国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 09/15/2020

Latest Large-Area Display Capacity Outlook Shows 1% Decline in 2021

Ross Young, Founder and CEOAustin, TX USA -

Last week DSCC released the capacity section of its Quarterly Display Capex and Equipment Market Share Report which looks into industry capacity by application, frontplane, backplane, country, supplier, substrate, etc.

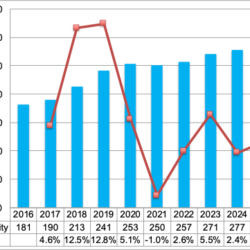

One of the interesting takeaways was the outlook for G7+ capacity for LCDs and OLEDs. As indicated below, G7+ capacity is expected to fall 1% in 2021 after rising by over 12% in 2019 and 2019 and 5% in 2020. This is a result of LCD fab shutdowns in Korea and delays in new fab ramps due to COVID-19. With LCD TV panel demand expected to rebound in 2021, it should keep supply tight, prices should continue to rise, and margins and stock prices should improve for panel suppliers. Will it lead to new spending in LCDs? We aren’t hearing about that at the moment. Looking beyond 2021, we are optimistically seeing 2% - 6% growth which includes some low probability investments. From 2020-2025 we only see LCD+OLED capacity rising at a 2.5% CAGR which I believe is a historically low figure which could lead to elevated margins for display suppliers for years.

⇒ 続き (図表入り全文) はこちらから

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。