国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 12/20/2021

10 Predictions for the Display Industry in 2021 - How Did We Do?

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

In the first edition of the DSCC Weekly Review in 2021 in January, I continued the tradition started in 2019 of laying out some predictions for the year. With some input from Ross and Guillaume I compiled a list of 10 predictions, and now in this last edition of the year it is time to see how many were right.

#1 – Cease-Fire but No Peace Treaty in US-China Trade War; Trump Tariffs Stay in Place - RIGHT

In January 2021, Donald Trump was still the President of the United States, and Trump’s trade war with China was a major theme of his presidency. When President Biden took office, there was some uncertainty about whether the new Administration would continue Trump’s hard line on China. Now that Biden has been in office for almost a year, it appears clear that the Trump tariffs are here to stay, and if anything, the new President’s stance on China is more severe than his predecessor’s.

After years of complaining about unfair China trade practices, Trump imposed a series of tariffs in targeting US imports of Chinese products. In January 2020, Trump signed an initial “Phase 1” deal that was intended to pave the way for a wider agreement between the two countries. Since then, the pandemic has upended economies around the world and disrupted world trade, but China’s trade surplus with the US is larger than ever. The goals of the Phase 1 deal to reduce China’s trade surplus with the US are in tatters, and there is little talk in the Biden White House of making a Phase 2 deal.

The Trump Administration shifted their focus from tariffs to sanctions in 2020, hitting Huawei with constraints that have effectively crippled its smartphone business and led it to spin off its Honor brand. Biden has taken this approach and magnified it, regularly adding more companies and organizations to the “entity list” that are involved in military technology, 5G, AI, and other advanced technologies. According to Chinese media reports cited by Wikipedia, a total of 260 Chinese entities are on the Entity List. The US added eight companies to the list this week, including semiconductor maker SMIC.

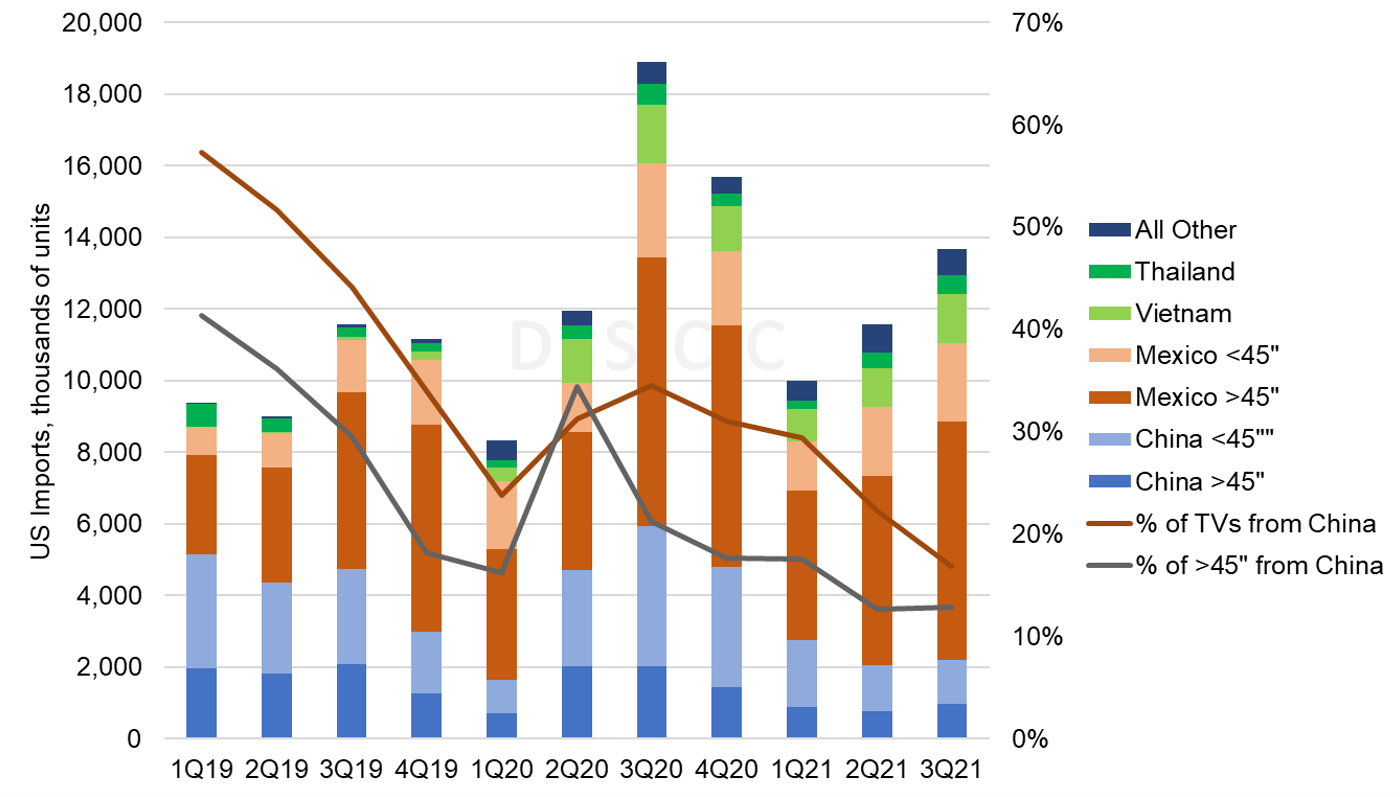

Within display industry end-products, only TVs were affected by Trump’s punitive tariffs. The initial tariff of 15% on Chinese TV imports implemented in September 2019 was reduced to 7.5% in the Phase 1 deal, but that tariff remains in effect, and adds to the 3.9% tariff on TV imports from most other countries. Mexico, under the USMCA deal which replaced NAFTA, can export TVs with no tariffs, and the Trump tariffs helped Mexico recover its share of the TV business in 2020.

As seen in the chart here, before the tariffs were implemented, China’s share of US TV imports exceeded 50% overall, and exceeded 40% on TV sets larger than 45”. After the tariffs were implemented this share plunged, and after a brief surge in mid-2020 when imports from China helped the US supply chain meet pandemic-fed demand, the share of TV imports from China has continued to fall. In Q3 2021 only 17% of US TV imports came from China, including only 13% of 45”+ TVs.

US TV Imports by Country and Screen Size group, Revenues, Q1 2019 - Q3 2021

The main beneficiaries of the trade war are TV assembly factories in Mexico, Vietnam and Thailand. In Q3 2021, TV imports from Mexico were up 38% compared to Q3 2019, while imports from China were down 53%. Over the same time period, imports from Vietnam were up 88% and imports from Thailand up 934%.

While the supply chain of TVs shifted from China to Mexico, the supply chains of notebook PCs, tablets and monitors remained dominated by China. In smartphones, the share of imports from China has varied but China remains the dominant source, with 78% of import revenue in Q3 2021. China’s share of monitors has consistently exceeded 80%, and its share of PCs (notebooks and tablets) remains above 90%.

#2 Samsung Will Sell Foldable Panels with UTG to Other Brands – RIGHT

Up until this year, Samsung has held a near-monopoly on foldable smartphones. In January, we believed that Samsung Display would begin to offer foldable panels with UTG to other customers in 2021, in the interest of broadening the category of foldable phones.

The evidence that we were right in this prediction is right in this week’s newsletter, with Ross’ story on Oppo’s launch of its Find N 5G foldable smartphone with a panel sourced from SDC and UTG cover. Although the line-up of foldable phones with UTG at year-end 2021 is less extensive than we expected – with Google dropping/delaying its plans for a Pixel Fold in 2021 in November, the direction of both the foldable category and SDC’s supply chain efforts remains clear.

According to DSCC’s Quarterly OLED Shipment Report, SDC will supply a total of 8.6M foldable OLED panels in 2021 to all brands.

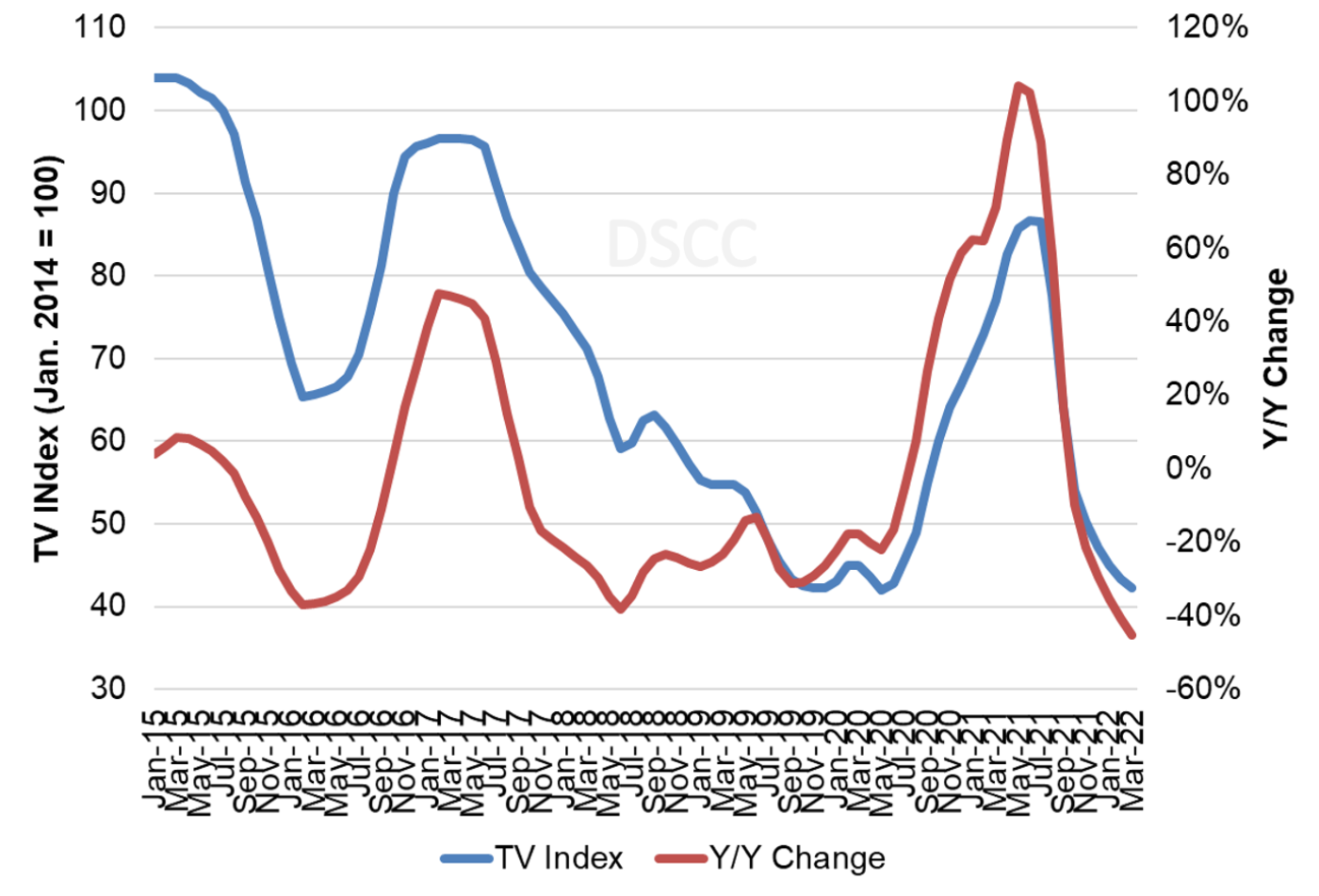

#3 LCD TV Panel Prices Will Remain Higher Than 2020 Levels Until Q4 - RIGHT

LCD TV panel prices represent one of the clearest manifestations of the Crystal Cycle, and the pandemic brought the most severe revolution of the Crystal Cycle in the history of the industry in 2020-2021. The pandemic led to some initial supply shortages, but then it became clear that stay-at-home orders and lockdowns resulted in increased demand for TVs. Prices started to increase in June 2020 and ended the year up more than 50%, but component shortages including glass and driver ICs drove prices up higher through the first half of 2021. Prices peaked at mid-year 2021 at levels more than 100% higher than their all-time low in May 2020, representing the longest and biggest price increases for an up-cycle in the history of the industry.

LCD TV Panel Price Index and Y/Y Change, 2015-2022

The effect of higher prices worked its way through both the supply and the demand sides of the industry. LCD makers rushed to add more capacity and succeeded in doing so. TFT Input for LCD fabs increased 11% Y/Y in Q3 2021, according to DSCC’s Quarterly All Display Fab Utilization Report. At the same time, higher panel prices led to higher TV prices, which suppressed demand (see our prediction #4). After the supply chain restocked inventory, the shortage shifted to oversupply and prices began to fall.

After the longest and biggest up-cycle, the display industry has now seen the sharpest down-cycle in its history in the 2nd half of 2021. Prices fell at double-digit % rates in August, September and October, and by this month they are an estimated 46% down from their peak in June. Panel prices on a Y/Y basis went negative exactly when we predicted: prices were up 17% Y/Y in September but down 10% Y/Y in October. We expect prices to continue to decline into Q1 2022. As for the rest of the new year, look for a prediction in our first edition of 2022.

#4 The Worldwide TV Market Will Decline in 2021 – RIGHT (Preliminary)

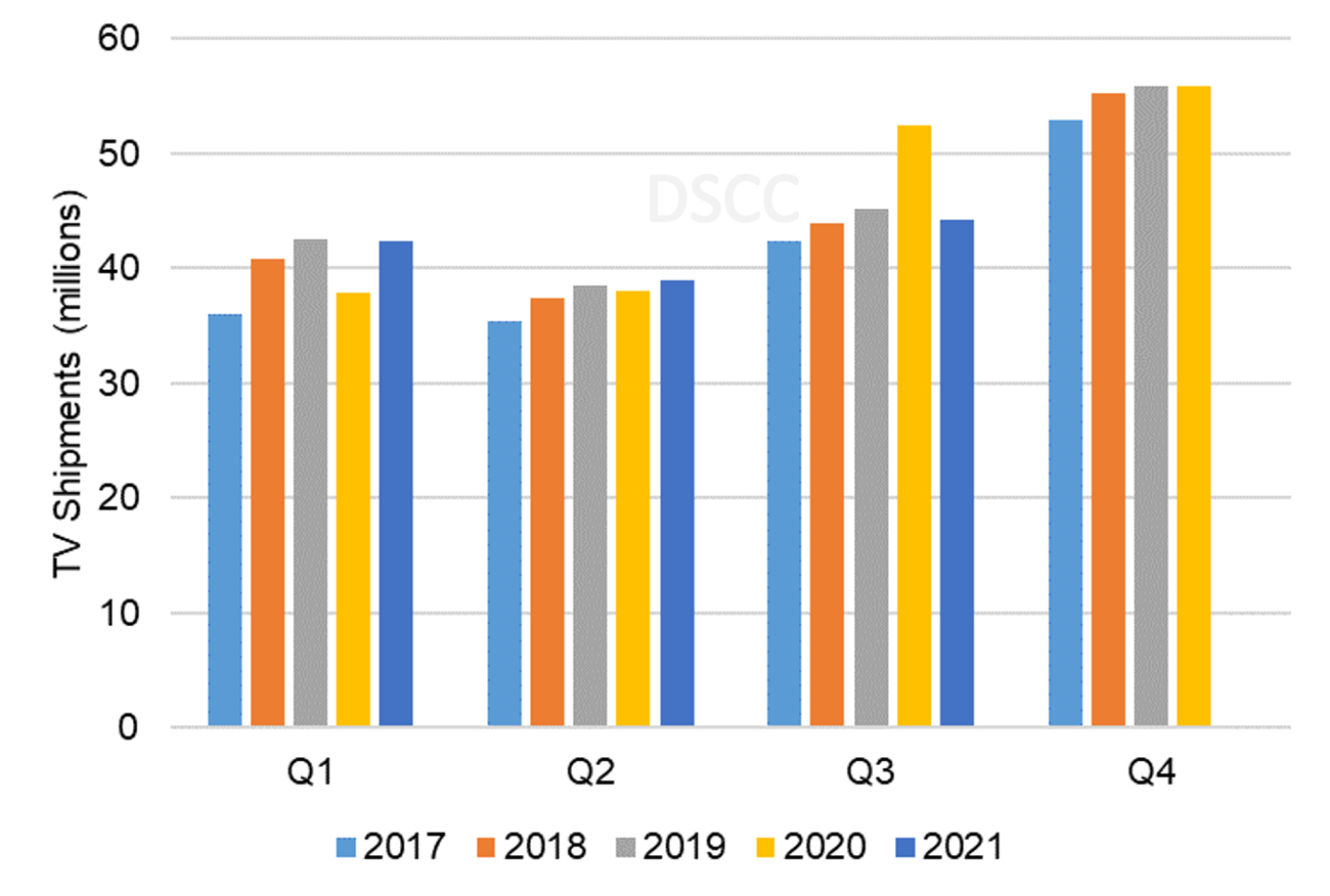

Back in January, we admitted that the data for Q4 2021 will not be available until early 2022, but predicted that it would be clear based on Q1-Q3 data that 2021 is a down year for TV.

The Y/Y numbers for TV started the year on the positive side, based on weak comps as TV shipments in the first half of 2020 were hurt by supply constraints caused by the pandemic and then by fears of demand collapse. We were correct in predicting that Q1 shipments would recover to 2019 levels and would increase by a double-digit % Y/Y. Shipments held up in Q2 but the bottom fell out in Q3 as shown in the next chart here. TV shipments from the top 15 brands in the third quarter were down 16% Y/Y, dropping the year-to-date total into the negative column at -2%.

Global TV Shipments of Top 15 Brands by Quarter, 2017-2020

In January we expressed the hopeful expectation that vaccines would bring an end to the pandemic. While that has certainly not borne out, we were correct in predicting that vaccines would become widely distributed in North America and Western Europe just in time for warmer weather to allow people to go outside. The end of lockdowns led consumers in these developed markets to slow TV purchases starting in Q2.

Meanwhile, demand in emerging economies is much more sensitive to macroeconomics, and the economic slowdown has resulted in declines in TV demand in those regions. On top of the macroeconomic and pandemic effects, higher LCD TV panel prices acted as a headwind on the TV market in 2021, and the panel price declines we have seen in the 2nd half are coming too late to stimulate demand in emerging economies.

According to the latest update to DSCC’s Quarterly Flat Panel Display Supply/Demand Report, we now expect the 2021 TV market will end the year down 3% compared to 2020 at 251M units.

#5 More than 8 Million Devices with MiniLED Will Be Sold in 2021 – WRONG (but close)

We expected that 2021 would be a break-out year for MiniLED technology in multiple applications, and the first indications at the virtual CES show in January were promising, with a big TV launch by Samsung, a new generation by TCL called ODZero, and even a launch by OLED TV leader LG Electronics. In the IT domain, we anticipated the release in early 2021 of Apple’s 12.9" iPad Pro with a MiniLED backlight and expected additional IT products from Asus, Dell and Samsung.

While shipments of MiniLED IT panels have exceeded expectations, on the TV side MiniLED shipments have fallen short, likely hampered by sky-high LCD TV panel prices. At the beginning of the year we predicted more than four million MiniLED TVs would be shipped in 2021, but according to DSCC’s latest Quarterly Advanced TV Shipment and Forecast Report, we now expect MiniLED TV shipments of only 2.3 million, and panel shipments of 2.7 million.

We predicted that MiniLED devices shipments for IT applications (monitors, notebooks and tablets) would total 4 million for the year, and demand for these products is greater than we expected. According to DSCC’s latest Quarterly Advanced IT Display Shipment and Technology Report, we estimate MiniLED panel shipments for IT to total 5.95M for the year, including 3.4M in the fourth quarter. With launch of the Macbook Pro 14 and 16 in October, Apple will account for more than half of the Q4'21 volume.

While the strong IT demand will bring total MiniLED panel shipments to 8.7M for the year, the surge will come too late to get MiniLED devices over 8M. Based on a preliminary estimate of 5.0M IT devices, we now estimate a total of 7.3M MiniLED devices for 2021. While that number falls short of our aggressive prediction, nevertheless it represents growth of more than 1000% in both TV and IT applications. MiniLED clearly will be a force in the display marketplace in the coming years.

#6 More Than $2 Billion Investment in OLED Microdisplays for AR/VR - WRONG

While AR/VR has emerged as one of the hottest topics of the year, and while OLED microdisplays appear to have an inside track to win this application, we got a little ahead of ourselves with this prediction. We had predicted a high level of investment in OLED microdisplay based on some aggressive plans by companies in China.

Several of these investments were delayed or cancelled in 2021, and we estimate investment in OLED microdisplay to total $258M this year, with the largest investment coming from XUS, $191M for a 12-inch R&D facility in Wuxi, Jiangsu, China. One significant plan by Ever Vivid for more than $500M for a phase 2 12-inch line was delayed to 2022 and may be questionable even next year.

Despite more modest investment levels in 2021, we continue to expect substantial investment and growth in OLED microdisplays, based on several public statements:

- Meta (Facebook) said in October that it expected its investment in its hardware division, Facebook Reality Labs, to reduce overall operating profit in 2021 by approximately $10 billion. It is unclear how much of this investment was in display technologies (including Micro OLED), but we can assume it was a sizeable portion.

- Sony is still expected to supply Micro OLED displays for the Apple headset, but we hear that production of the displays has been pushed to the first half of 2022.

- Sidtek recently announced groundbreaking for a 12-inch plant with monthly input of 18K wafers, capable of making 4M displays per year.

#7 MicroLED TV Will Start, But Unit Sales Will be Exceeded By Its Resolution (4K) - RIGHT

In January, we predicted that we would see the first TVs made for consumer use in 2021 and offered this assessment of the technology: “MicroLED TV represents Samsung Visual Display’s ultimate answer to OLED. It can match the deepest black of OLED and offers dramatically better peak brightness. In just about every picture quality attribute, MicroLED represents the perfect display technology. The only problem is the price.”

Indeed, a solution to that problem appears nowhere in sight. We were wrong in predicting that the lowest priced MicroLED models would be offered at less than $100,000 in 2021, and even with a very low unit forecast, we overestimated TV shipments by more than an order of magnitude. According to DSCC’s latest Quarterly Advanced TV Shipment and Forecast Report, we now expect MicroLED TV shipments of only 30 units in 2021, at an average price of $120,000.

In discussions on this technology, I have told people that they will need to wait until the decade of the 2030s to buy a MicroLED TV. Unless I suddenly become friends with a billionaire, that assessment seems right on track.

#8 New LCD Capacity Expansions - RIGHT

After years of oversupply and with the threat of OLED in both smartphones and TV, by the beginning of 2020, it appeared that LCD was “old technology”, and while a few capacity expansion investments were still planned in China, new investment stopped after 2021. During 2020, it became increasingly clear that this assessment was premature, and LCD has a lot of life left.

The longest and biggest up-cycle in the history of flat panel displays brought new life to LCD and very big profits to LCD makers. Consistent with past cycles, these profits have stimulated plans for increased expansion, and those plans remain in place even though LCD panel prices have declined in the 2nd half of 2021.

To assess the magnitude of capacity expansions which have been planned in 2021, we refer to DSCC’s Quarterly Display Capex and Equipment Market Share Report, which provides quarterly updates to our capacity database of every fab in the industry. In our Q4 2020 outlook issued in November of that year, we estimated that LCD capacity would plateau after 2023 at 340M square meters. In our latest view, we expect the industry to continue to grow to well over 400M square meters in 2026, 27% more than a year ago.

This includes major expansions from BOE, CSOT and HKC, which together account for 65M of the increase, but also expansions by AUO, Sharp and even HannStar, which will make its first expansion since 2005.

#9 No Commercially Acceptable Efficient Blue OLED Emitter in 2021 - RIGHT

I started this prediction in 2019, and I’ve been right for three years running.

An efficient blue OLED emitter would be a tremendous boost to the whole OLED industry, but especially to the company that develops it. The main candidate for this is Universal Display Corporation, trying to develop a phosphorescent blue emitter. German start-up Cynora, working on Thermally Activated Delayed Fluorescent (TADF) materials, Japan-based Kyulux and China-based Summer Sprout also target an efficient blue emitter.

UDC’s red and green emitter materials allow excellent color and lifetime with high efficiency, because phosphorescence allows 100% internal quantum efficiency, whereas the predecessor technology, fluorescence, only allows 25% internal quantum efficiency. Because blue is so much less efficient, in White OLED TV panels LGD requires two blue emitter layers, and in mobile OLED Samsung organizes its pixels with the blue sub-pixel substantially larger than red or green.

A more efficient blue would allow LGD to potentially go to a single blue emitting layer, and Samsung to re-balance its pixels, in both cases improving not only power efficiency but also brightness performance. A more efficient blue would hold even greater promise for Samsung’s QD-OLED technology. If the rumors are accurate, Samsung Display’s QD-OLED panels require three layers of fluorescent blue emitters, plus another layer of green emitter to boost brightness. An improvement in blue OLED emitters would provide a big improvement in cost and performance.

UDC has for years worked on developing a phosphorescent blue emitter, but each quarter the company uses identical language in its earnings call about phosphorescent blue: “we continue to make excellent progress at our ongoing development work for our commercial phosphorescent blue emissive system.” Cynora for its part has described its progress in achieving the three goals of efficiency, color point, and lifetime, but that progress seems to have stalled since 2018, and Cynora has shifted its short-term approach to an improved fluorescent blue and a TADF green.

A more efficient blue OLED material may eventually happen, and when it does it will accelerate the growth of the OLED industry, but it didn’t happen in 2021. Read our first issue next year to see what we predict for 2022.

#10 Taiwan Panel Makers Will Have Their Best Year In More Than a Decade - RIGHT

For the two big Taiwan-based panel makers, AUO and Innolux, the pandemic has coincided with a tremendous turnaround in these company’s prospects. At the beginning of 2020, these companies were in dire straits. Both companies were far behind in OLED technology, with little hope of competing with the Koreans, and were unable to match the cost structure of their big Chinese competitors BOE and CSOT. As LCD appeared to be “old technology”, as stated above, these companies appeared to be increasingly irrelevant.

While Taiwan may have missed the boat on OLED, it is a center for excellence in MiniLED technology, and this along with the massive increase in LCD panel prices in the first half of 2021 have greatly improved the prospects for both companies. Perhaps the biggest surprise has been the sustained performance in Q3 and Q4 2021 even while LCD TV panel prices were falling precipitously. While LCD TV panel prices fell by more than 50% between June and November, AUO revenues fell only 9% during that time, and Innolux revenues fell 16%.

Both companies continue to benefit from their diverse product mix – they both excel in IT panels which have continued to see strong demand, and both have strong shares in automotive displays which are not affected by the Crystal Cycle.

The best year for profitability in the last decade for these companies was the last peak of the crystal cycle in 2017. AUO earned a net profit of TWD 30.3B (US$992M) with a 9% net margin, while Innolux earned TWD 37B ($1.2B) with an 11% net margin. Through the first three quarters of 2021, both companies have nearly identical numbers, with net income of TWD 52B ($1.8B) and net margin of 19%. Although the net margin may get pulled down by Q4 results, the strong revenue numbers in October and November show that both companies will finish the year with robust profits.

I count this prediction right because the Taiwan panel makers did have their best year in more than a decade, but this sells the companies short. In 2021 the Taiwan panel makers had their best year ever.

By my count, of the ten predictions we have eight right and two wrong, one of which was close. I am pleased with that result based on some very aggressive predictions. If we get all ten predictions right, we are probably not being bold enough at the beginning of the year.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。