国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 12/13/2021

AMOLED Materials Market to Grow to $2.2 Billion by 2025

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

Sales for AMOLED stack materials for all applications are expected to grow by 32% in 2021 and grow at a 16% annual rate from $1.05B in 2020 to $2.17B in 2025, according to the last update of DSCC’s Biannual AMOLED Materials Report (一部実データ付きサンプルをお送りします). The report details all aspects of AMOLED materials, including multiple applications, supplier matrices and cost comparisons.

This quarter’s report incorporates the latest update to DSCC’s capacity and utilization outlook for AMOLED. We expect that the growth of AMOLED in TV and phones, as well as other applications, will continue to drive material sales.

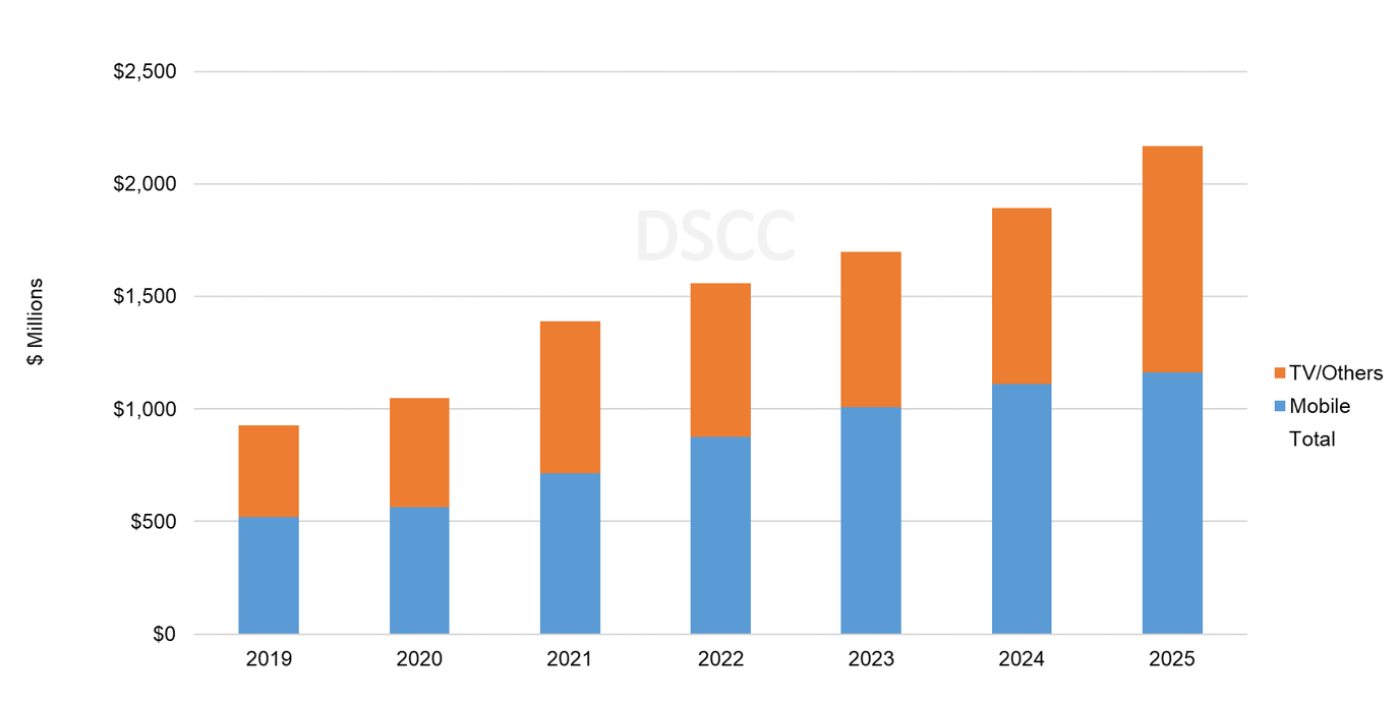

Our forecast for AMOLED material revenues by application is shown in the first chart here. We expect revenues from panels in mobile applications will continue to generate more than 50% of all AMOLED material revenues through 2025. This is mainly because the new capacity for OLED TV, such as QD OLED and inkjet printed OLED will have lower material revenue per panel. While OLED Evo goes in the other direction by adding cost to the OLED stack, we expect that OLED Evo will represent only a small fraction of LGD’s output, rising to 10% in 2025, so the added revenue contribution from OLED Evo will be modest.

We now see the initial plans for FMM VTE RGB OLED fabs being extended to G8.5 for IT markets. This approach will benefit UDC and other VTE materials suppliers since the same materials can be used. Details can be found in DSCC’s Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします). The impact will be higher OLED material revenues for mobile applications compared to our prior view, especially in 2025 as these fabs ramp up.

AMOLED Material Revenues by Application, 2019-2025

The report details the OLED stack configurations of all the major AMOLED product architectures, including Small/Medium panels with RGB pixel structure, White OLED (WOLED) by LGD for TV panels, QD-OLED by Samsung and OLED Evo by LGD. The stack profiles, along with estimates of material thickness, material utilization and material prices, form a picture of the unyielded stack cost for each AMOLED product architecture.

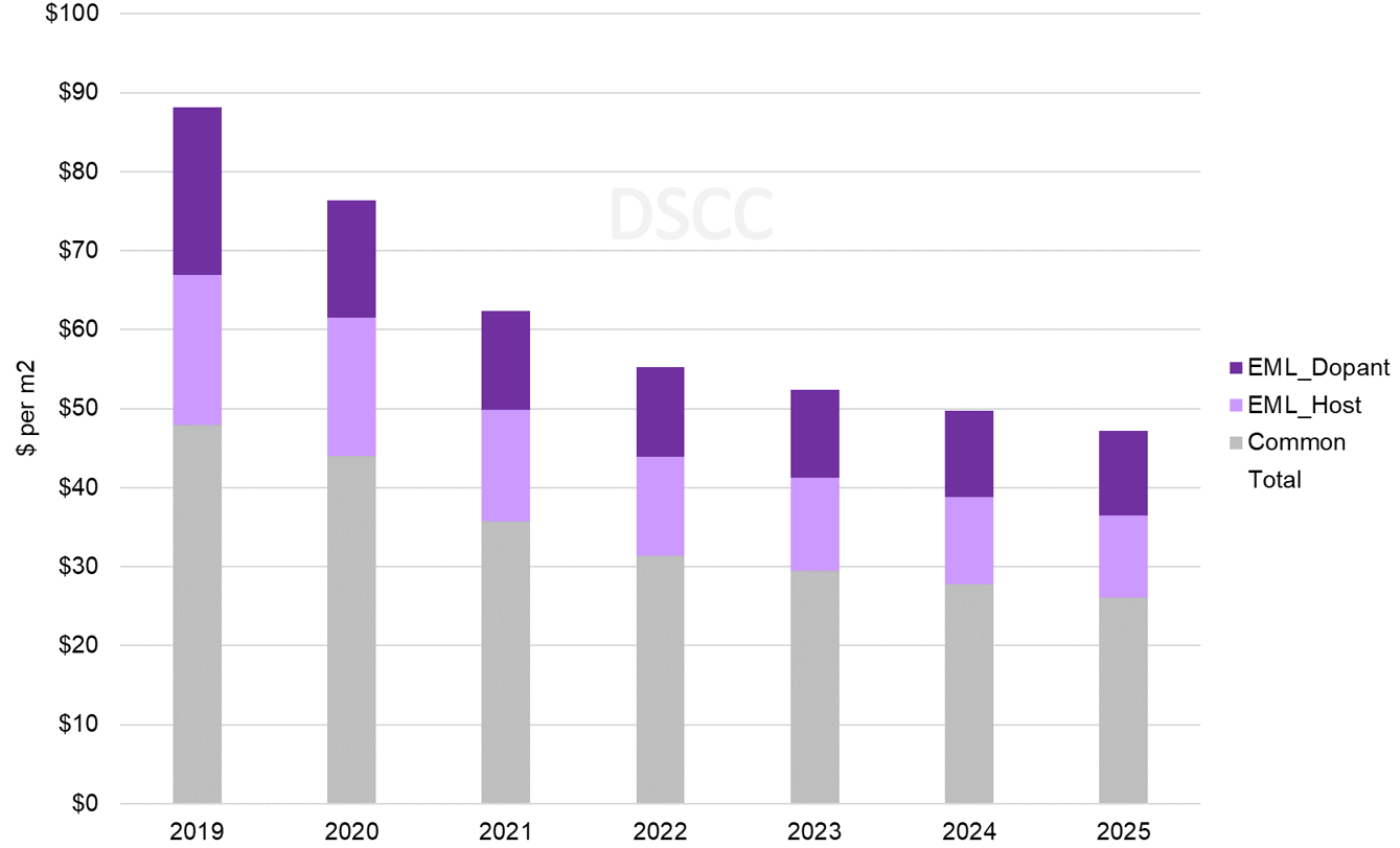

The following chart here shows our outlook for the material cost for LGD’s White OLED panels. We expect that steady, incremental improvements in material utilization and price will help LGD drive the unyielded stack cost of its standard WOLED panels from $76.32 per square meter in 2020 to $47.19 per square meter in 2025, an average decrease of 10% per year. For LG Display, with increased volume and experience we expect that yields will also improve over time, so that the cost declines of yielded OLED stack materials will be even greater.

With the additional emitting layer, we estimate that the unyielded stack cost of the OLED Evo panel adds about $13 per square meter in cost. Although this figure also declines over time, we estimate the cost adder in 2025 remains more than $10 per square meter. With this continuing cost adder, we expect that OLED Evo will continue to be positioned as a premium product, and that the additional green layer will not be used on LGD’s mainstream products.

Unyielded Material Cost per m2 for WOLED Panels

Our report provides an estimate of AMOLED stack material costs QD-OLED, which we expect will be substantially lower than those for WOLED. When QD-OLED is introduced starting early next year, its unyielded stack costs are expected to be ~25% lower than the standard WOLED. If an additional green layer is used as has been rumored, the QD-OLED stack cost would be higher. Of course, for QD-OLED, the unyielded stack cost is only a part of the picture. The yields on the mature WOLED technology will certainly be higher than those for QD-OLED, and we expect that the front end of the QD-OLED display includes both a color converter and a color filter, and therefore will be substantially more expensive than the color filter used in WOLED. While we expect the OLED stack cost of QD-OLED to be lower than that of WOLED, we expect the total product cost of QD-OLED to be higher.

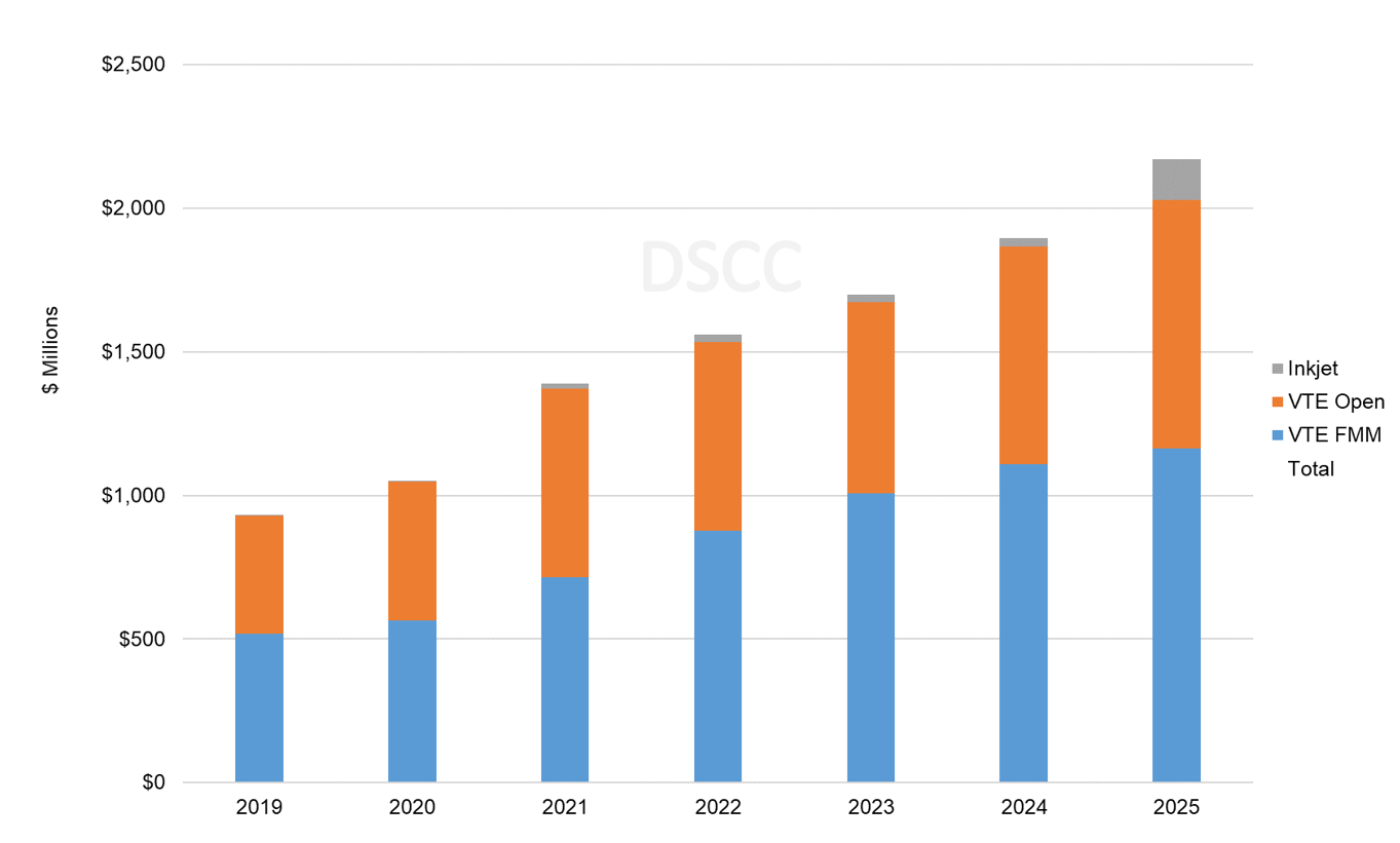

With CSOT’s planned investment in a Gen 8.5 AMOLED fab using inkjet printing with production starting in 2025, the revenues for soluble materials for inkjet printed OLED will increase rapidly in 2025. Nevertheless, the AMOLED materials market in terms of overall revenues will continue to be dominated by evaporated materials, and this dominance will be accelerated by additional RGB FMM VTE Gen 8.5 fabs for IT and possibly TV eventually. Evaporated materials will remain the only type used for smaller AMOLED panels for smartphones and will continue to dominate the market for OLED TV panels. We expect revenues from soluble materials for inkjet printed OLED will grow from less than $1M in 2019 to $142M in 2025, when they will represent 14% of the TV/Other segment but still only 7% of the overall AMOLED materials market.

Material Revenues by Deposition Type, 2019-2025

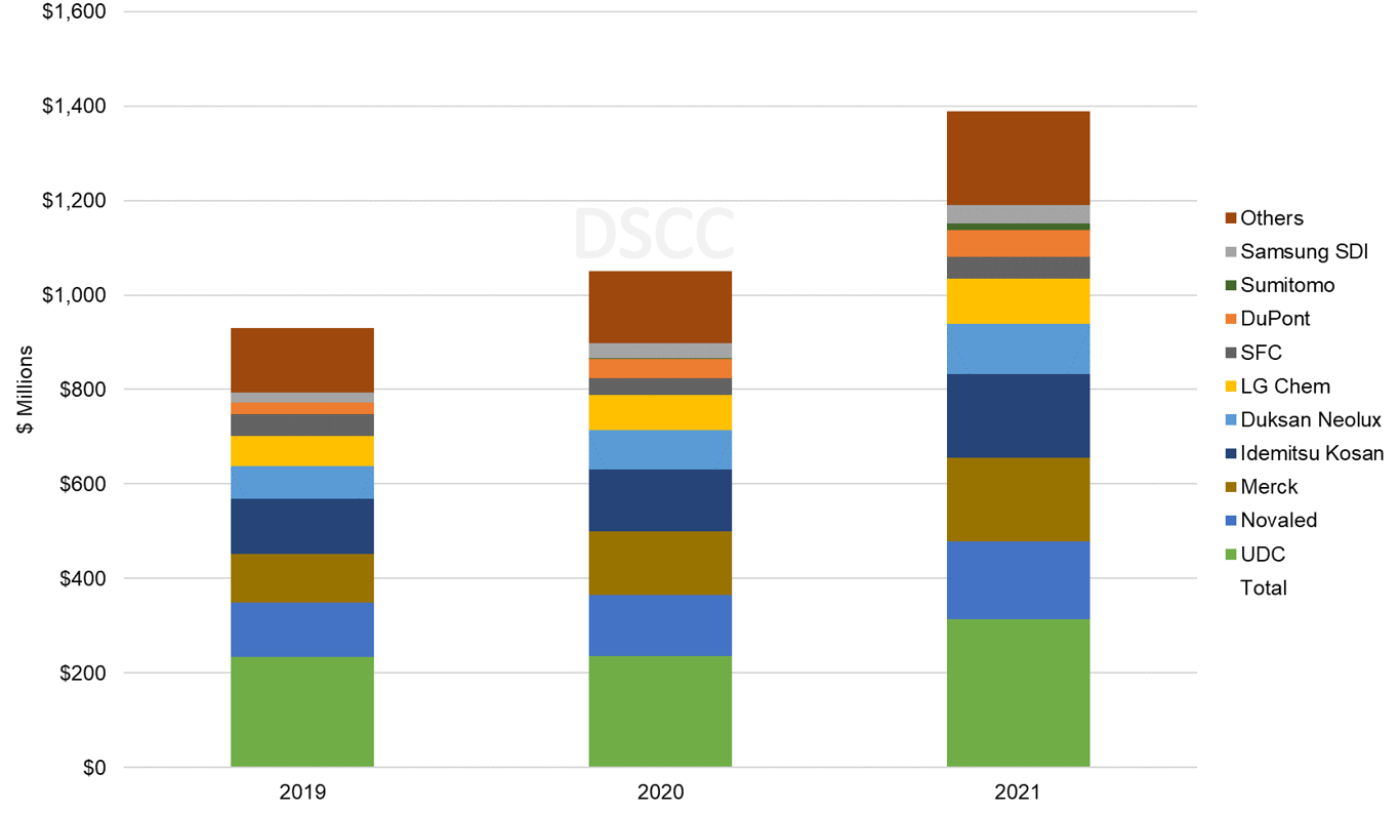

Based on the existing supplier matrix, the report includes a projection of AMOLED material revenues by supplier, as shown on the next chart. Universal Display Corporation (UDC) has been the #1 supplier in revenues for the industry, and we expect that to continue. Idemitsu Kosan, Novaled and Merck hold the number two through four positions among materials suppliers. These four companies are expected to capture 60% of industry revenues in 2021, but as the chart indicates, there is a long tail of companies supplying materials into the industry.

AMOLED Materials Revenues by Supplier, 2019 – 2021

The DSCC Biannual AMOLED Material Report (一部実データ付きサンプルをお送りします) includes profiles for all major AMOLED stack architectures, supplier matrices for the main OLED panel makers and revenue projections for 18 different material types and 20 material suppliers. For 2022 we will transition this report from quarterly to semi-annual and the report will have a reduced price. For more information about the report, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。