国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 09/27/2021

DSCC Releases Its Future of OLED Manufacturing Report, Reveals How OLED Technology, Manufacturing, Performance and Products Are Likely to Evolve

Ross Young, Founder and CEOAustin, TX USA -

DSCC has released its 338-page report on The Future of OLED Manufacturing (一部実データ付きサンプルをお送りします), which is really a look at how all aspects of OLEDs are likely to evolve with special attention paid to how OLED manufacturers are likely to address the IT display opportunity including the scale up of G6 FMM VTE-based RGB OLEDs to G8.5 and the migration from LTPS/LTPO to IGZO. This breakthrough report is divided into five sections:

- Commercial/Industrial History of OLEDs

- Historical and Current Technical Challenges

- Mobile OLED Manufacturing/Roadmap

- IT OLED Manufacturing/Roadmap

- OLED TV Manufacturing/Roadmap

The history chapter goes back to the beginning of OLEDs covering:

- The first paper from Tang and Van Slyke in 1987;

- Samsung SDI’s entry and early struggles;

- Samsung’s OLED TV attempt and LGD’s OLED TV success;

- Samsung’s success in mobile OLEDs;

- Apple-SDC tie up, Chinese follow;

- Apple’s all OLED line-up, etc.

The next chapter on historical and current challenges covers:

- What are the typical yields by region and technology;

- What are the biggest sources of yield loss;

- What is the capacity outlook by technology and manufacturer;

- Impact of China;

- Threats from other technologies including miniLEDs, microLEDs, QNED, etc.;

- How the capital intensity in OLED manufacturing has risen.

The smartphone chapter covers a long list of innovations that have recently appeared or are likely to appear in the near future which include:

- Integrating the touch sensor;

- Offering variable refresh down to 10Hz;

- Replacing the polarizer with a color filter;

- Micro lens patterning;

- Hiding selfie cameras and IR sensors under the display;

- High resolution lithography;

- High efficiency blue OLED emitters;

- IGZO backplanes;

- Optimizing the display to enable new form factors such as foldable and rollable.

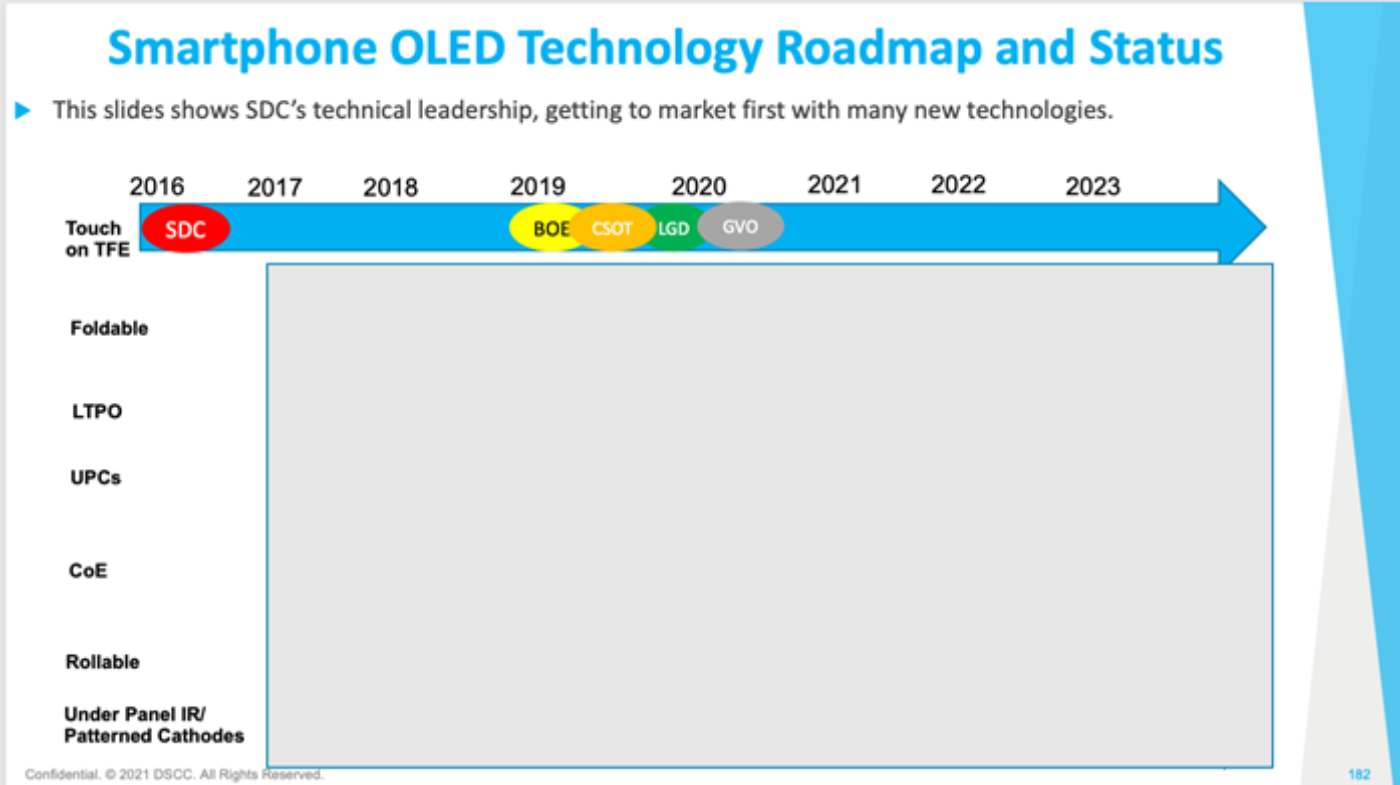

We share our view on the smartphone display technology roadmap and each panel suppliers’ status in technology commercialization as shown in the redacted slide below. This slide is very useful in pointing out SDC’s leadership and how it has used its advances in OLED manufacturing and device technology to stay ahead of its competitors and maintain its high market share.

The IT market (notebooks, tablets and monitors) is a key market for OLEDs as they look to overtake LCDs. This chapter covers:

- What is the IT display opportunity, what products exist and what products are coming? What is the technology roadmap?

- How OLED manufacturers plan to scale their RGB OLED technology from G6 to G8.5 to become more cost competitive with LCDs and overtake LCDs.

- What kind of cost savings can be realized at G8.5 IGZO FMM VTE fabs vs. G6 LTPS fabs?

- What are the technical challenges in scaling OLED frontplanes based on FMM VTE to G8.5?

- Will G8.5 FMM VTE RGB OLED fabs be rigid or flexible?

- Are there FMM solutions for vertical full G8.5 masks?

- Which companies are best positioned for the IT market?

- How will OLEDs meet new requirements for IT applications in regard to burn-in, lifetime, brightness, etc.

- Quantifying the advantages of tandem structures.

- Burn-in compensation schemes.

- Apple and Samsung’s roadmaps for tablets and notebooks.

- OLED vs. miniLED vs. a-Si cost forecasts.

- What is the OLED vs. miniLED forecast in each IT market including the emergence of mirror displays.

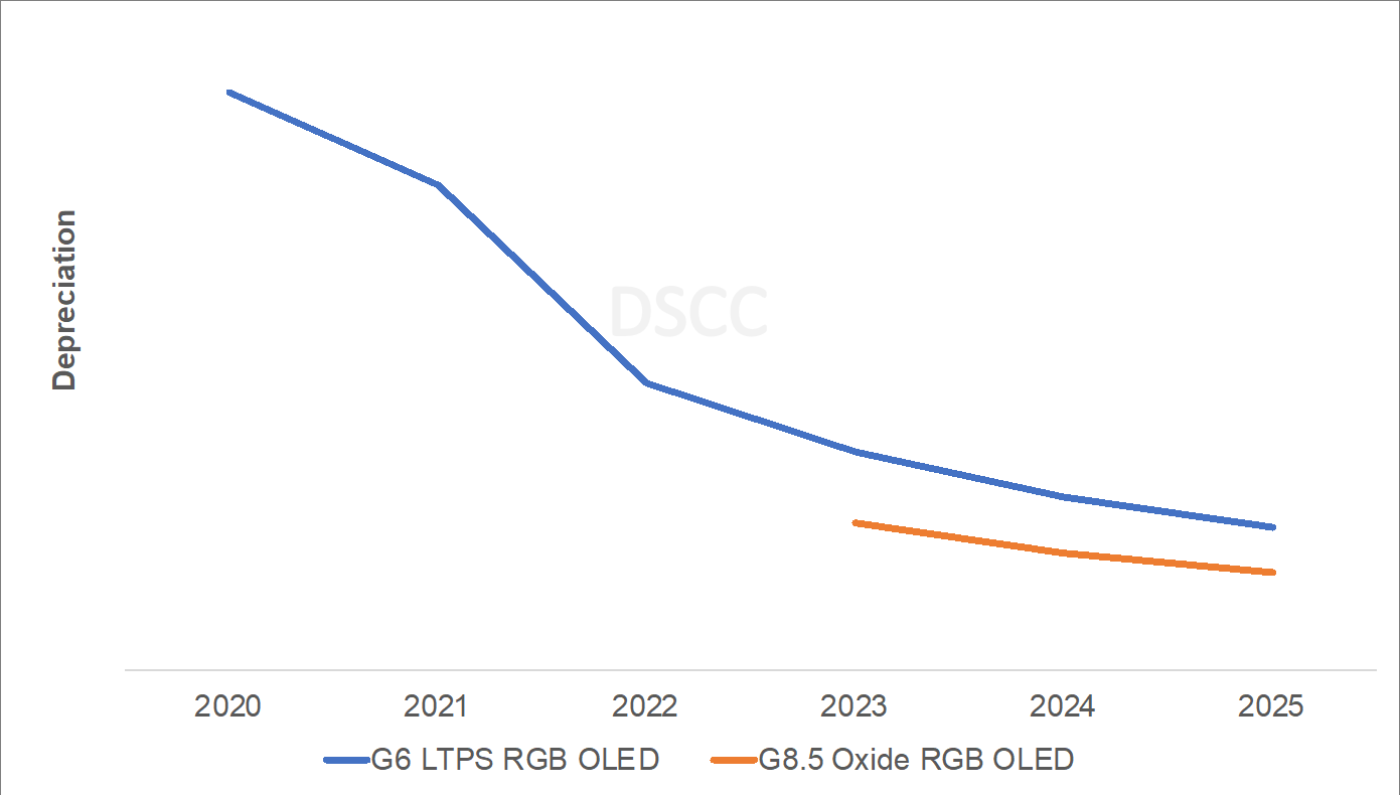

You can see the relative cost savings OLED manufacturers are likely to experience by migrating to IGZO on G8.5 substrates with FMM VTE equipment vs. LTPS at G6. This chart shows the difference in depreciation per panel resulting in large savings and a cost advantage vs. G6 LTPS OLED with even bigger savings vs. flexible OLED.

G6 LTPS RGB OLED vs. G8.5 IGZO RGB OLED

While OLEDs don’t face competition at the high-end of the smartphone market, they will face competition in the high end of the IT market for many years through LCDs with miniLED backlights. OLED suppliers will need to innovate to minimize their disadvantages vs. miniLEDs and maintain their advantages. Examples include:

- Oxide and LTPO backplanes for variable refresh.

- Tandem structures to increase brightness, increase efficiency and reduce the likelihood of burn-in.

- Auxiliary electrodes to reduce IR drop, reduce power and improve efficiency through cathode patterning;

- Under panel cameras and IR sensors to maximize screen to body ratios/minimize bezel widths and offer multi-factor authentication;

- High efficiency blue OLED emitter to help extend lifetime and minimize burn-in.

The TV chapter examines:

- OLED TV fab schedules

- Pros and cons of each OLED TV technology

- Outlook for OVJP and QNED.

- How auxiliary electrodes are likely to be implemented?

- Role of high efficiency blue OLED emitters in TVs.

- OLED TV product roadmaps

- OLED TV vs miniLED vs. a-Si LCD cost forecasts

- OLED TV vs. miniLED shipment forecasts

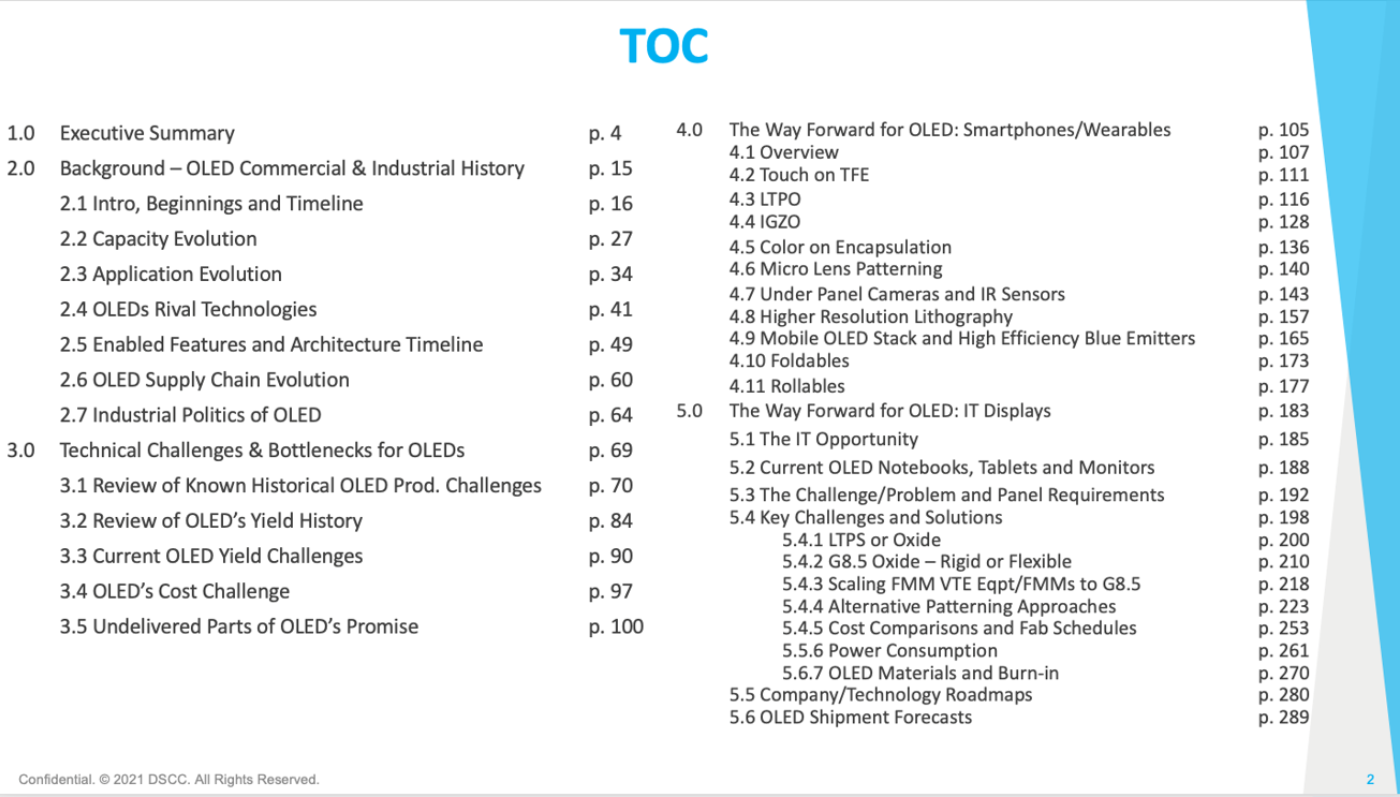

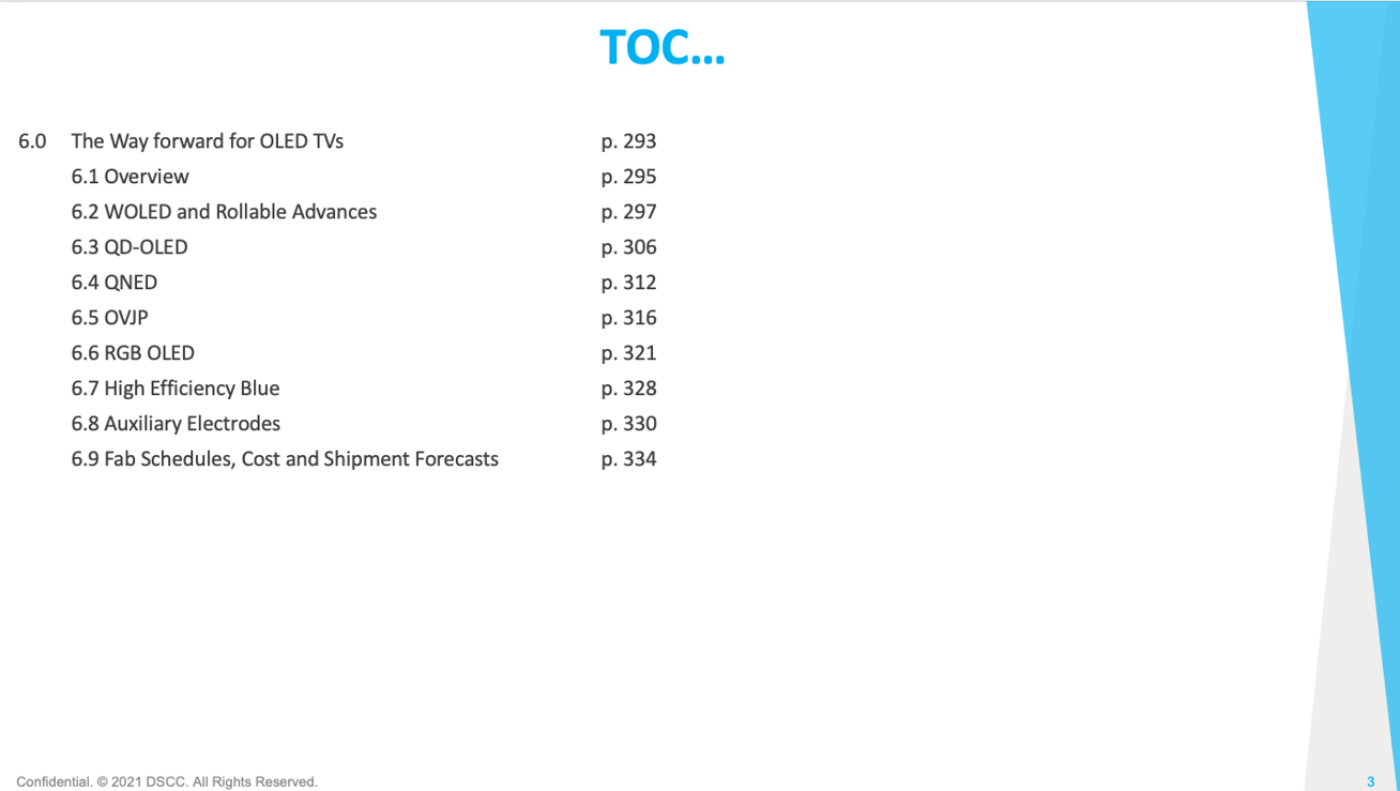

The table of contents for this highly informative report is below. For more information, please contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

The Future of OLED Manufacturing Report 2021

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。