AMOLED蒸着材料市場、2027年に27億ドルへ成長。燐光青色材料の最新情報~専門調査レポートが発刊

出典調査レポート Semi-Annual AMOLED Materials Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

AMOLED蒸着材料 (全用途対象) の出荷額は2023年に前年比1%増の17億ドルに到達、2027年には27億ドルに成長し、2023年から2027年の年平均成長率は11%になると予測されている。DSCCが Semi-Annual AMOLED Materials Report 最新版で明らかにした。DSCCのFPD部材担当シニアアナリストであるKyle Jangは「Universal Display Corporation (UDC) が発表通り青色燐光エミッタードーパントの商品化に成功すれば、2027年の出荷額は数億ドル単位で上振れの可能性もある」と述べている。このレポートでは、複数の用途、メーカー間の関係を示すマトリックス図、コスト比較など、AMOLED材料のあらゆる側面を詳細に解説している。

2024年1月発刊のレポートには、AMOLEDの生産能力と稼働率の見通しに関するDSCCの最新予測を収録している。レポートには、業界で蛍光青色発光体の使用が継続すると仮定したベースケースシナリオと、燐光青色がもたらす出荷額追加の概要を示す特別追加シナリオが含まれている。

今回のレポートの最も重要な変更点は、リサイクル材料が含まれるようになったことであり、これによりさまざまな蒸着材料メーカーの量産AMOLED用蒸着材料の市場全体を網羅できるようになった。さらに、材料厚、平均価格、材料使用率について、より現実に即したデータを組み込むことで市場精度が向上しているのが特徴である。

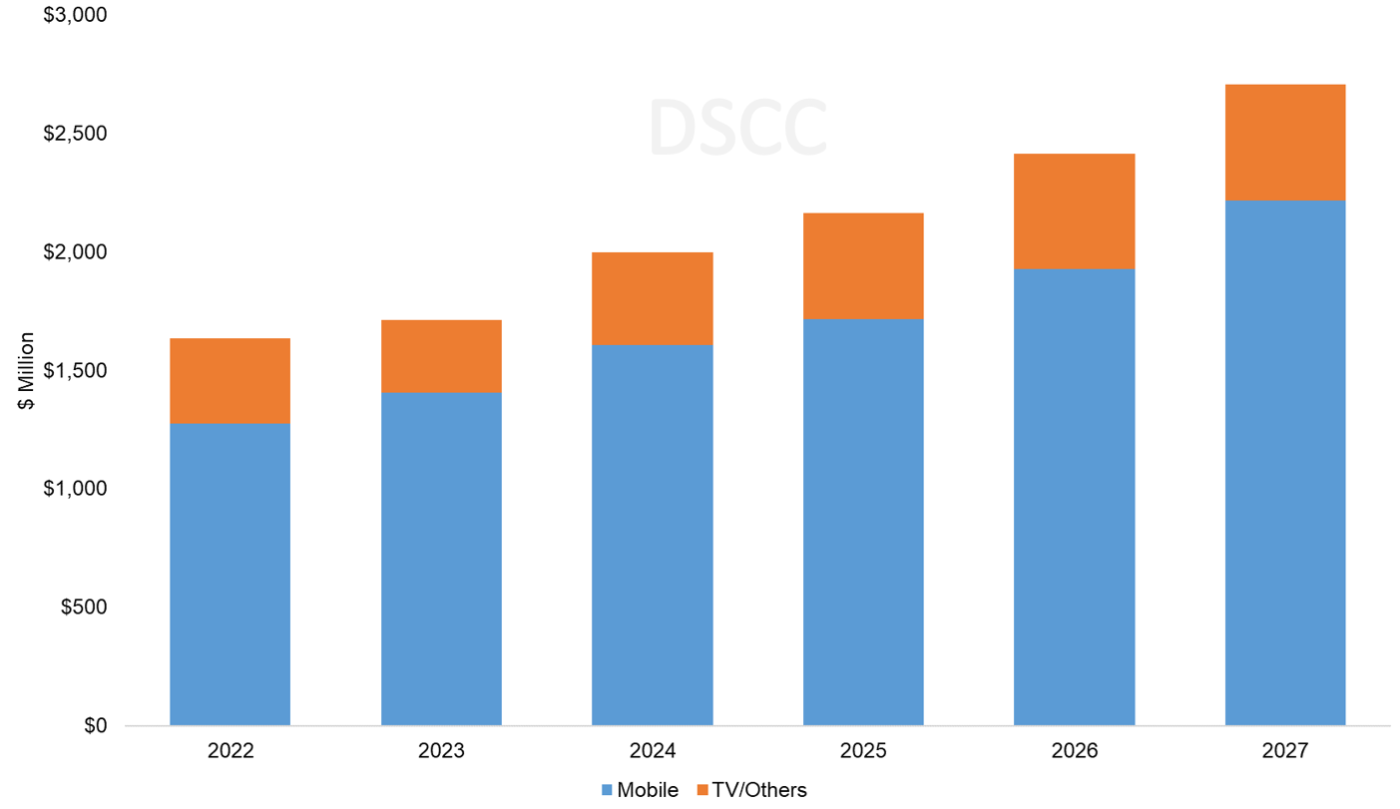

一つ目のグラフは用途別AMOLED材料出荷額予測を示している。TVやその他の大画面用途の出荷額は2023年の3億500万ドルから2027年には4億9200万ドルへ、年平均成長率13%で増加すると予測されている。モバイル用途は今後もOLED材料出荷額の大半を占め、年平均成長率12%で2027年には18億ドルまで成長する見通しだ。IT用途 (タンデム構造) の出荷額は2023年から2027年にかけて年平均成長率79%で増加し、2027年には4億4300万ドル近くに成長するとDSCCは予測している。

AMOLED Evaporation Materials Market to Grow to $2.7B by 2027, Phosphorescent Blue Update

※ご参考※ 無料翻訳ツール (DeepL)

The revenue for AMOLED evaporation materials for all applications is expected to grow 1% Y/Y to $1.7B in 2023 and expected to grow to $2.7B in 2027, an 11% CAGR (2023-2027), according to the latest update of DSCC’s Semi-Annual AMOLED Materials Report. According to DSCC Senior Analyst of Display Components and Materials Kyle Jang, "Revenues can be hundreds of millions of dollars higher in 2027 if Universal Display Corporation (UDC) successfully commercializes a blue phosphorescent emitter dopant, as they have announced. The report details all aspects of AMOLED materials, including multiple applications, supplier matrices and cost comparisons."

The January 2024 report incorporates the latest update to DSCC’s capacity and utilization outlook for AMOLED; both mobile and TV demand have been adjusted slightly compared to our prior forecast. The report includes a base case scenario that assumes the industry continues to use fluorescent blue emitters and includes a special additional scenario outlining the additional revenue generated by phosphorescent blue.

The most significant change in this report is the inclusion of recycled materials, allowing it to encompass the entire evaporation material market for mass production AMOLED from various evaporation materials companies. In addition, it features improved market accuracy by incorporating more realistic thicknesses, ASPs and material utilization.

DSCC's forecast for AMOLED material revenues by application is shown in the first chart here. Revenues from TV and other large screen applications are expected to grow from $305M in 2023 to $492M in 2027, a 13% CAGR. Mobile applications will continue to represent a majority of OLED material sales, growing at a 12% CAGR to $1.8B in 2027. DSCC expects revenues from IT (Tandem structure) to increase by a 79% CAGR in 2023-2027 to nearly $443M in 2027.

AMOLED Material Revenues by Application

The report details the OLED stack configurations of all the major AMOLED product architectures, including Small/Medium panels with single and tandem structures, White OLED (WOLED) by LGD for TV panels and QD-OLED by Samsung. The stack profiles, along with estimates of material thickness, material utilization and material prices form a picture of the unyielded stack cost for each AMOLED product architecture.

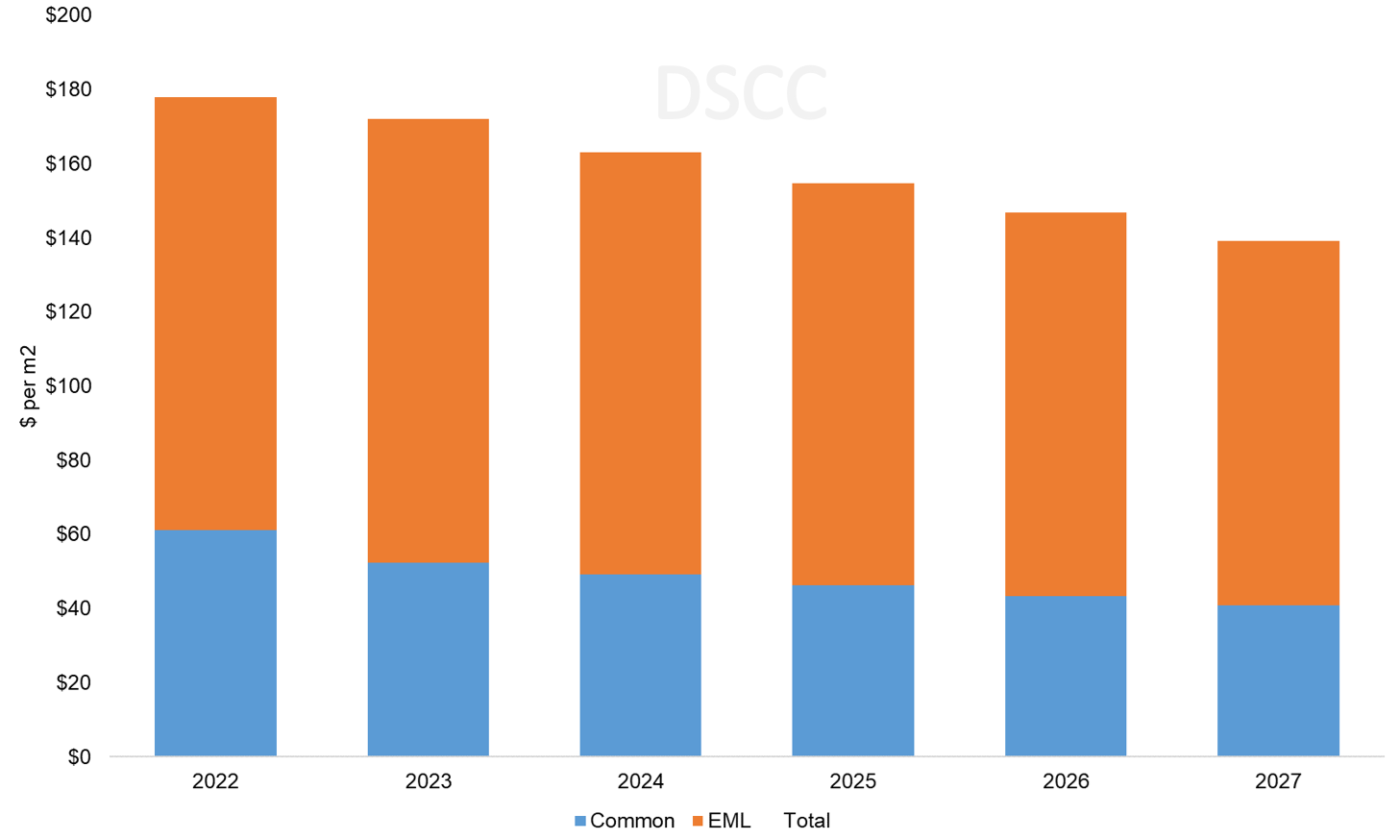

The following chart shows our outlook for the expected material cost for tandem structure OLED panels. DSCC expects that steady, incremental improvements in material utilization and price will help SDC/LGD drive the unyielded stack cost from $172 per square meter in 2023 to $139 per square meter in 2027, an average decrease of 5% per year. In addition, DSCC forecasts that yields will also improve over time with increased experience, resulting in cost reductions for yielded OLED stack materials.

The tandem structure involves the stacking of R/G/B emitting layers twice, with the addition of a charge generation layer (CGL). This results in a cost increase of nearly twice as much compared to the traditional R/G/B single stack. However, efforts are made to optimize optical effects by reducing the thickness of the common layer, designing it to be 1.5 times or less compared to the single-stack thickness. In the future, tandem structures are expected to be the main application for OLED panels in the IT sector, leading to anticipated high growth.

Unyielded Material Cost per m2 for Tandem OLED Panels

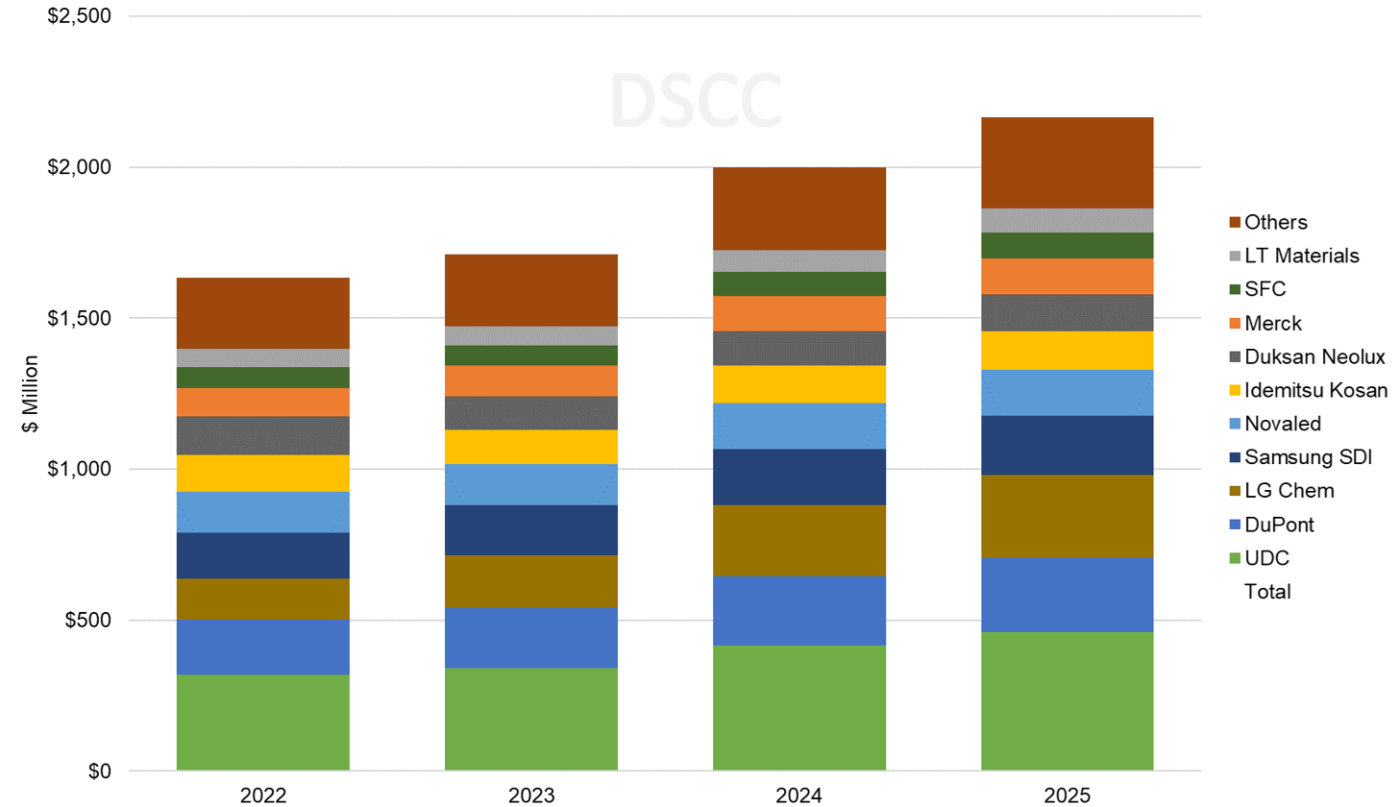

Based on the existing supplier matrix including some shifts in suppliers in 2023, the report includes a projection of AMOLED material revenues by supplier, as shown in the next chart. UDC has been the #1 supplier in revenues for the industry, and DSCC expects that to continue. DuPont, LG Chemical and Samsung SDI hold the number two through four positions among materials suppliers. These four companies are expected to capture 51% of industry revenues in 2023, but as the chart indicates, there is a long tail of companies supplying materials into the industry.

AMOLED Materials Revenues by Supplier

The most recent edition of the report includes a scenario estimating the additional OLED material revenues generated from the potential shift from fluorescent to phosphorescent blue emitters. In February 2022, UDC announced that it was on track to enable the introduction of phosphorescent blue OLED into the commercial market in 2024. UDC has largely confirmed this timeline in subsequent announcements, although at Display Week 2023, UDC clarified that they expect to have a phosphorescent blue that is commercially available in 2024, but that the timetable for devices using the new material would be up to their clients. However, due to lower lifespans of phosphorescent blue, it appears there might be a delay until 2025. Consequently, the transition to phosphorescent is expected to be slower than our previous forecast. Nevertheless, it is evident that if this shift occurs, it will serve as a catalyst for the accelerated growth of the entire OLED industry.

The technology sections have also been updated to align with current development trends and address pertinent issues. DSCC covers various technologies and concerns aimed at enhancing the lifespan and efficiency of OLED panels, with a specific focus on material technology. A key trend in evaporation material is deuterium-substituted technology, which enhances material lifespan by forming stronger bonds with carbon compared to hydrogen. SDC and LGD have adopted deuterium for Green/Blue and have plans to apply it to Red for mobile applications. In the realm of TVs, both companies are adopting deuterium blue, with differences noted by SDC/LGD for other colors. The expected rapid increase in deuterium usage comes with challenges such as IP concerns, limited suppliers and high costs. Beyond deuterium substitution, this report covers a range of technologies, including phosphorescent, TADF, Hyper-fluorescence, Tandem Stack, 4 Stacks, CPL, CoE, MLA and more.

The DSCC Semi-Annual AMOLED Materials Report includes profiles for major panel maker’s AMOLED stack architectures and supply chain including single stack/tandem stack/WOLED/QD-OLED, supplier matrices for the main OLED panel makers and revenue projections for 18 different material types and 21 material suppliers.

出典調査レポート Semi-Annual AMOLED Materials Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。