting with the post-pandemic price plunge, which ran from mid-2021 to summer 2022. Prices hit their all-time lows in September 2022 and increased modestly in Q4’22 and Q1’23 before larger price increases covered Q2’23 and Q3’23. Actual prices for November came in at or lower than our expectation, and we have decreased our expected prices for December. The price declines will extend at least through the first two months of 2024.

LCD TV Panel Prices

After double-digit percentage increases on average for LCD TV panel prices in both Q2’23 and Q3’23. We expect panel prices to decline in the fourth quarter by 2.1% on average, with smaller panels showing larger declines while larger panels will be close to zero change Q/Q.

In the third quarter, price increases were relatively evenly distributed, with all sizes seeing increases between 10% and 18%. The price changes expected in the fourth quarter favor larger panels; although the price for 75” panels has fallen from $248 in September to $245 in November and is expected to fall further in December, the average price for 75” panels in the fourth quarter is equal to the Q3 average. On the other hand, prices for 32” panels will decline by 6% Q/Q in Q4’23.

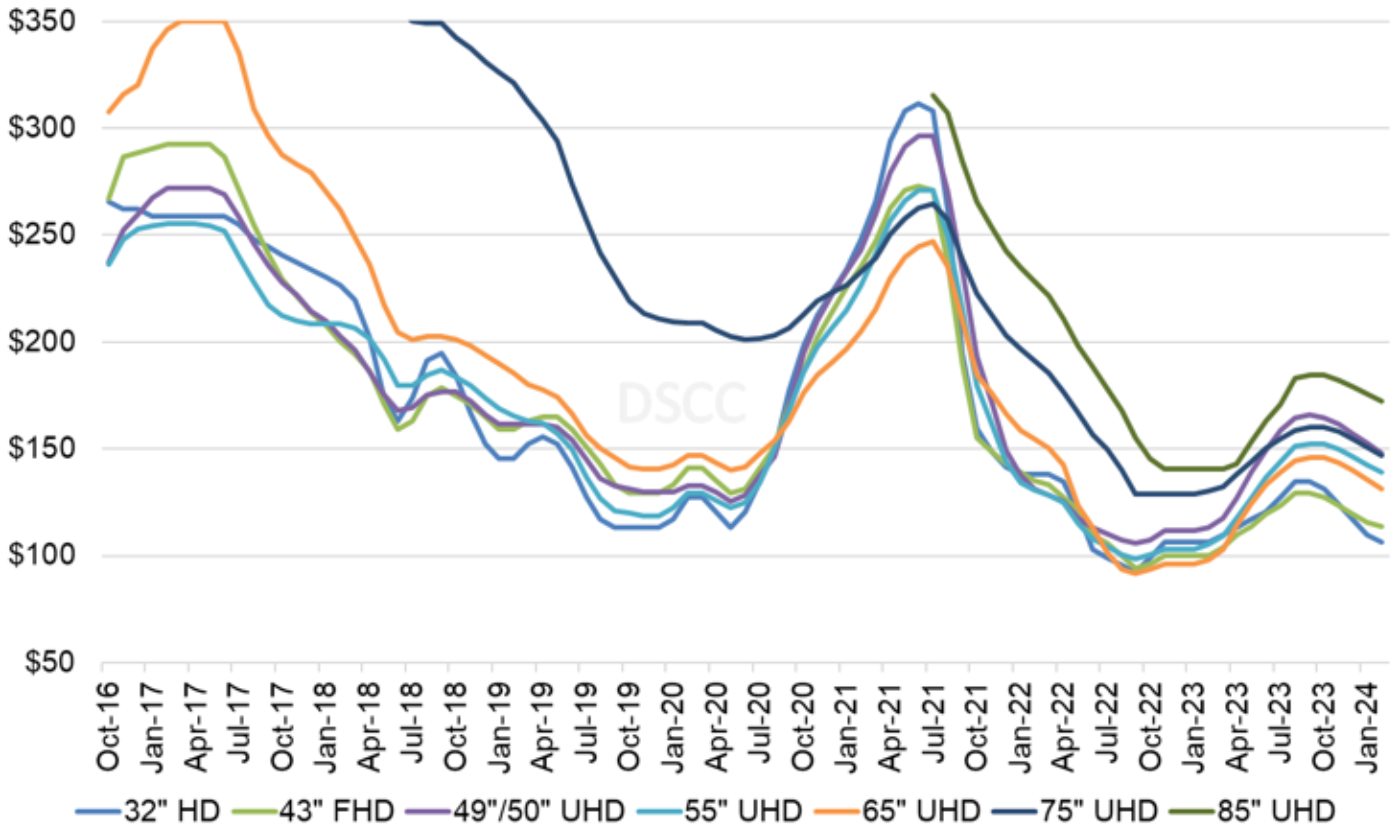

As we look at pricing on an area basis, we are seeing some stratification in the range of prices. From August 2022 through March 2023, the price for 65” TV panels was the lowest in area terms, but the increases in recent months have brought the 65” panels into the mainstream. In December 2023, 32” and 43” panels have the lowest area price at $117 and $120 per square meter, respectively, but area prices go higher for 65” ($140), 55” ($146), 75” ($155) and 49/50” ($157). The current price strata works to the advantage of panel makers with Gen 8.x capacity who can efficiently make 49/50” and 55” panels, and to the disadvantage of panel makers with Gen 10.5 capacity who can efficiently make 65", 75” and 43” panels.

Monthly Area Prices per Square Meter for LCD TV Panels

Prices for the largest screen sizes, 85”, remain at a premium to the smaller sizes, and that premium has been increasing in recent months. In June 2022, 85” panels sold for $188 per square meter, an 83% premium over 32”. The premium hit a low point in March 2023 as 85” panels sold for $141 per square meter, a 28% premium over 32”. Now in December 2023, 85” panels are selling for $179 per square meter, a 53% premium over 32”, and by February 2024 we forecast that 85” panels will sell for $169 per square meter, a 64% premium over 32”.

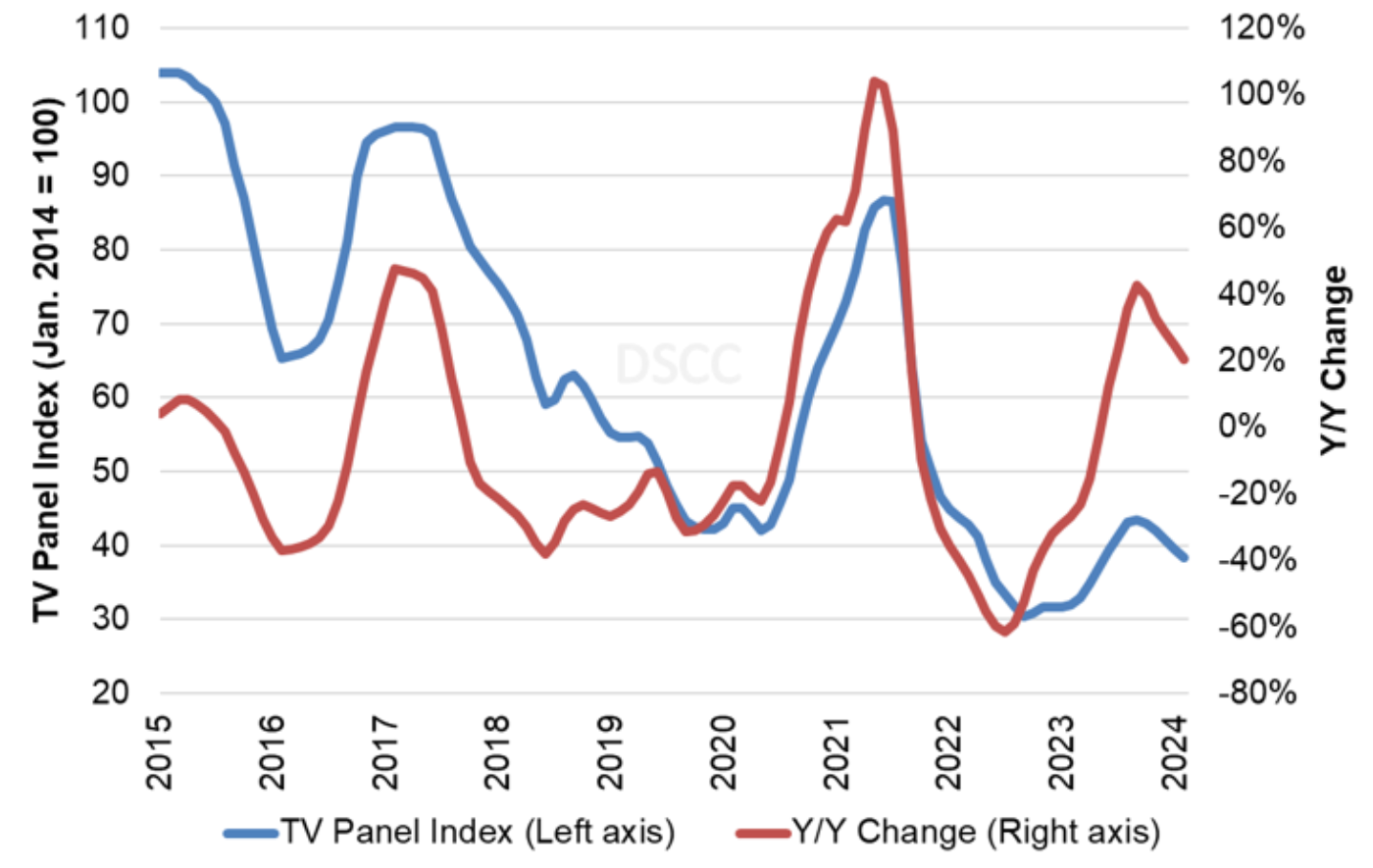

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through February 2023. The price increases in Q3’23 brought our index up to a peak of 43.4 in September 2023, an increase of 42% compared to the low of 30.5 in September 2022. We now expect the index to decline to 40.8 at year-end, which is down 6% from the recent peak but still up 29% Y/Y and up 34% compared to the all-time low. We expect that by February 2024, prices will drop another 6%, which will put them 26% above the all-time low.

LCD TV Panel Price Index

Both of the big Taiwan panel makers reported improvements in profitability in Q3’23 as they enjoyed the improved pricing environment, but both companies still reported net losses. Both companies indicated that shipments would decline in the fourth quarter, which is consistent with the pattern of declining prices. The industry’s capacity still far outstrips the likely demand for the foreseeable future, and high industry utilization in the middle two quarters of 2023 has created a supply glut, which we forecast will result in prices declining through the end of the year and into Q1’24.