国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 10/11/2021

Slowdown in TV Market Driving LCD Oversupply

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

The TV market in the second half of 2021 is slowing down, which is the main factor in an increasing oversupply in the LCD industry. Because of the long-time lag required to bring new capacity online, the pandemic-driven supply shortage that started in 2020 extended to the middle of this year, but panel supplies continued to increase in Q3 despite the industry shifting to oversupply. Even a slowdown in Q4 2021 will not absorb an inventory overhang which will persist into 2022.

Digitimes reported this week that many of the world’s top TV brands had lowered their sales goals for 2021:

- Samsung: from 48M TVs to 45M;

- TCL: from 30M TVs to 25M;

- Hisense: from 24M to 20M;

- Sony: from 10M to 8M.

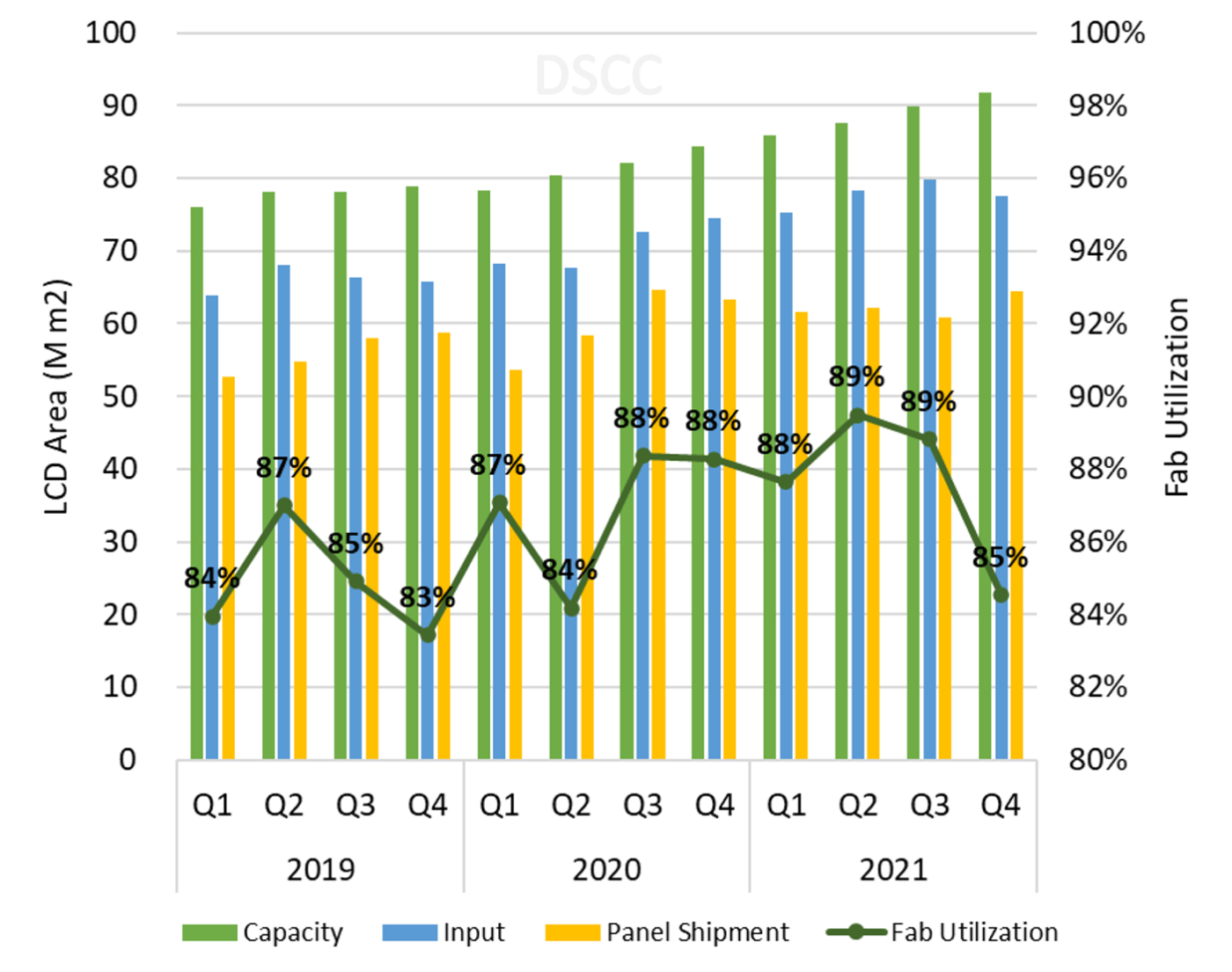

The reduction in TV demand has led DSCC to revise its view of overall industry supply/demand for 2021 and into 2022 with a preliminary update to DSCC’s Quarterly Flat Panel Display Supply/Demand Report (一部実データ付きサンプルをお送りします). As shown in the chart here, DSCC estimates that LCD capacity increased 2.7% Q/Q and 9.4% Y/Y in Q3 2021, and fab utilization held close to steady at 89%, down a fraction of 1%. So, area input in the industry increased by 2% Q/Q but panel shipments decreased by 2% Q/Q. The decrease in panel shipment area was primarily driven by reduced LCD TV panel shipments, down 6% Q/Q.

Even before Q3, TV inventories downstream from the panel makers had been increasing at TV set makers and retailers. The imbalance in supply/demand has been exacerbated by the continued oversupply in Q3. Although DSCC now expects fab utilization to slow down to 85% in Q4, industry capacity is increasing by 2% so the reduction in input area is only 2%. This reduction will not be sufficient to absorb the excess inventory in the industry, which will carry over into 2022.

LCD Area Capacity, Input, Shipments and Utilization, 2019-2021

Just one week ago, DSCC released our monthly update of LCD TV panel prices, expecting a severe price drop of nearly 30% Q/Q in Q4 2021. With the reduced outlook for the TV market, the pressure on panel prices is likely to continue to push downward.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。