国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 11/08/2021

DSCC Report Compares and Forecasts OLED and MiniLED Panel Costs in Tablets, Notebooks and Monitors

Ross Young, Founder and CEOAustin, TX USA -

In DSCC’s newly released Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします), one of the many highlights is the cost comparisons between OLEDs and MiniLED panels in tablets, notebooks and monitors.

We took the MiniLED panel sizes that Apple has or will introduce at 12.9”, 16.2” and 27” and tried to compare them on an apples-to-apples basis with identically sized OLEDs. We actually looked at two different flavors of MiniLED backlight units (BLUs) as shown below. For tablets and notebooks, we looked at chip on board (COB) FPC and BT type PCB backplanes with 10,000 MiniLEDs and 2596 zones as well as a lower cost approach with 3000 MiniLEDs and 779 zones using package on Board MiniLEDs with FR4 PCB backplanes. For monitors, we used an 1152 zone configuration with 5000 MiniLEDs and a BT-type PCB backplane. The report laid out the type of fab utilization and yields which assumed G8.5 oxide backplanes were used with variable refresh rates up to 120Hz.

We also included assumptions for cost reductions associated with:

- Reductions in MiniLED costs due to higher yields and higher volumes;

- Reductions in # of MiniLEDs per panel due to efficacy improvements and optical enhancements;

- Reductions in transfer costs helped by faster transfer equipment at higher yields as well as fewer MiniLEDs per device;

- Lower backplane costs due to fewer MiniLEDs per device, the use of discrete driver ICs which should result in simpler backplane layouts with fewer layers;

- Optical films – today phosphor films are used and we expect new multi-function films to optimize the BLU film stack;

- LED driver ICs – we expect discrete bare ICs to be bonded together with LED dies in the future. Alternatively, some companies are working on integrating more and more dimming zones per IC resulting in fewer chips and packages, but higher power/cost ICs. The centralized approach may result in more than 256 zones per driver compared to <4 zones in the discrete approach, but it suffers from hot spots, more complicated PCB layouts and reliability issues if one driver IC fails.

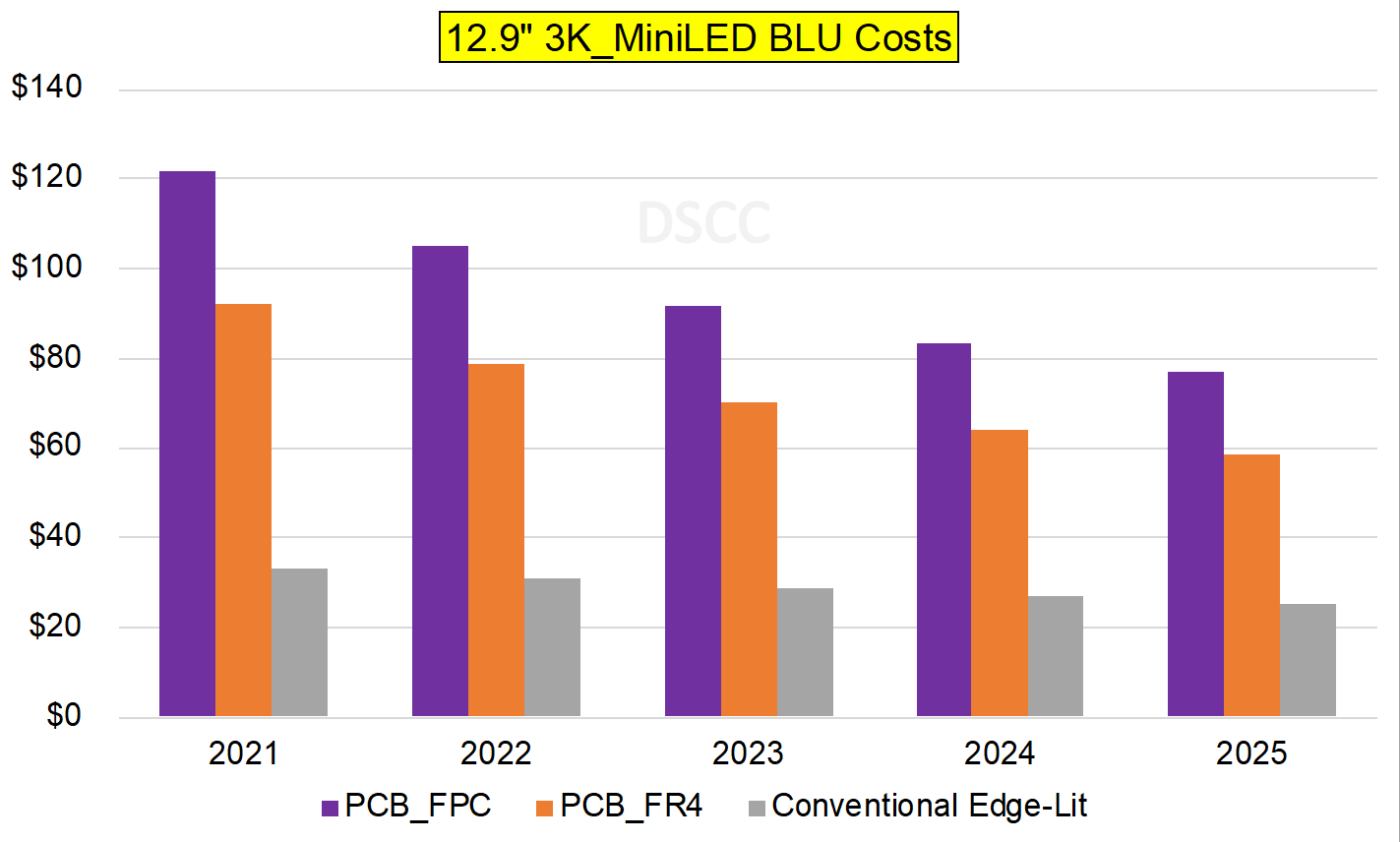

The approach Apple took costs around 3.7x more than conventional edge-lit backlights at 12.9”, but its costs are expected to fall at ~11% CAGR from 2021 to 2025 with the premium falling to 3.1x in 2025 or $52. However, lower cost approaches exist albeit with tradeoffs in performance. We examined an FR4 PCB backplane with 3000 MiniLEDs and 770 zones, it currently costs 2.8x more than edge-lit backlights and is expected to fall to 2.3x in 2025 with the $US difference falling to under $35.

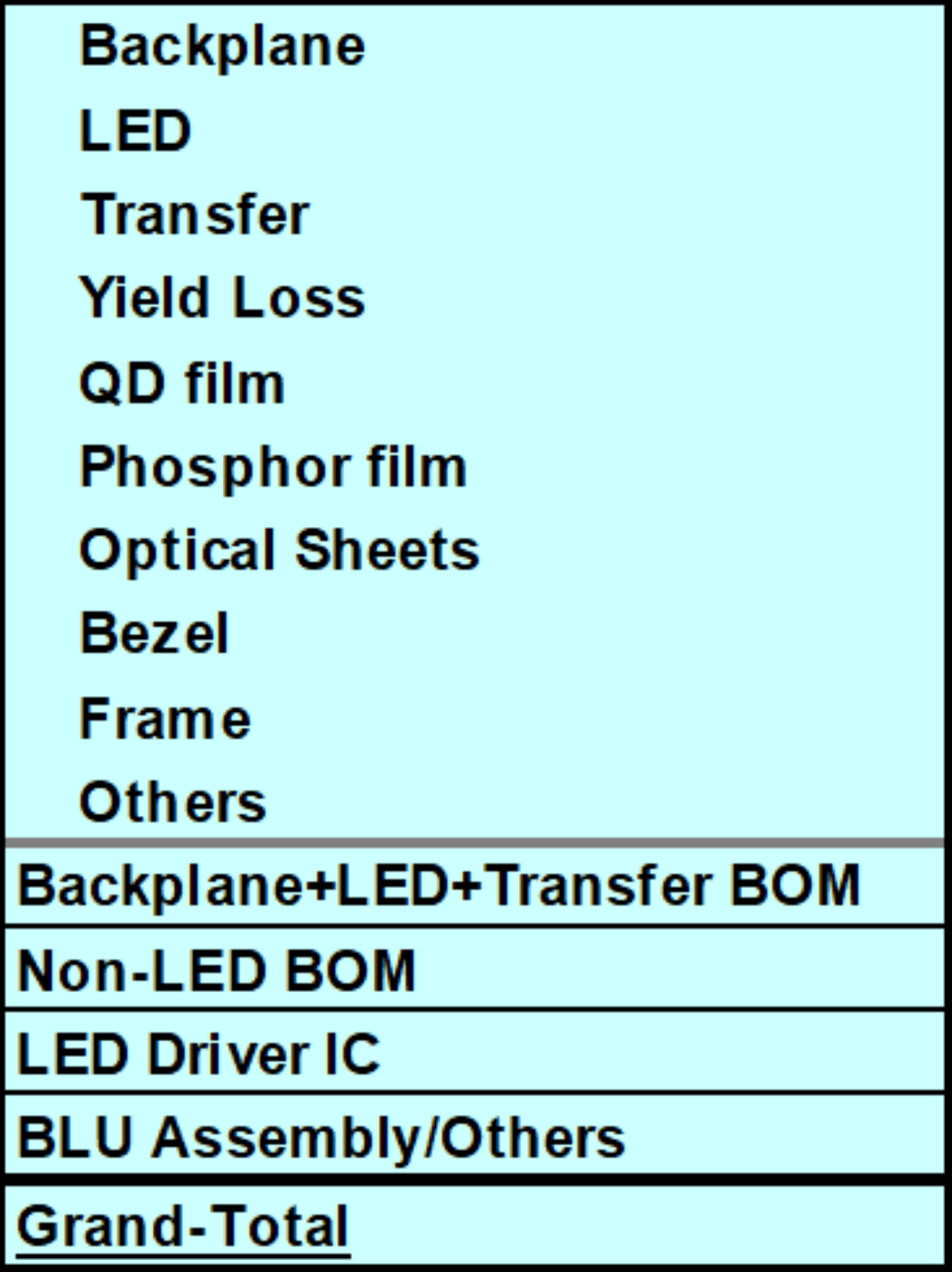

We also examined the MiniLED BLU bill of materials (BoM). We looked at the items in the table below and provided them for each application and BLU type and forecasted them out to 2025. In the Apple MiniLED BLU, they are using a phosphor film rather than a QD film. In the COB type, the LED costs make up a smaller share of the total costs with the backplane, transfer and LED driver IC costs higher. The LED costs are 50% higher in the POB type due to the package costs. But the backplane and transfer costs are significantly more for the COB type. The largest opportunities for cost reduction in the COB type are from reduced yield loss as backplane yields rise as well as 9-12% CAGR declines in backplanes, LEDs, phosphor films, LED driver ICs and Other. The largest opportunities in the POB type are also from reduced yield loss as backplane yields rise as well as 9-12% CAGR declines in LEDs, phosphor films, LED driver ICs and Other.

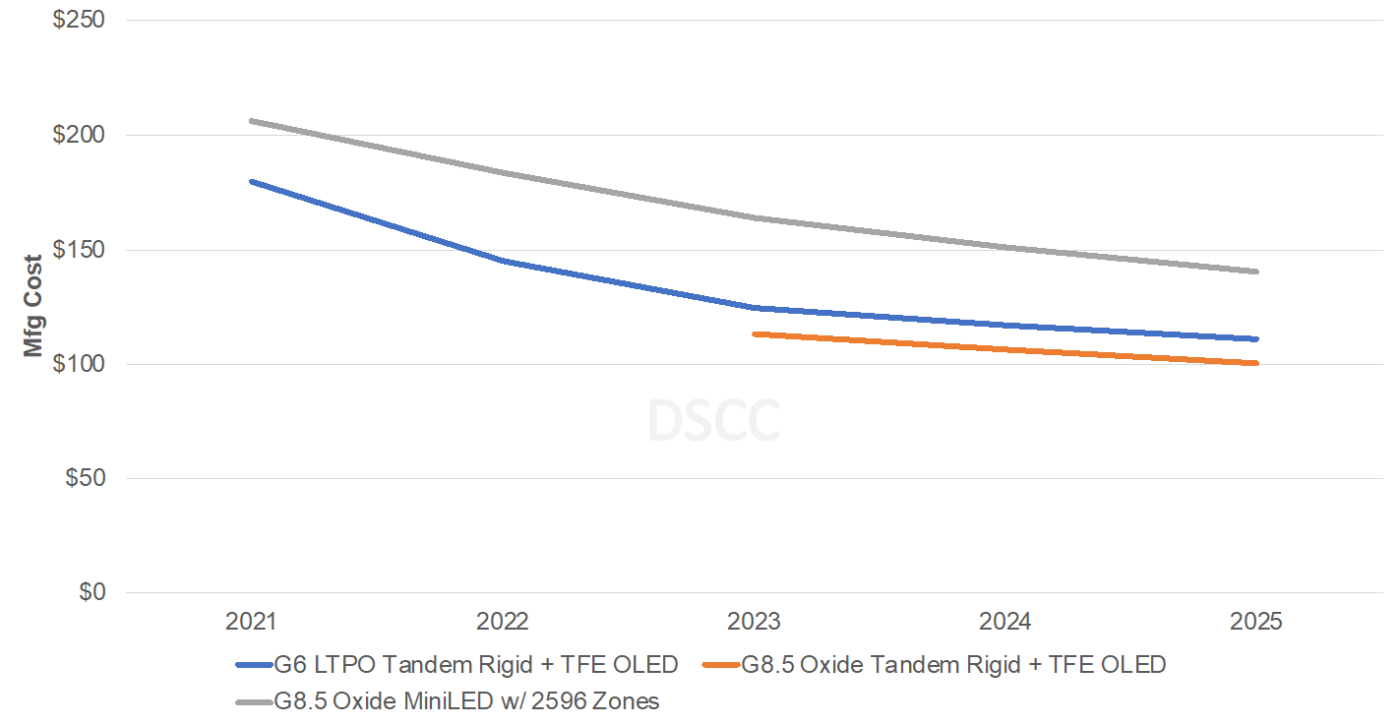

We also examined the panel BoMs and showed that the MiniLED BLU accounts for 60% of the 12.9” MiniLED panel manufacturing costs, by far the highest component. 12.9” manufacturing costs are currently estimated at $206 and are expected to fall at 9% per year to $140 in 2025 with BLUs falling at 11% per year. Similar data and analysis are provided at 16.2” and 27”.

In the case of OLEDs, we looked at fab utilization, yields and also looked at G6 RGB OLED vs. G8.5 RGB OLED assuming FMM VTE equipment. In tablets and notebooks, we assumed tandem structures and rigid + TFE substrates. For G6, we assumed LTPO with G8.5 using oxide. At 12.9”, the G8.5 fabs produce 9% lower manufacturing costs while at 16”, G8.5 resulted in 16% lower manufacturing costs with G6 not optimized for 16.2” at 24-up for G6 vs. 63-up at G8.5. At 27”, we assumed a single stack with rigid + TFE substrates.

We then compared MiniLED vs. OLED costs. For 12.9”, as indicated below, we show OLEDs maintaining a cost advantage vs. the MiniLED premium solution throughout the forecast. If that is the case, why did Apple go with MiniLEDs? Their decision may have been more about having multiple MiniLED panel sources than a single OLED source. In addition, tandem structures aren’t available yet in the tablet market. We do expect Apple to move to OLED when LGD can supply these panels in addition to SDC. Although MiniLEDs are shown falling at a double-digit rate, then can fall even faster if Apple opts for a solution with fewer MiniLEDs and zones as other brands are likely to do.

OLED vs. MiniLED Panel Manufacturing Costs

The results are different at 16.2” due to the lack of optimization on G6 OLED fabs. However, when better optimized G8.5 oxide RGB OLED fabs become available, we expect G8.5 to have a double-digit cost advantage. On the other hand, at 27” with a lower cost MiniLED implementation with just 5000 MiniLEDs and 1152 zones, we expect MiniLEDs to have a cost advantage even compared to G8.5 oxide RGB OLED fabs. For more information on our Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします), please contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced IT Panel Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。