Advanced (先端技術FPD搭載) ノートPC市場~Q4’22は前期比6%減。2023年は横ばいの予測

[ご案内] 4/11火 TCC品川で開催!DSCC Japan セミナー 2023年前期版~底を脱し上昇に転じたFPD市場を徹底解説!

コロナ禍からの夜明けと共に、いち早く対面式セミナーを復活 (昨年10月) させたDSCC Japanセミナー、ご来場者様からの大歓迎のお声を受けて、今年から通常体制の年2回・品川会場に戻ります!今回もお客様のビジネス戦略をご支援すべく、1日でFPD産業の必聴ポイントを把握できる最新分析データをご提供!みずほ証券・中根康夫シニアアナリスト⇔当社アジア代表・田村喜男の「言いたい放題」オフレコ対談枠も、本セミナーの名物企画として再演決定!徹底的に「ご来場者様満足」にこだわるDSCC Japanセミナーならではのバリューにご期待ください!

冒頭部和訳

DSCCが先週発行の Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) 最新刊にてAdvanced (OLEDおよびMiniLED) ノートPC用FPDの出荷実績と最新予測を明らかにした。Q4’22はAdvanced ノートPC用FPDの出荷数は前期比より減少したが、その要因として、ノートPC市場全体でチャネル在庫とブランド在庫が増加したこと、さらに、長引くマクロ経済の逆風や消費者需要と商業需要の弱体化によって、Advanced ノートPC用FPD市場の成長が減速したことが挙げられる。

Advanced Notebook PCs Decline 6% Q/Q in Q4’22 - 2023 Expected to Remain Flat

※ご参考※ 無料翻訳ツール (DeepL)

Last week, we released the advanced notebook PC display (OLEDs and MiniLEDs) results and our latest forecast in the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします). In Q4’22, we saw a Q/Q decrease of advanced notebook PC displays as a result of elevated channel and brand inventories in the total notebook market and slower growth in the advanced notebook display market as a result of the continued macroeconomic turbulence and the slowing of consumer and commercial demand.

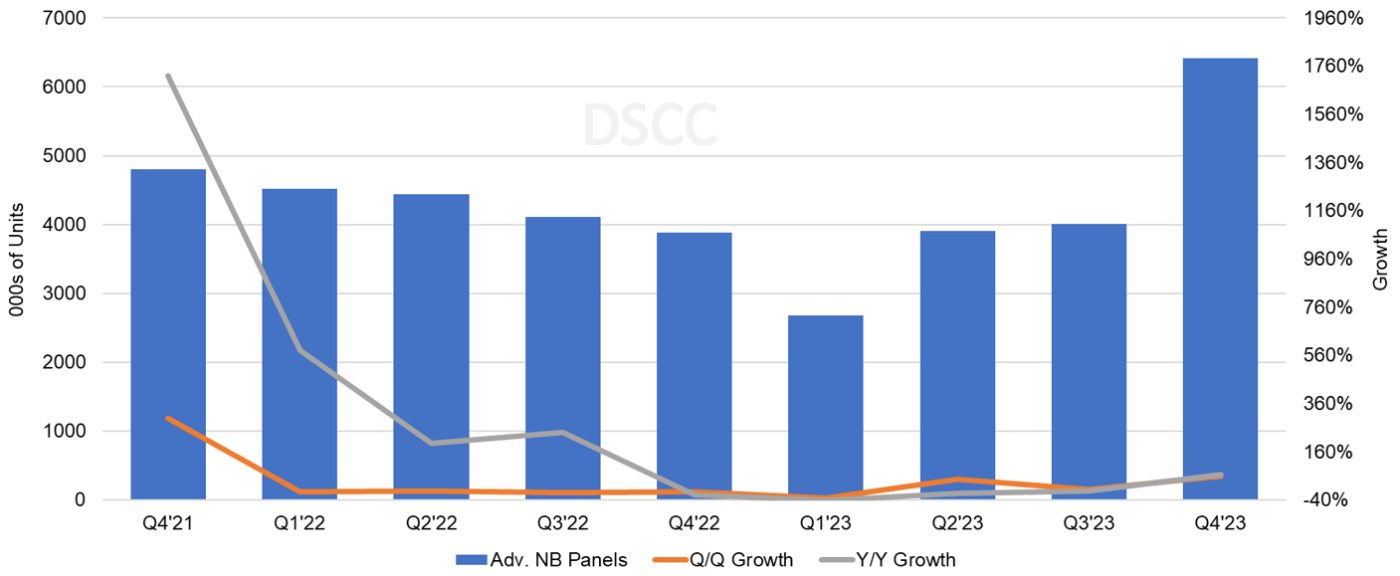

For advanced notebook PC displays, Q4’22 was down 6% Q/Q to 3.8M panels after falling 8% Q/Q in Q2’22. For 2022, advanced notebook PC displays rose 107% Y/Y to 16.9M units with MiniLEDs at a 65% share, up from 32% in 2021 and OLEDs at a 35% share, down from 68% in 2021. The majority share for MiniLEDs is a result of the significant panel shipments for Apple, Acer and Asus. Apple announced the new M2 Pro and M2 Max powered 14.2” and 16.2” in January.

In the recent earnings calls by Apple, Asus, Dell, HP and Lenovo, they all mentioned the challenging macroeconomic environment as a result of faster than expected declines and weaker consumer and commercial demand for the overall PC market. All of these brands noted that they expect an inventory correction by the second half of 2023. From a revenue perspective, these brands reported revenue declines for Q4’22 and all noted that premium products for the gaming and the creative communities softened the decline in revenue. Asus. Dell, HP and Lenovo offer several models of OLED notebook PCs as their premium products. Asus and Lenovo also offer MiniLED notebooks PCs.

Advanced Notebook PC Display Shipments

In 2023, we expect advanced notebook PCs to remain flat with OLED notebook displays increasing 20% Y/Y and MiniLEDs decreasing 10% Y/Y. For OLED notebook PC displays, we expect Asus to lose share, but remain with the majority share as a result of gains from Acer, HP, Samsung, LGE, MSI, Gigabyte and Xiaomi.

SDC remains the dominant OLED panel supplier while the MiniLED notebook PC display market is currently split between LGD and Sharp for Apple products, while AUO, BOE and other panel suppliers provide other brands. In Q4’22, for advanced notebook displays, LGD led with a 40% share followed by SDC with 32% and Sharp with 25%. On a panel revenue basis, LGD led in Q4’22 with a 49% revenue share and is expected to lead through 2022, as a result of the 14.2” and 16.2” Apple MacBook Pro models. In 2022, for the advanced notebook PC category, Sharp had a 36% unit share, followed by SDC with 35% and LGD with 27%. In 2023, we expect SDC to have the majority share as a result of the double-digit Y/Y growth for OLED notebook displays.

Although growth slowed in 2022 versus our previous estimates, we maintain a robust forecast as a result of several G8.7 IT fabs coming online in 2025 – 2026, with the expectation that Apple will enter the OLED notebook PC category in 2024 and continued cost reductions and innovations for MiniLEDs. In 2027, we expect advanced notebook PCs to achieve an 18% and 46% panel revenue share of the total notebook PC market, up from an 8% share and 22% in 2022 on a 31% unit CAGR and revenue CAGR to reach $6.7B in 2027.

This report also includes OLED and MiniLED technology roadmaps and advancements that include:

- OLED technology advancements for IT panels such as:

- OCTA

- Rigid + TFE substrates

- Panel roadmaps

- MiniLED technology advancements

- Wider viewing angles in LED chips

- Optical design trends

- Panel roadmaps

- The latest IT LCD and OLED fab schedules

- MiniLED and OLED panel price forecasts

For more insights into Advanced Display shipments by brand, size, resolution, refresh rate, backplane, substrate, OLED stack, touch, etc., as well as panel and product roadmap, cost and technology advancements, please see the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします).

本記事の出典調査レポート

Quarterly Advanced IT Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。