国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 02/15/2021

[Blog] LCD Shortages Leads to Surge in LCD Capex

Ross Young, Founder and CEOAustin, TX USA -

With LCD prices surging, many customers on allocation due to tight panel supply and component shortages and LCD manufacturers enjoying strong financial performance and stock price appreciation, LCD manufacturers are now projected to embark on a new wave of capacity growth.

DSCC has raised its 2020-2024 LCD equipment spending forecast by 55% to $20.7B in its latest Quarterly Display Capex and Equipment Market Share Report versus its prior issue. The surge in LCD spending has boosted total display capex by 10% to $64B over the same period.

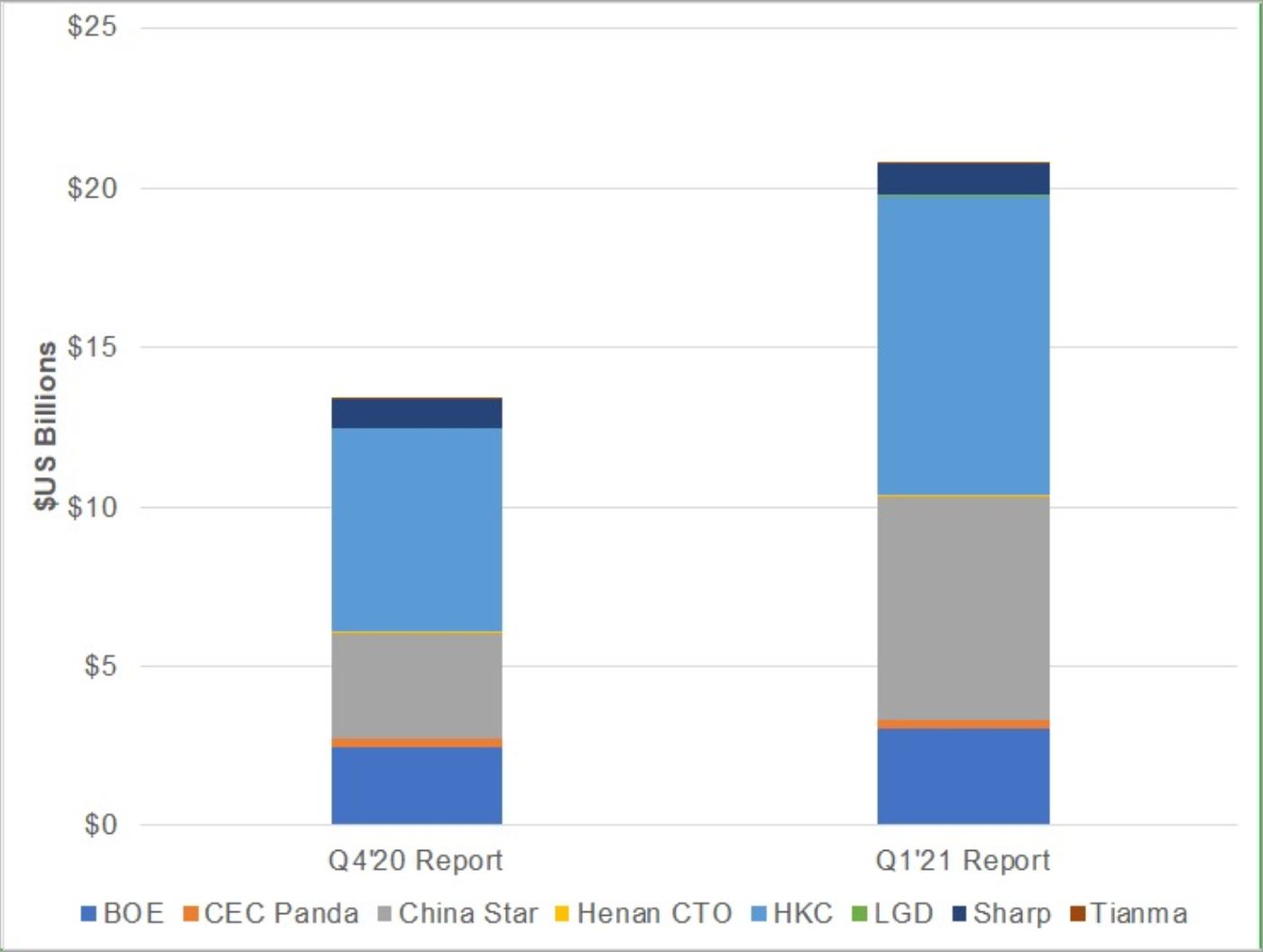

2020-2024 LCD Equipment Spending

While LCD revenues grew just 1% in 2020 as prices fell to new lows in the first half of the year, DSCC predicts 25% growth in 2021 to $106B on higher prices and continued large-area (10”+) unit growth. Total display revenues with OLEDs included are now expected to grow 22% in 2021 to $144B, a record high for the display industry.

LCD manufacturers are not only benefitting from strong demand from the COVID-19 inspired work from home (WFH), learn from home (LFH) and entertain from home (EFH) wave which has boosted both IT and TV markets, but also from the arrival of miniLED backlights which narrow the performance gap with OLEDs at the high-end of these markets and also raise LCD prices. Due to rising prices and increased confidence in continued growth, LCD manufacturers are now looking to add capacity where they can through both small expansions where space exists as well as in new fabs.

DSCC’s Q4’20 and Q1’21 2020-2024 LCD equipment spending forecasts are compared in the first figure on a move-in basis. As indicated, LCD equipment spending will be dominated by three companies, BOE, China Star and HKC. All three of them have increased their LCD spending plans by at least 25% from our Q4’20 to our Q1’21 issue.

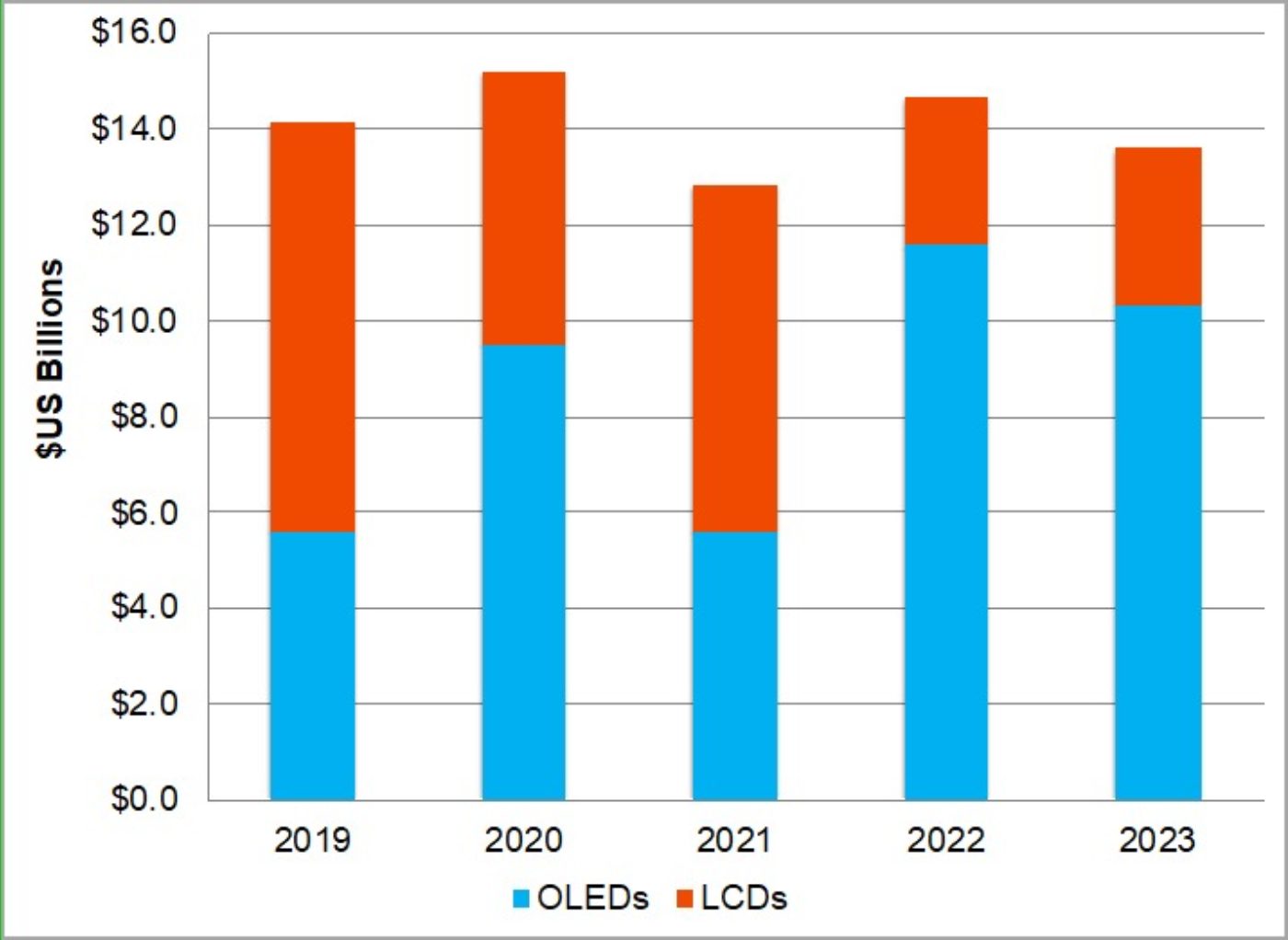

As a result of the recent surge in LCD equipment spending, total display equipment spending on a move-in basis from 2019-2023 now looks quite consistent ranging between $13B and $15B per year. OLEDs are expected to lead with a 60% share with LCDs at 40%.

2019-2023 Display Equipment Spending (Move-In Basis)

The sudden surge in LCD spending is welcomed by a number of equipment suppliers overly reliant on LCD fabs who have begun to diversify into OLEDs and semiconductors. This gives them more time to succeed in their diversification efforts and may result in outperformance as LCD spending now looks to go on well beyond previous expectations. It is also a welcome relief to buyers of LCD panels who can’t get enough supply. DSCC will upgrade its LCD capacity forecast as a result of these developments very soon.

For more information on DSCC’s Quarterly Display Capex and Equipment Market Share Report, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。