スマートフォン用OLED出荷分析

冒頭部和訳

DSCCが先日発行した Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) において、減少が予測されるスマートフォン用OLED出荷額についての詳細データとインサイトを明らかにした。スマートフォン用OLED出荷額は2021年の330億ドルから 2022年には320億ドルに、2023年には310億ドルに減少すると予測されている。

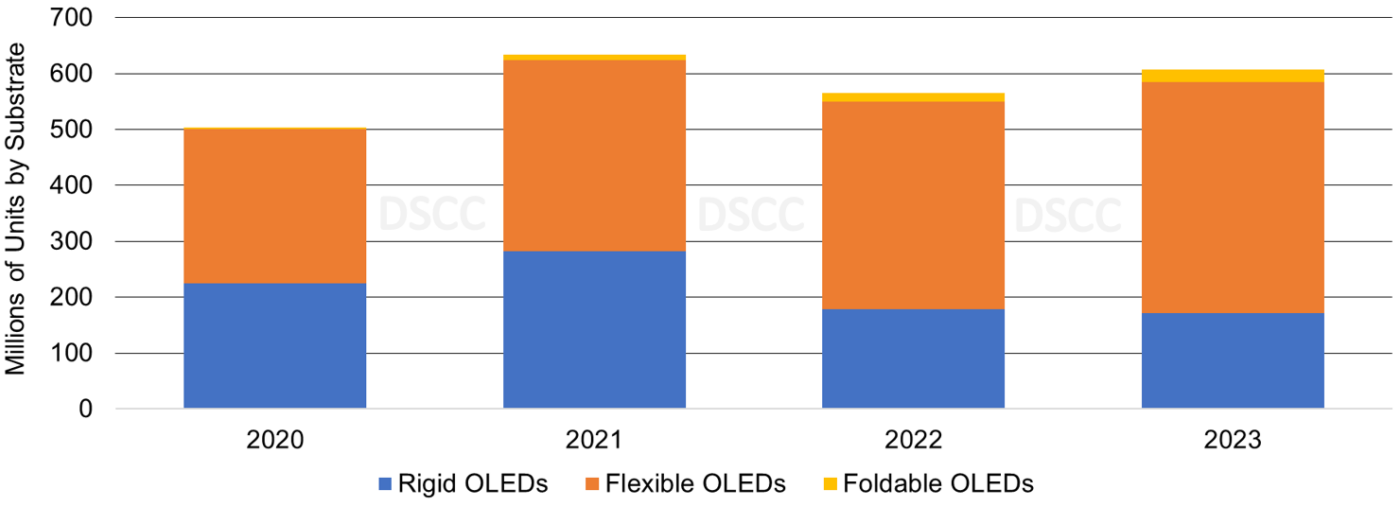

(中略) 2023年のスマートフォン用OLED出荷数は前年比7%増と予測されている。フレキシブル型が前年比11%増で数量シェア68%を獲得、続くフォルダブル/ローラブル型は前年比45%増でシェア4%、リジッド型は前年比4%減でシェア28%となる見通しだ。2023年にはフレキシブルOLEDのASPが前年比3%安、また稼働するフレキシブルOLED生産能力が増える見通しで、どのブランドも1桁または2桁の成長率でパネル調達を増やすと予測される。スマートフォン用フレキシブルOLEDのASPが下がり続けていることから、スマートフォン用リジッドOLEDは前年比2%減の見通しで、複数ブランドがスマートフォン用リジッドOLEDのカテゴリーから完全に撤退し、スマートフォン用リジッドOLEDの余剰生産能力はIT用に転換されることになるだろう。

DSCC Expects OLED Smartphone Panel Revenues to Decline 2% Y/Y in 2023 Despite 7% Unit Growth

※ご参考※ 無料翻訳ツール (DeepL)

In the recently released Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします), we revealed additional granularity and insights for the expected panel revenue declines for OLED smartphones. OLED smartphones panel revenue is expected to decline to $32B in 2022 from $33B in 2021 and to $31B in 2023.

For 2022, we expect OLED smartphone panel shipments to decrease 11% Y/Y to 565M panels. Flexible OLED smartphone panels are expected to increase 9% Y/Y and account for a 66% unit share, up from 54% in 2021. Rigid OLED smartphone panels are expected to decline 37% Y/Y and account for a 32% unit share, down from 45% in 2021. Rigid OLED smartphone panels continue to decline rapidly as a result of several Chinese panel suppliers pricing flexible OLED smartphone panels very close to rigid OLED smartphone panels and several brands significantly reducing their demand versus 2021.

For 2023, we expect OLED smartphone panels to increase 7% Y/Y and flexible OLED smartphone panels to increase by 11% Y/Y for a 68% unit share, followed by foldable/rollable OLED smartphone panels increasing by 45% Y/Y to a 4% unit share and rigid OLED smartphone panels declining by 4% Y/Y for a 28% unit share. In 2023, for flexible OLED smartphone panels, we expect all brands to increase panel procurements by single- and double-digit percentages as a result of flexible OLED panel ASPs declining 3% Y/Y and more flexible OLED capacity coming online. We expect rigid OLED smartphone panels to continue to decline by 2% Y/Y as ASPs for flexible OLED smartphone panels continue to decline, several brands will have completely exited the rigid OLED smartphone category and excess rigid OLED capacity will be used for IT applications.

For 2022, on a smartphone panel revenue basis, we expect rigid OLED smartphone panel revenue to decrease 38% Y/Y for a 13% share, down from 20% in 2021. Flexible AMOLED smartphone panel revenue is expected to increase 5% Y/Y to an 80% revenue share in a smaller market. Foldable AMOLED smartphone panel revenue is expected to increase 35% Y/Y with a 7% revenue share, up from 5% in 2021.

For 2023, we expect smartphone panel revenues to decline 2% Y/Y, with flexible smartphone panel revenues declining 4% Y/Y on 11% Y/Y unit growth, followed by a 41% Y/Y increase for foldable/rollable smartphone panel revenues on 45% Y/Y unit growth. For rigid OLED smartphone panel revenue, we expect panel revenues to decline 14% Y/Y on 4% Y/Y unit declines.

Annual OLED Smartphone Panels by Substrate

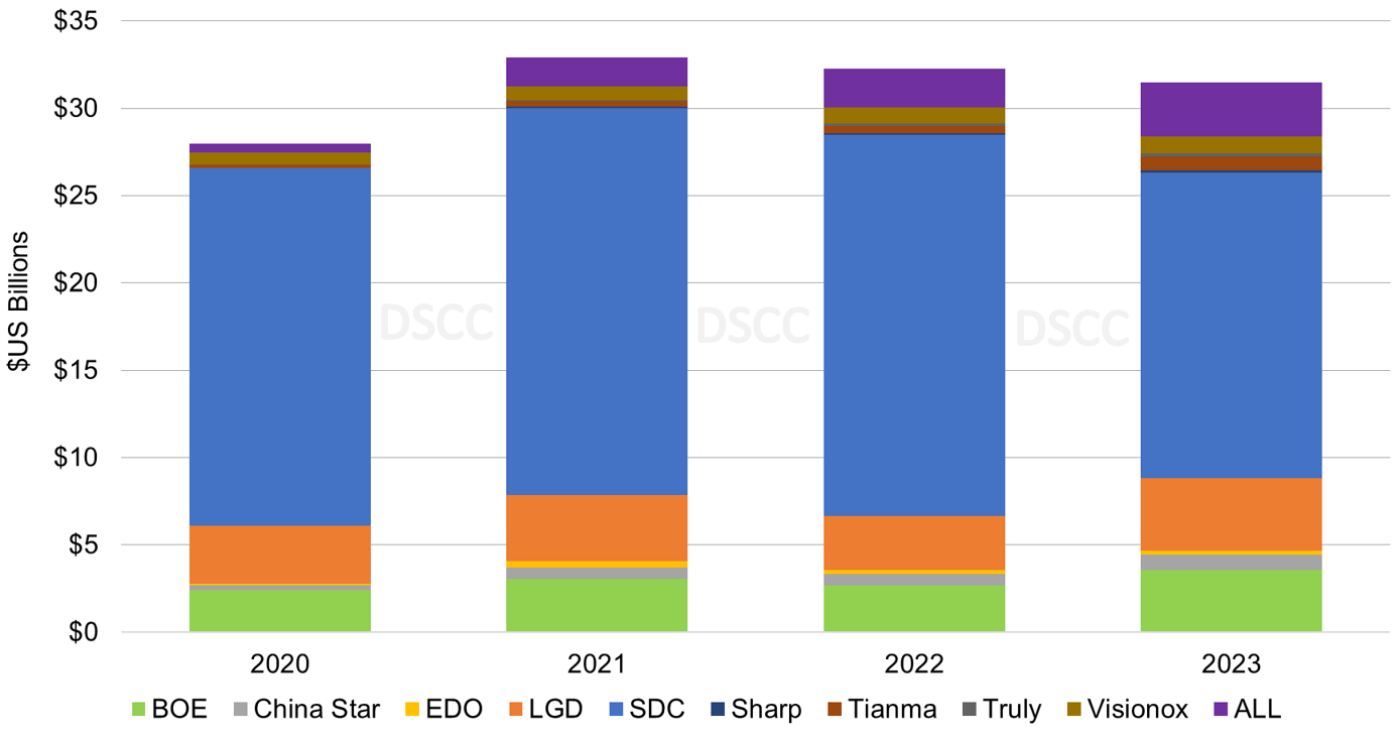

In the case of 2022 panel revenue share by panel supplier, we expect SDC to remain the dominant panel supplier with a 68% share, followed by LGD with 10%, BOE with 8% and Visionox with 3%. In 2023, based on expected panel shipment volumes, we expect SDC to have a 56% panel revenue share, followed by LGD with 13%, BOE with 11% and Visionox and China Star with 3%. We expect LGD to only supply LTPO panels for the Apple iPhone 15 Pro and iPhone 15 Pro Max in 2023.

Annual OLED Smartphone Panel Revenue by Panel Supplier

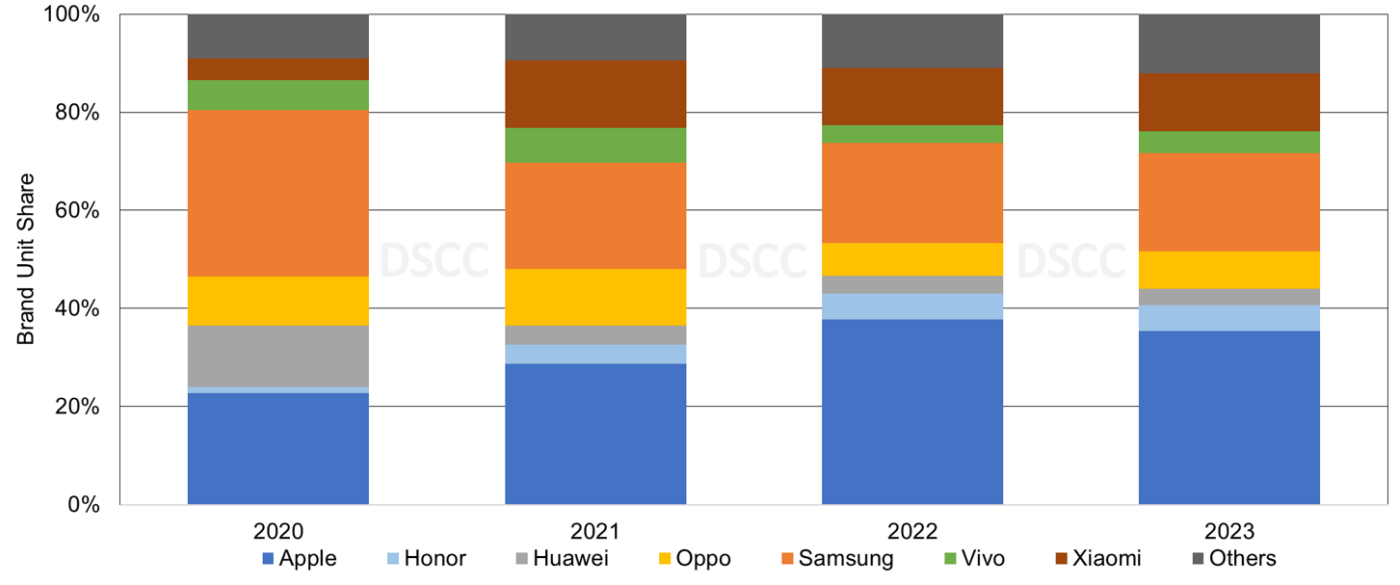

In the case of 2022 smartphone OLED brand share, we expect Apple to have a 38% unit share and a 53% smartphone device revenue share, up from 29% and 41%, respectively in 2021. We expect Samsung to have a 20% unit share and a 21% smartphone device revenue share, down from 22% and 22%, respectively in 2021.

Annual OLED Smartphone Panel Shipment Share by Brand

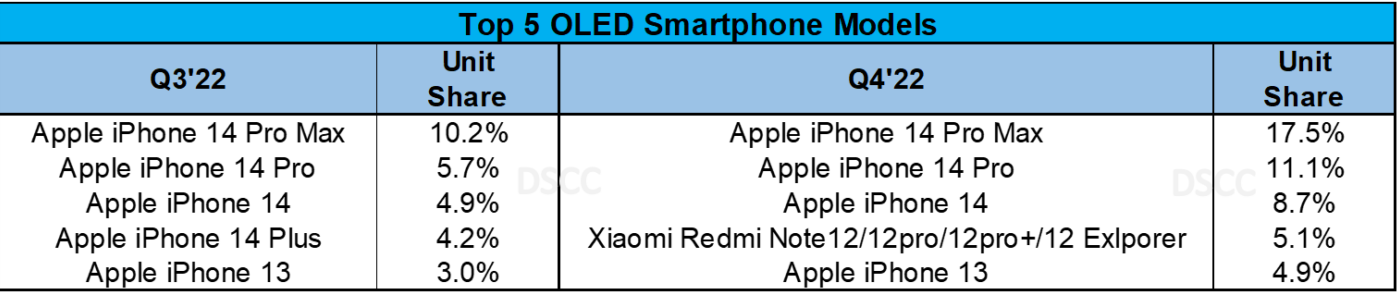

For Q4’22, we expect the top five models to be the Apple iPhone 14 Pro Max, iPhone 14 Pro, iPhone 14, Xiaomi Redmi 12 series and the Apple iPhone 13. These five models are expected to account for a 47% unit share and 62% smartphone device revenue share. For 2022, based on current panel shipments, we expect the Apple iPhone 14 series to account for a 18% unit share of all AMOLED smartphone panels.

Q3’22 and Q4’22 Top 5 Rigid and Flexible OLED Smartphone Panel Procurement by Brand

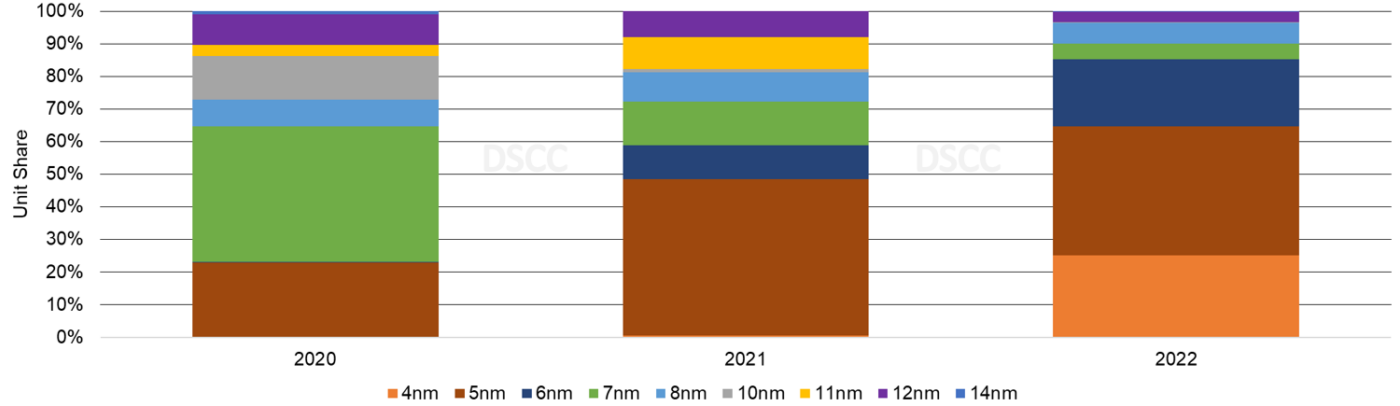

A recent article regarding the use of TSMCs 3nm lithography process was published. One of the many insights of the Advanced Smartphone Display and Technology Report includes the data covering the lithography process on current and future OLED smartphones. In 2022, we expect the 5nm lithography process to have a 40% share, followed by 4nm at 25%. In 2023, we expect Apple to use TSMC’s 3nm lithography process for the A17 Bionic chipset.

Annual OLED Smartphone Chipset Lithography

Readers interested in subscribing to the Quarterly Advanced Smartphone Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) should contact お問い合わせ窓口. This report includes all DSCC’s smartphone data from covering all OLED smartphone and panel shipments by brand, model, all display and major non-display parameters, panel and device revenues and forecasts by quarter and by year through 2027. In addition, it provides insights into technology and innovation trends in OLED display technology, which is applicable to smartphones. There are over 1,100 AMOLED smartphone configurations in our database including variations by substrate, TFT backplane, panel supplier, refresh rate, chipset supplier, 5G networks and much more.

本記事の関連調査レポート

Quarterly Advanced Smartphone Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。