国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 11/08/2021

DSCC Raises Display Equipment Spending Forecast on IT Opportunity

Ross Young, Founder and CEOAustin, TX USA -

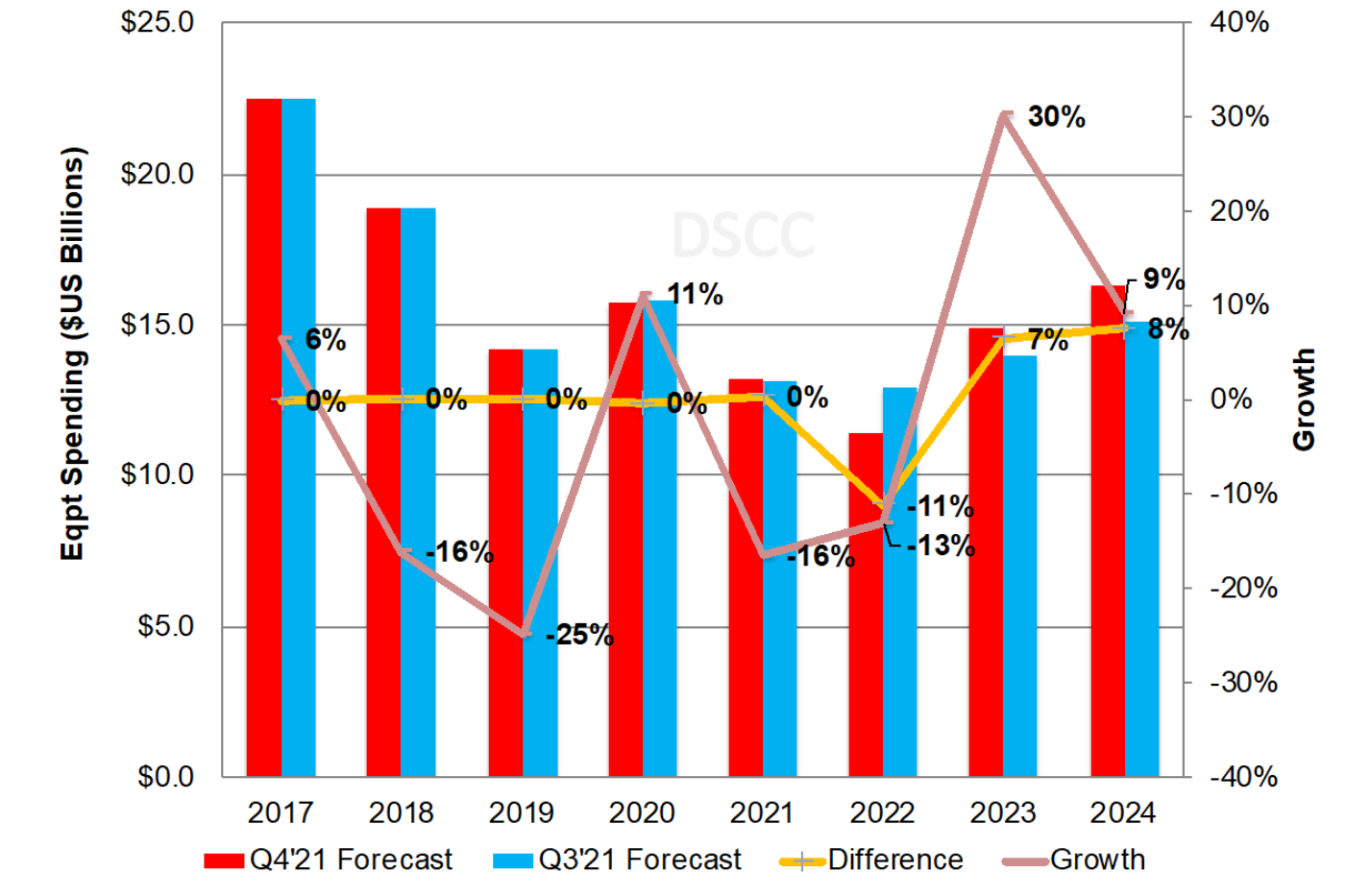

DSCC has increased its 2020-2025 display equipment spending forecast by 2.3% vs. last quarter to $80.7B, helped by rising OLED spending in Korea targeting the IT market, as revealed in the latest issue of its Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします). In 2022, spending is forecasted to fall by 11% vs. last quarter due to a delay at a Chinese mobile OLED supplier, which will boost 2023.

DSCC’s Display Equipment Spending Forecast (Delivery Basis)

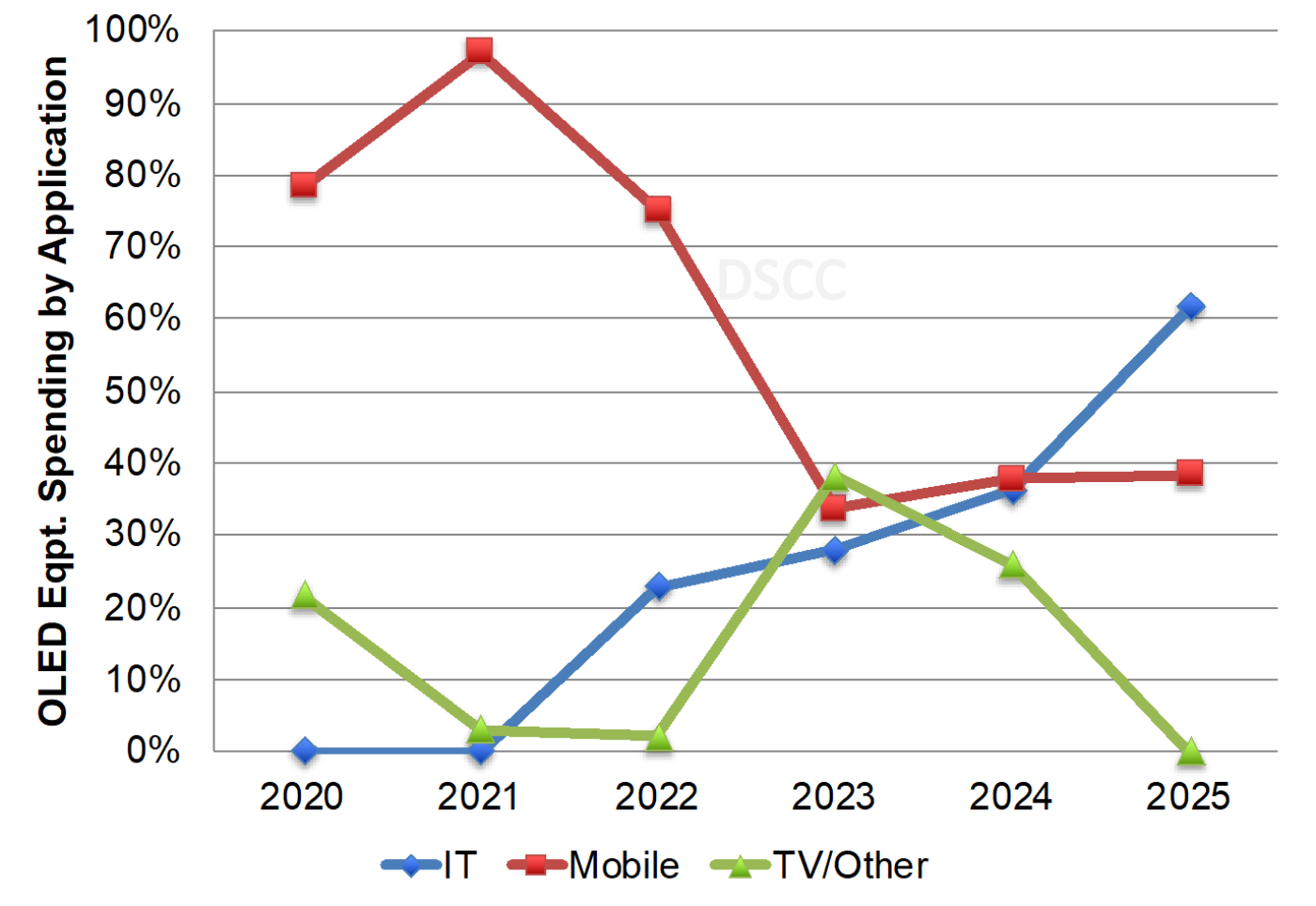

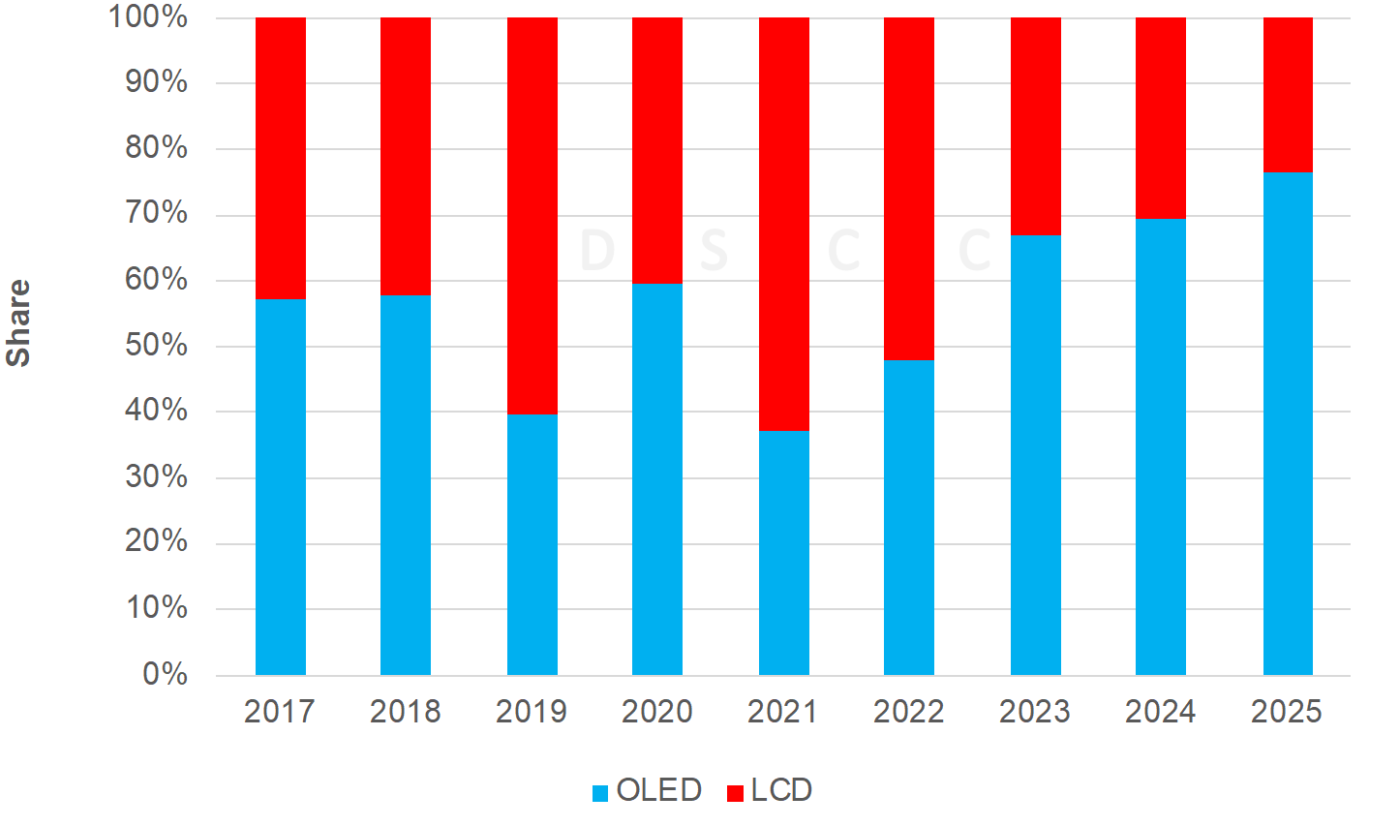

DSCC expects to see increased OLED spending in the IT space as OLED manufacturers target the enormous opportunity waiting for them in tablets, notebooks and monitors. In 2021, OLED penetration into the >650M unit IT display market is expected to be just 1.4%. DSCC expects to see fabs focused on the IT markets accounting for 37% of 2022-2025 OLED equipment spending and 40% of 2023-2025 spending as another new G8.5 IT OLED line was added. Helped by spending in IT markets, 2024 is expected to be the largest year for OLED equipment spending since 2017. From 2020-2025, OLEDs are expected to account for 60% of LCD + OLED equipment spending with LCDs now expected to lead in both 2021 and 2022 on the recent surge in LCD pricing.

DSCC’s Display Equipment Spending Forecast by Application (Delivery Basis)

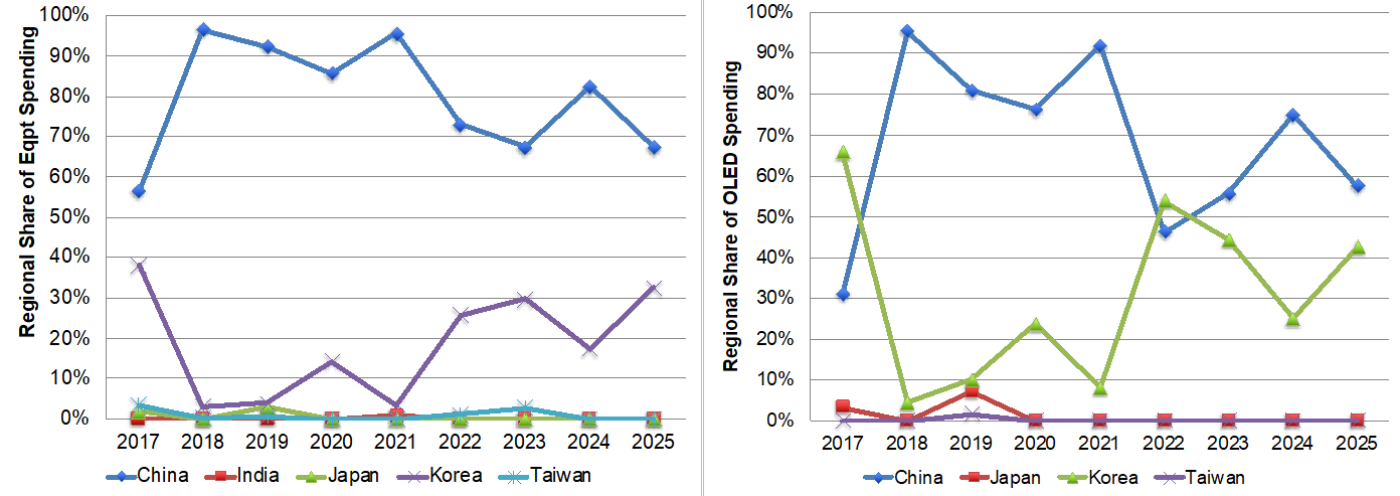

While mobile OLED spending has slowed in China due to lack of penetration, OLED spending in Korea and LCD spending in China continue to increase. DSCC has increased 2020-2025 OLED spending in Korea on IT markets by 19% vs. last quarter to over $10B on a recent G8.5 addition. Korea’s OLED spending is expected to grow by 637% in 2022 and another 50% in 2023 to $4.4B. In addition, LCD spending continues to increase, with DSCC raising its 2020-2025 LCD spending forecast for the fifth straight quarter on six new investments. DSCC is now showing $33B in LCD fab spending from 2020-2025, including new investments in Taiwan and India as well as China. China’s LCD spending was increased by another 1% to $31.9B.

DSCC’s Display Equipment Spending Forecast by Region and OLED Spending by Region (Delivery Basis)

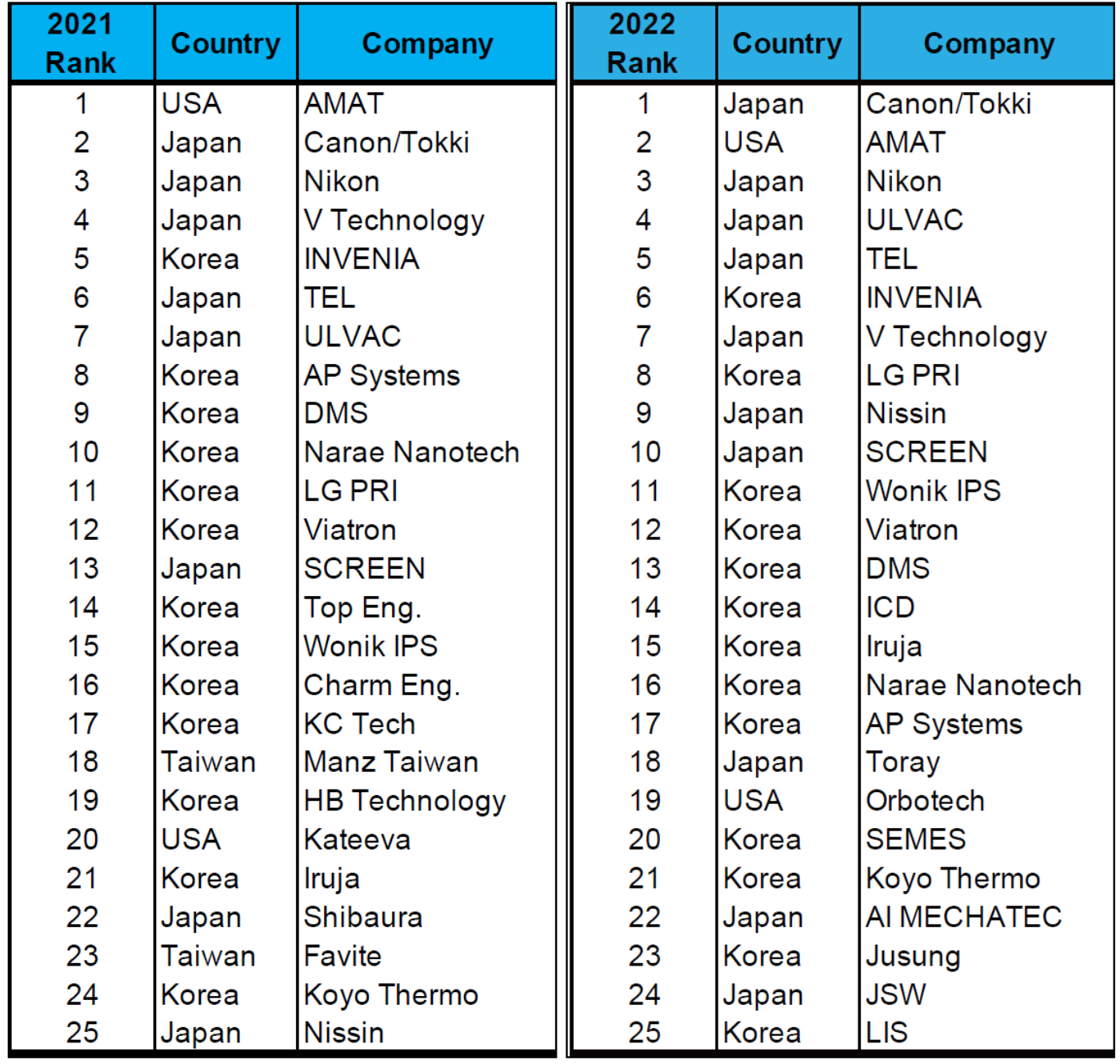

The Q4’21 issue of DSCC’s Quarterly Display Capex and Equipment Market Share Report also reveals the latest look at 2021 revenues by equipment supplier and the first snapshot of 2022 rankings. Applied Materials is expected to be the #1 display equipment supplier in 2021 on both a move-in and install basis due to its dominant position in CVD and TFE and share gains in array test and sputtering. It is expected to be followed on a move-in basis by Canon/Tokki, Nikon, V Technology, INVENIA, TEL, ULVAC, AP Systems, DMS and Narae Nanotech. DSCC provides market share for over 60 different segments on a unit and revenue basis, which can also be segmented by frontplane technology, backplane technology, substrate size, region, application and more. Despite the market falling by 16% in 2021, there are a few suppliers seeing impressive growth on a delivery basis including:

- V Technology up 59% on significant CF exposure share gains.

- INVENIA up 86% on significant dry etch share gains.

- ULVAC up 5% on sputtering share gains.

- LG PRI up 56% on organic TFE and lamination share gains.

- Viatron up over 700% on furnace/PI curing share gains.

- Top Eng. up over 100% on significant scriber share gains.

Of the top 25 suppliers, there are expected to be:

- 13 from Korea;

- 8 from Japan;

- 2 from the USA;

- 2 from Taiwan.

In 2022, the top 10 are expected to be Canon/Tokki, AMAT, Nikon, ULVAC, TEL, INVENIA, V Technology, LG PRI, Nissin and SCREEN. Companies gaining share in the top 10 include:

- Nikon on more design wins.

- ULVAC on share gains in CVD, sputtering and FMM VTE.

- TEL on dry etch share gains.

- LG PRI on wins across 8 different types of tools with share gains in 6 of them.

- Nissin on wins at new mobile OLED fabs, new LTPS LCD fabs and in LTPO conversions where additional implant steps are being used.

By country, the top 25 are expected to be segmented as follows:

- 13 from Korea;

- 10 from Japan;

- 2 from the USA.

2021-2022 Top 25 Display Equipment Suppliers on a Delivery Basis

The latest report also features a detailed look at the latest manufacturing trends covering:

- Touch on TFE

- LTPO

- Color on Encapsulation

- IGZO Advances, Scaling to G8.5 and Oxide OLED Cost Advantages

- Tandem Structures

- Under Panel Cameras and IR Sensors

- Auxiliary Electrodes for Reducing OLED IR Drop/Power Consumption

- WOLED, QD-OLED and IJP RGB OLED Manufacturing

For more information on DSCC’s Quarterly Display Capex and Equipment Market Share Report, please contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Display Capex and Equipment Market Share Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。