国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 11/22/2021

OLED Share Continued to Increase in Advanced TV Market in Q3’21 and Samsung's Share Continued to Slip

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

The combination of relatively stable OLED TV prices competing against rising LCD TV prices led to another quarter of gains for OLED TV sales, according to the latest update of the DSCC Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします), now available to subscribers. As OLED has gained share, Samsung has lost share in the Advanced TV market, and while Samsung maintained the #1 position in both units and revenues in Q3’21, its share has eroded especially in Western Europe.

This report covers the worldwide premium TV market, including the most advanced TV technologies: WOLED, QD Display, QDEF, Dual Cell LCD and MiniLED with 4K and 8K resolution. The report looks at current and future TV shipments and revenues by technology, region, brand, resolution and size, and forecasts the growth of all of these technologies. This update includes the shipment results for Q3’21 and a forecast for Q4’21; an updated forecast out to 2026 will be published later in the quarter.

We define an “Advanced TV” (capitalized) as any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology. The historical data in the report allows analysis by feature for Advanced LCD TVs, including:

- QDEF TV: TV using a Quantum Dot Enhancement Film; these TVs are sold as “QLED” by Samsung, TCL and others;

- MiniLED: LCD TVs with a MiniLED backlight, as sold by TCL starting in 2019 and introduced by Samsung, LG, Hisense and others in 2021;

- Dual Cell: LCD TVs employing dual-cell technology, as introduced by Hisense in 2019;

- LCD Others: this category includes LCD TVs with 8K resolution, which do not fall in any other category.

The historical data for OLED TV includes only one product configuration, LGD’s White-OLED (WOLED) technology, but the forecast in the report includes QD Display, which designates QD OLED and successor technologies such as QNED and EL-QLED, as well as Rollable OLED and MicroLED. Our forecast for MicroLED TV is based on product sizes up to 110”, as products in larger sizes such as Samsung’s 146” The Wall, belong in a different category than “TV”.

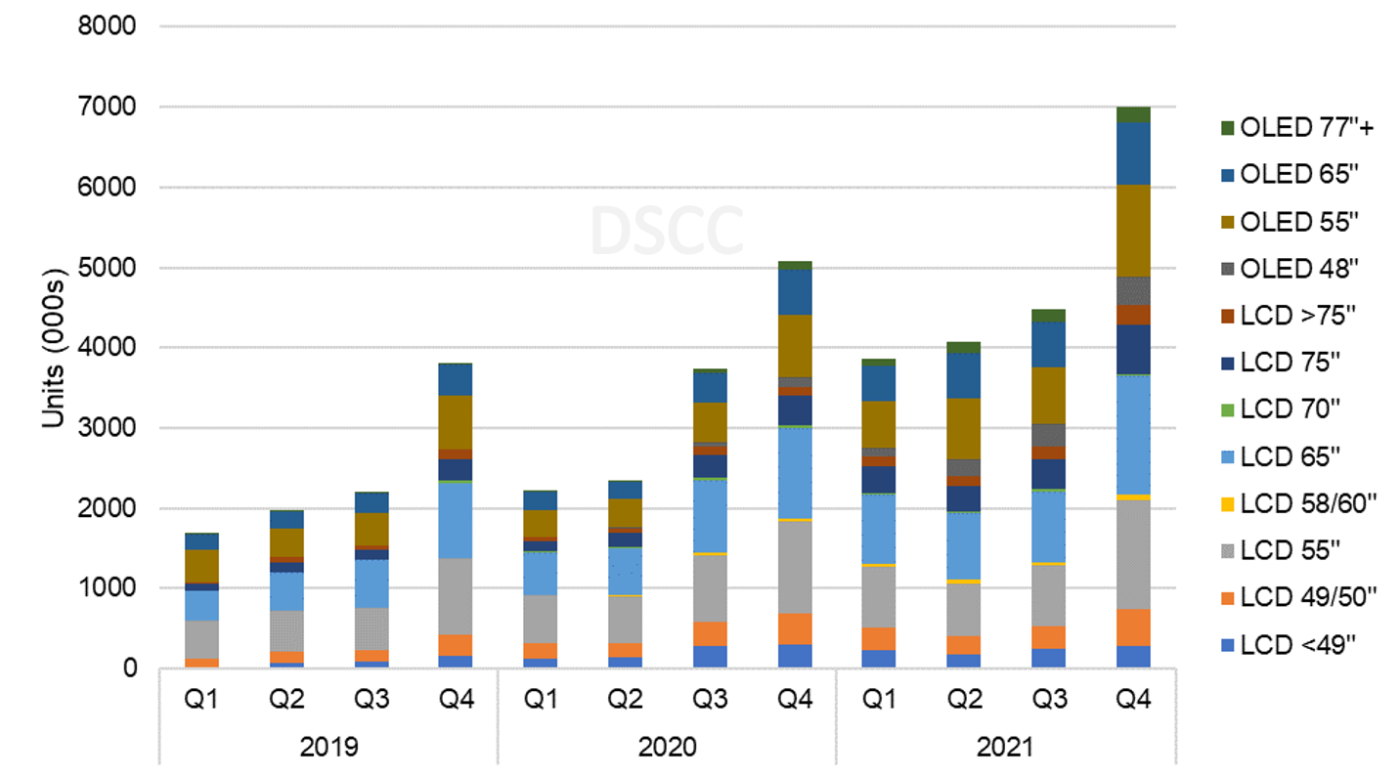

Advanced TV shipments in Q3’21 increased by 20% Y/Y to 4.5M units, as shown in the first chart here. In volume terms, the entire Y/Y increase was provided by OLED TV, as Advanced LCD TV shipments were flat Y/Y. Within the LCD category, shipments for 65” and smaller sizes declined Y/Y while Advanced LCD TVs of 75” increased 32% Y/Y and Advanced LCD TVs larger than 75” increased 58%. All screen size groups for OLED TVs increased Y/Y, with the biggest gains in 48”, up 399% Y/Y and 77” and larger, up by 194%. The 48” OLED TV models were introduced only in Q2’20 but already represented 15% of OLED TV volume in Q3.

While OLED TV share of all Advanced TV had declined during 2018-2020, the additional capacity from LG Display’s Guangzhou fab combined with the steep increases in LCD TV panel prices up through Q2’21, has helped OLED TV regain share in the premium category. OLED TV shipments increased by 77% Y/Y in Q2’21 and OLED TV share increased from 26% in Q3’20 to 38% in Q3’21.

Advanced TV Shipments by Size and Display Technology, 2018 to 2021

Advanced TV revenue growth in Q3 was substantially higher than unit growth at 50% Y/Y. Revenues for Advanced LCD TVs grew 27% Y/Y despite flat unit shipments as the screen size mix got bigger and TV prices increased. OLED TV revenues increased 88% Y/Y and OLED revenue share increased from 37% in Q3’20 to 46% in Q3’21. Revenues for 77”+ OLED grew 146% Y/Y as the new 83” models sold well, adding to strong growth in 77”.

We expect continued growth in Advanced TV shipments in Q4; we forecast an increase of 38% Y/Y to nearly 7M TV sets. We expect Advanced LCD TV shipments to increase 29% Y/Y while OLED TV shipments increase 58% Y/Y. With LCD TV panel prices declining sharply in Q3’21, we expect LCD to regain some share in Q4, with OLED TV capturing 35% of the Advanced TV category in Q4’21, up from 31% in Q4’20.

One minor note on the TV technology front for our Q4 forecast – we expect the first sales of Samsung MicroLED TVs in Q4 in the 110” size. We forecast sales of 30 units of MicroLED, which represents 0.0004% unit share of the Advanced TV market. You’ve got to start somewhere.

The report’s pivot tables allow an analysis of brand share by screen size, region, technology, resolution and other variables. In Q3’21, among all Advanced TV products, Samsung maintained its leading position but lost some share with unit shipments down 7% Y/Y compared to the company’s outstanding Q3’20. LG Electronics increased shipments by 123% with big increases in OLED and some sales of Advanced LCD TVs and LG’s share increased from 14% in Q3’20 to 25% in Q3’21. TCL Advanced LCD TV shipments increased by 44% Y/Y but Sony did even better at 56% Y/Y to fend off its Chinese competitor and maintain the #3 position in Advanced TV units with an 8% share.

The report divides worldwide shipments into eight geographic regions. Western Europe and North America have continued to be the largest regions for Advanced TV. These two regions represented a combined 65% of Advanced TV units and 70% of revenue in Q3’21. Shipments to Western Europe increased 33% Y/Y in Q2’21 and revenues increased by 66% Y/Y. Shipments to North America increased 11% Y/Y and revenues increased 41% Y/Y as sales of big TVs surged. China, where OLED has struggled to gain share, appeared to be most affected by the LCD panel price increase and shipments there were flat Y/Y but revenues increased 29% as Advanced LCD TV prices increased and OLED gained some share.

In North America, Samsung enjoys a dominant position on the strength of its large-screen product portfolio but has seen its share erode as competitors in both Advanced LCD and OLED TV grow share. Samsung increased its share in North America shipments and held revenue share Q/Q but has lost share Y/Y in both measures. LG increased Advanced TV shipments to North America by 93% Y/Y to increase its unit share to 21%.

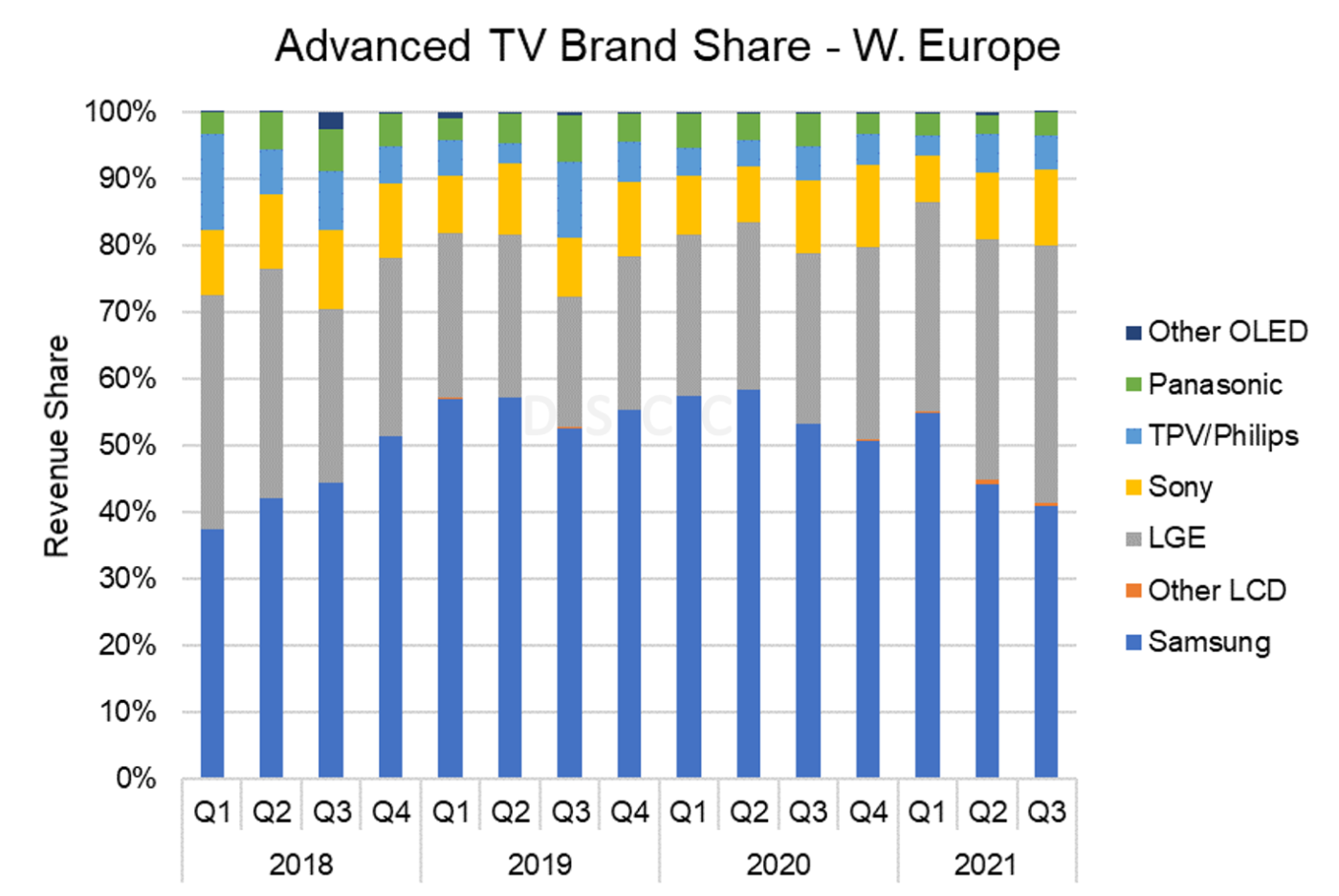

In Western Europe, Samsung continued to hold its position as the #1 brand but has seen its share erode with increasing competition. Samsung captured 53% share of Advanced TV units and 41% of revenues in Western Europe in Q2’21, but those figures were down 18% and 17%, respectively, compared to its share peak in Q2’20. Samsung remains ahead of its nearest competitor, but LG gained at Samsung’s expense with 31% share of units and 39% of revenue. Samsung’s product strategy emphasizing big sizes has not fared well in Europe where average screen sizes are smaller and the market for TVs larger than 65” is small compared to the US and China. LG’s introduction of the 48” OLED TV proved a key factor in the company’s share gain in Western Europe as nearly 50% of LG’s worldwide sales of 48” occurred in that region.

Another interesting cut of the brand data is the battle by screen size. In 55” worldwide unit shipments, Samsung continues to lead but that lead has narrowed, and LG has seized the #1 position in revenue share. Samsung’s unit share of 55” Advanced TV declined from 50% in Q2’20 to 42% in Q3’21, while LG’s share of 55” Advanced TV units increased Y/Y from 19% to 30%. Compared to a peak in Q1’20, Samsung lost 16 points of revenue share in Q3’21 with 32%, while during the same time frame LG increased its share by 12 points to 38%.

In the largest size category of 70”+ Samsung has seen its position erode from a near-monopoly in 2018 to 2019 to mere dominance in 2020-2021 as LG and Sony sales of 77” and 83” OLED and TCL sales of 75” and larger LCD have increased dramatically. In Q3’21, Samsung still captured 54% unit share of 70”+ Advanced TV shipments, but this figure was down from 79% in Q3’20. Meanwhile, LG, Sony and TCL gained share.

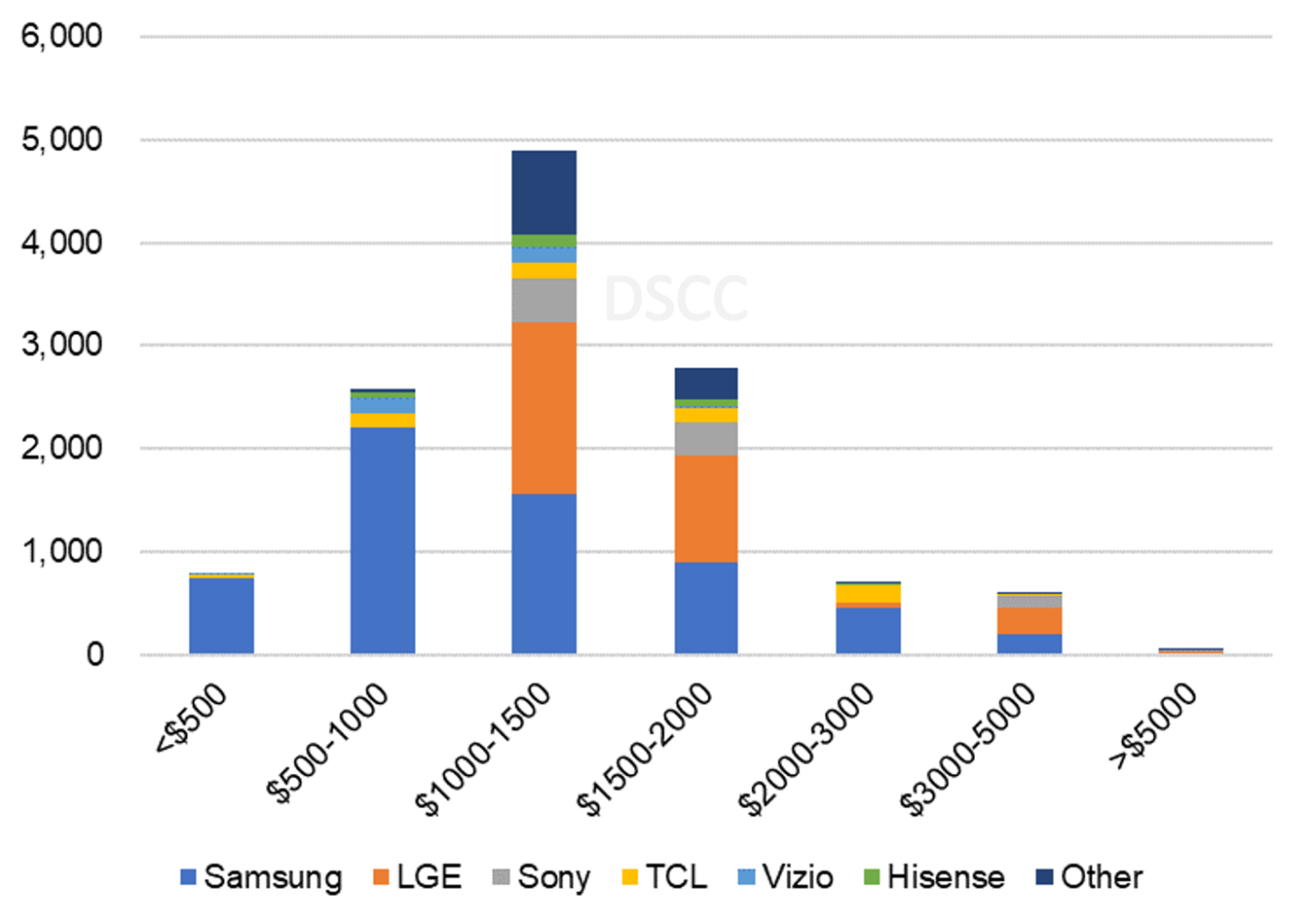

The last chart here shows one last valuable cut of the data, units by brand by price band. The pivot tables allow for this analysis by any time period, and the chart here shows the market by price band for the first three quarters of 2021. The chart shows that Samsung’s leading position in Advanced TV is mostly a function of its dominance in Advanced TVs under $1000. Samsung’s strategy of pushing its QLED product line toward mainstream price points has allowed it to thrive, but Vizio and TCL also appear as competitors at these lower prices. LG’s OLED TVs give it the leading position in the range of $1000-$2000 and above $3000, and Sony holds a solid #3 position in price points above $1000.

Worldwide Advanced TV Units by Price Band for Q1-Q3 2021

DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) includes technical descriptions of all major Advanced TV display technologies, plus quarterly shipment results from Q1’18 through Q3’21, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast for five years across technology, region, resolution and size. Readers interested in subscribing to the Quarterly Advanced TV Shipment and Forecast Report should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced TV Shipment and Forecast Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。