国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 06/01/2021

LCD Capacity Upgraded on Numerous Expansions

Ross Young, Founder and CEOAustin, TX USA -

DSCC upgraded its LCD capacity forecast in the latest issue of its Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) while reducing its OLED capacity forecast.

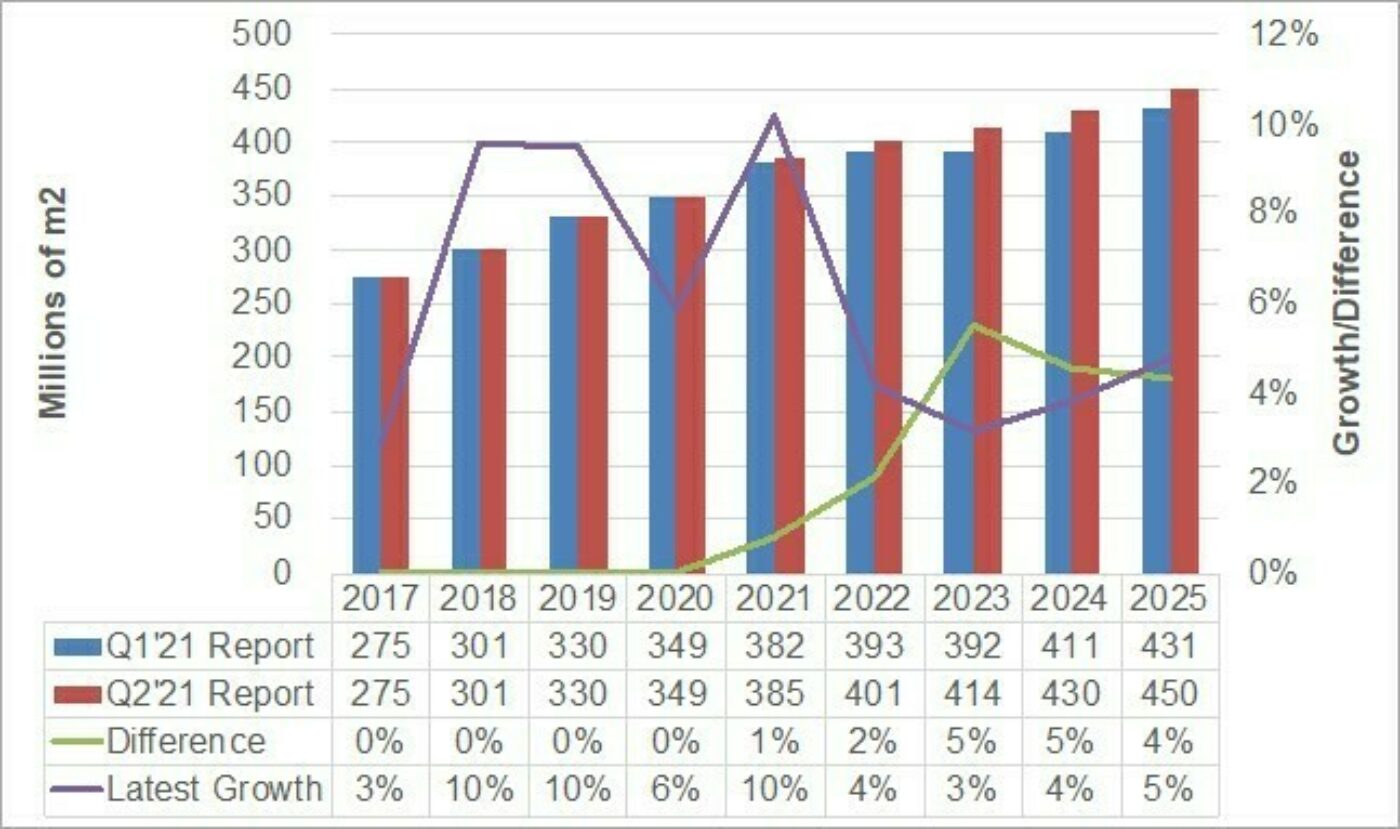

As indicated in the figure, DSCC upgraded its 2025 display capacity forecast by 4.4% versus the prior issue due to 14 new LCD investments as manufacturers respond to tight supply and higher prices. Manufacturers are also looking to stretch capacity through process simplification and de-bottlenecking to meet demand and take advantage of the higher prices. We now see 10% growth in LCD + OLED capacity in 2021, with 3%-5% growth from 2022-2025. Relative to last quarter, capacity growth is 1% - 5% higher per year from 2021-2025. Display capacity is now growing at a 5.2% CAGR versus 4.3% last quarter. LCD capacity was upgraded by 5.3% versus the previous issue and now grows at a 3.9% CAGR versus 2.8% last quarter.

OLED capacity was downgraded by 2% versus our previous forecast due to several delays and one cancellation. OLED capacity is now expected to grow at an 18.6% CAGR versus 19% last quarter. Key variables to the LCD growth include if and when LGD will shut down its LCD TV panel fabs in Korea and how much used capacity EFonLong/Taijia will be able to successfully ramp in China after acquiring 120K G8.5 substrates per month capacity from SDC.

2017 - 2025 Display Capacity Forecast, Growth and Change vs. Last Quarter

This report examines capacity by:

- Quarter/Year;

- Frontplane;

- Backplane;

- Application;

- Region;

- Substrate Size;

- Manufacturer;

- Form Factor (Flexible vs. Rigid).

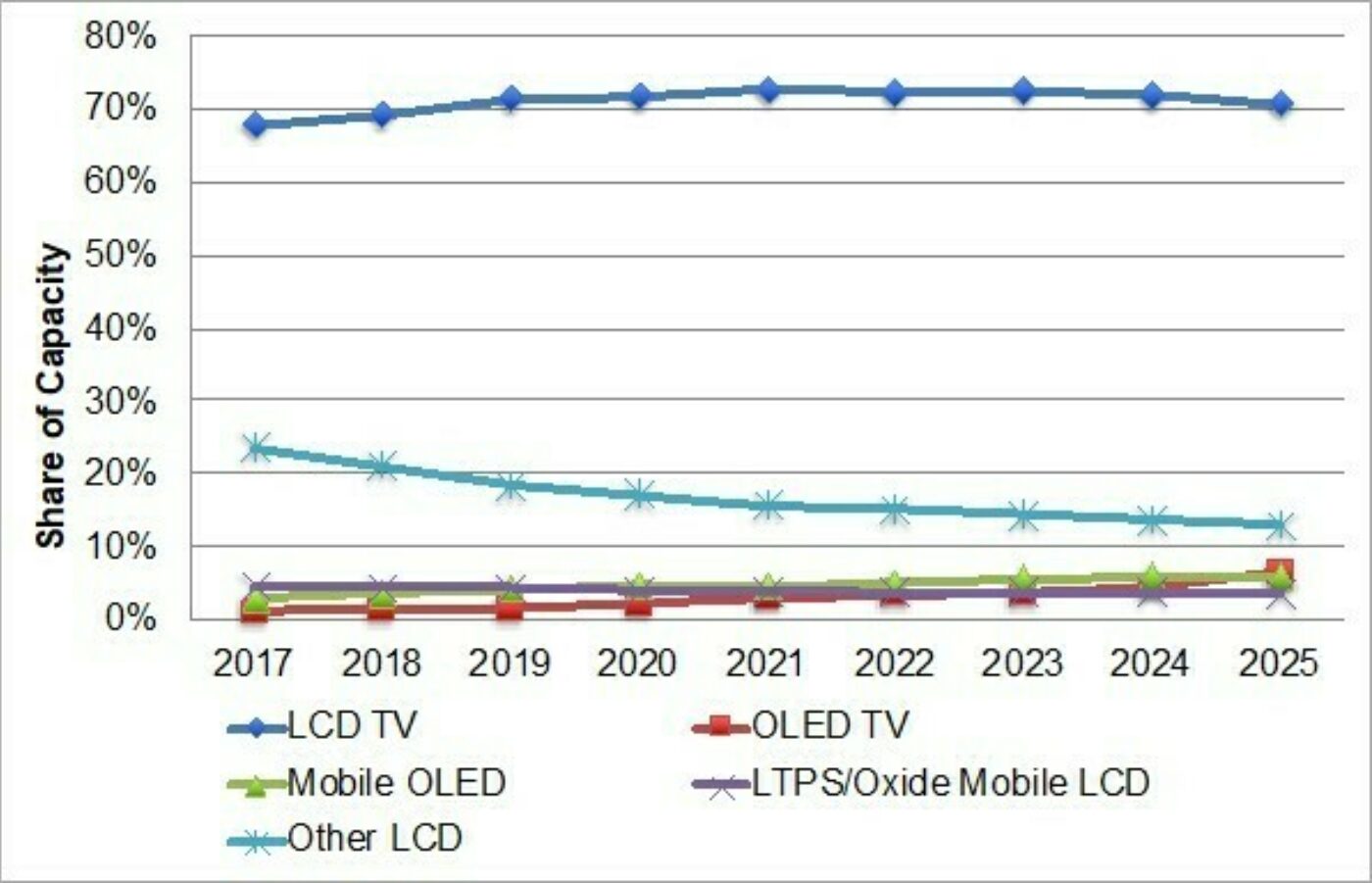

LCD TVs will continue to dominate capacity, and we now show them growing at a 4.9% 2020-2205 CAGR, up from 3.6% last quarter, encouraged by improved market conditions and the strong outlook for miniLED LCD TVs. OLED TVs are expected to enjoy the fastest growth, rising at a 31% CAGR, down from 32% last quarter on some delays, with its share rising from 2% in 2020 to 7% in 2025.

Mobile OLEDs are expected to grow at an 11% CAGR and reach a 6% share in 2025, down from 7%. Mobile LCDs are rising at a 3% CAGR and maintain a 4% share. Other LCDs are expected to fall at a 0.5% CAGR, with its share falling from 17% to 13%.

2017 - 2025 Display Capacity Forecast

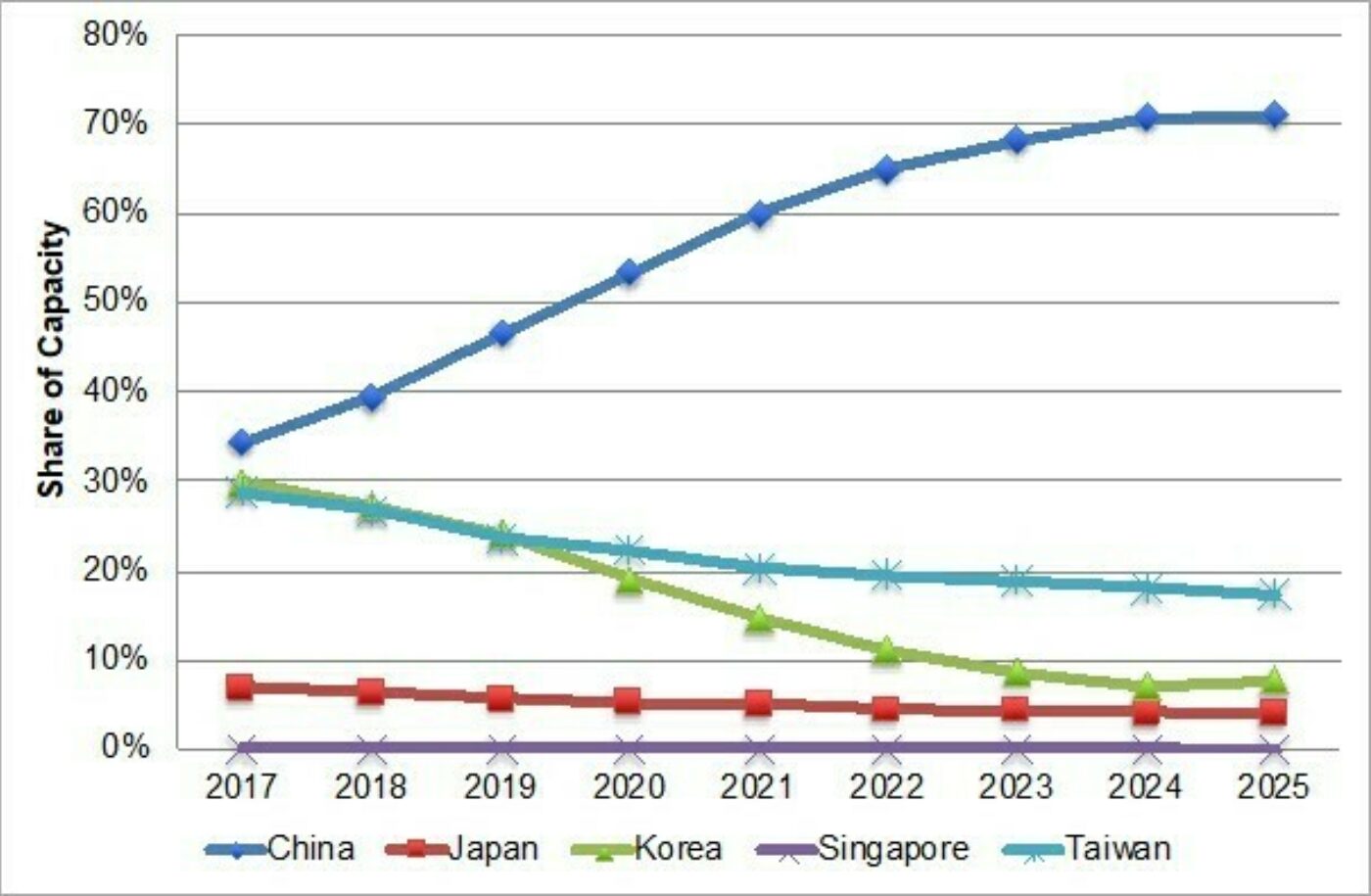

Regionally, China’s share is expected to rise from 53% in 2020 to 71% in 2025, and is the only region expected to experience capacity growth over the forecast. China’s display capacity is now expected to rise at an 11.4% CAGR, up from 10.1% last quarter, with Korea down at a 12.2% CAGR and Japan, Singapore and Taiwan flat.

Regional Share of Display Capacity

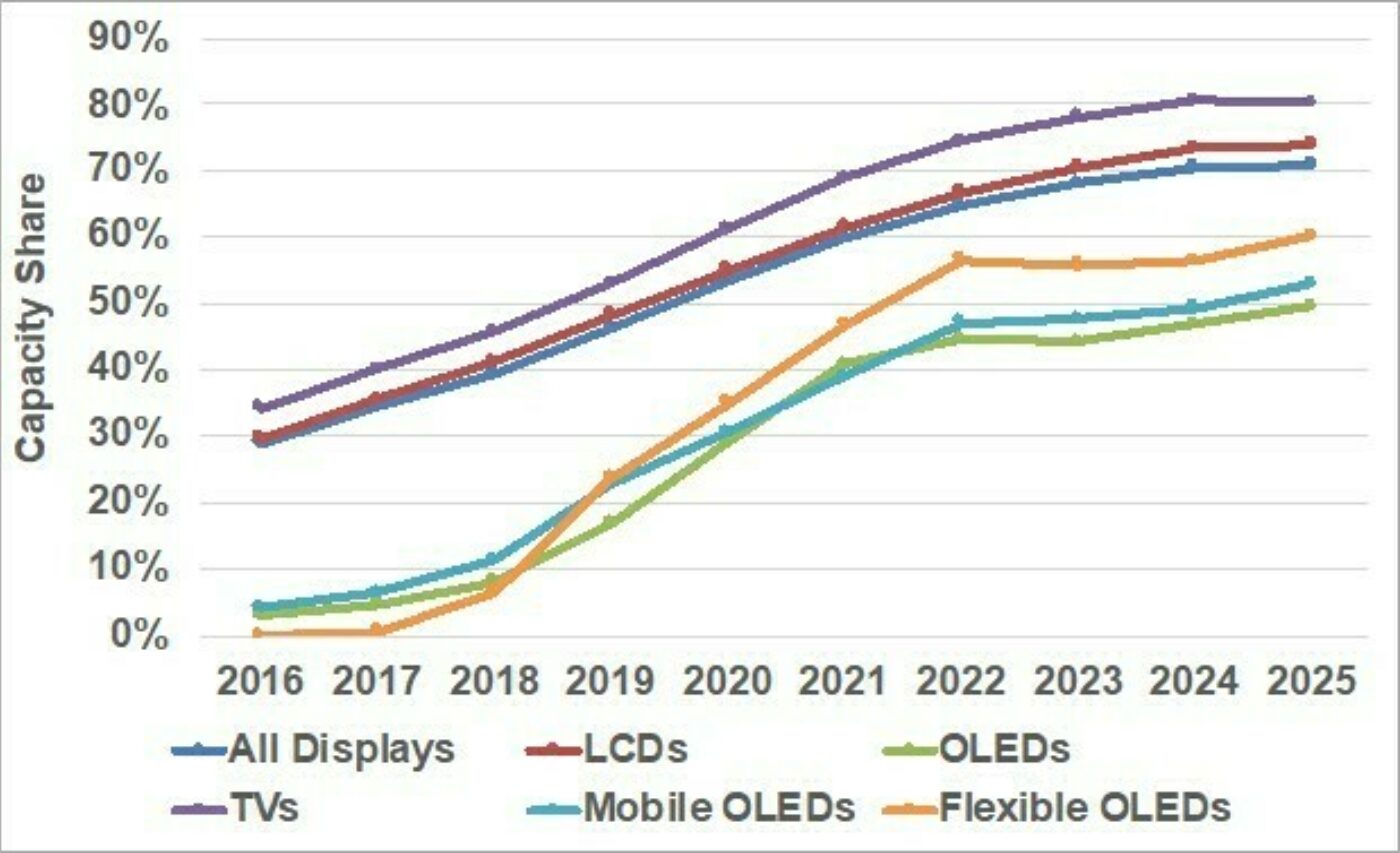

China’s capacity share in all major applications/technologies is shown in the figure below. As indicated:

- Its LCD share is expected to rise from 55% in 2020 to 74% in 2025;

- Its OLED share is expected to rise from 29% in 2020 to 49% in 2025;

- Its TV share is expected to rise from 53% in 2020 to 80% in 2025;

- Its mobile OLED share should reach 53% in 2025, with its flexible OLED share reaching 60%.

China’s Capacity Share by Application/Technology

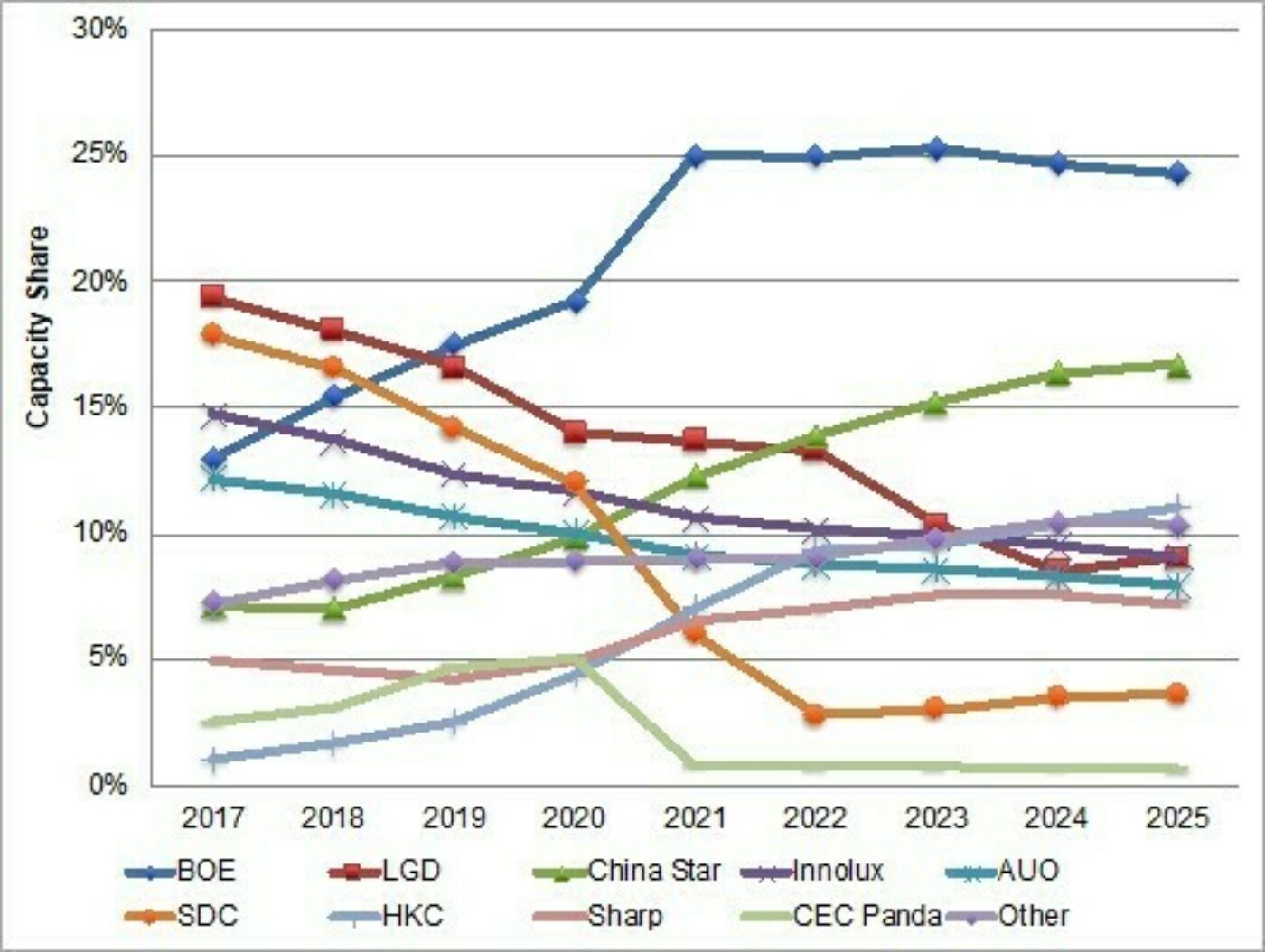

By manufacturer, BOE became the #1 display supplier on a capacity basis in 2019 with a 17.5% to 16.6% advantage over LGD. We expect BOE to widen its advantage on an 11% CAGR, up from 9%, from 2020 to 2025 due to its acquisition of most of CEC Panda and its G10.5 LCD and G6 and G8.5 OLED investments. China Star is expected to become #2 in 2022 on its acquisition of SDC Suzhou and its new LCD and OLED fabs growing at an 18% CAGR. LGD is now expected to fall more slowly as it keeps its LCD fabs operating in Korea for longer. It will still fall from #1 in 2018 to #2 in 2019, #3 in 2022, #5 in 2024 and 2025.

Display Capacity by Manufacturer

In the case of LCDs, BOE, China Star and HKC are even more dominant and are the top three suppliers. In OLEDs, LGD is expected to lead from 2021-2025. In mobile OLEDs, rigid OLEDs and flexible OLEDs, SDC is expected to lead. For more information on display capacity, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。