国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 10/11/2021

New DSCC Report Quantifies OLED vs. MiniLED Competition in Tablets, Notebooks and Monitors

Ross Young, Founder and CEOAustin, TX USA -

Last weekend there was a heavyweight championship fight between the UK’s Tyson Fury and the USA’s Deontay Wilder. But, DSCC has been working to quantify another heavyweight fight between OLEDs and MiniLED backlit LCDs in the tablet, notebook and monitor markets.

The battle between OLEDs and MiniLEDs is expected to last for years. Both are likely to see tremendous growth and could be labeled winners as will the consumer who will enjoy better performing displays at lower and lower prices. In each application, the dynamics of which technology will enjoy higher volumes will depend on many different factors including:

- Display cost;

- Display brightness;

- Display power consumption;

- Display lifetime;

- Number of suppliers;

- Ability to dual source;

- Brand strategy;

- Panel supplier strategy;

- Optimized OLED capacity growth;

- MiniLED capacity growth;

- And more.

We have now published our results and forecasts for OLED vs. MiniLED displays in our Quarterly Advanced IT Panel Shipment and Technology Report (一部実データ付きサンプルをお送りします) which includes shipment results and forecasts by:

- MiniLED LCD vs. OLED

- Brand

- Panel supplier

- Display size

- Display resolution

- Refresh rate

- Backplane technology (a-Si vs. IGZO vs. LTPS vs. LTPO)

- OLED frontplane type (FMM RGB OLED vs. WOLED vs. QD-OLED vs. IJP RGB OLED)

- OLED stack (single vs. tandem)

- Rigid vs. flexible vs. foldable

- MiniLED backplane

- MiniLED zones

- # of MiniLEDs

- Touch type (add-on vs. in-cell vs. touch on TFE)

- Cover glass

- CoE vs. polarizer

- Hole vs. Notch vs. UPC vs. None

- Chipset supplier

- Chipset

- Design rules

- RAM

- Storage Size

- Cellular network

- # of cameras

- Battery

- OS

- Stylus support

- And more

Q3’21 highlights for advanced tablets include:

- Advanced display tablets rose 4% Q/Q and over 500% Y/Y to 1.8M in Q3’21.

- The Apple 12.9” MiniLED iPad Pro was the #1 tablet with an advanced display with a 56% share. The Huawei Mate Pad Pro was #2 with an 11% share followed by the Samsung Galaxy S7+.

- Sharp was the leading tablet panel supplier due to its strong position in the Apple iPad Pro. EDO was #2 and was #1 in OLED tablets, ahead of SDC.

- MiniLEDs led OLEDs with a 56% to 44% share on a panel shipment timeline.

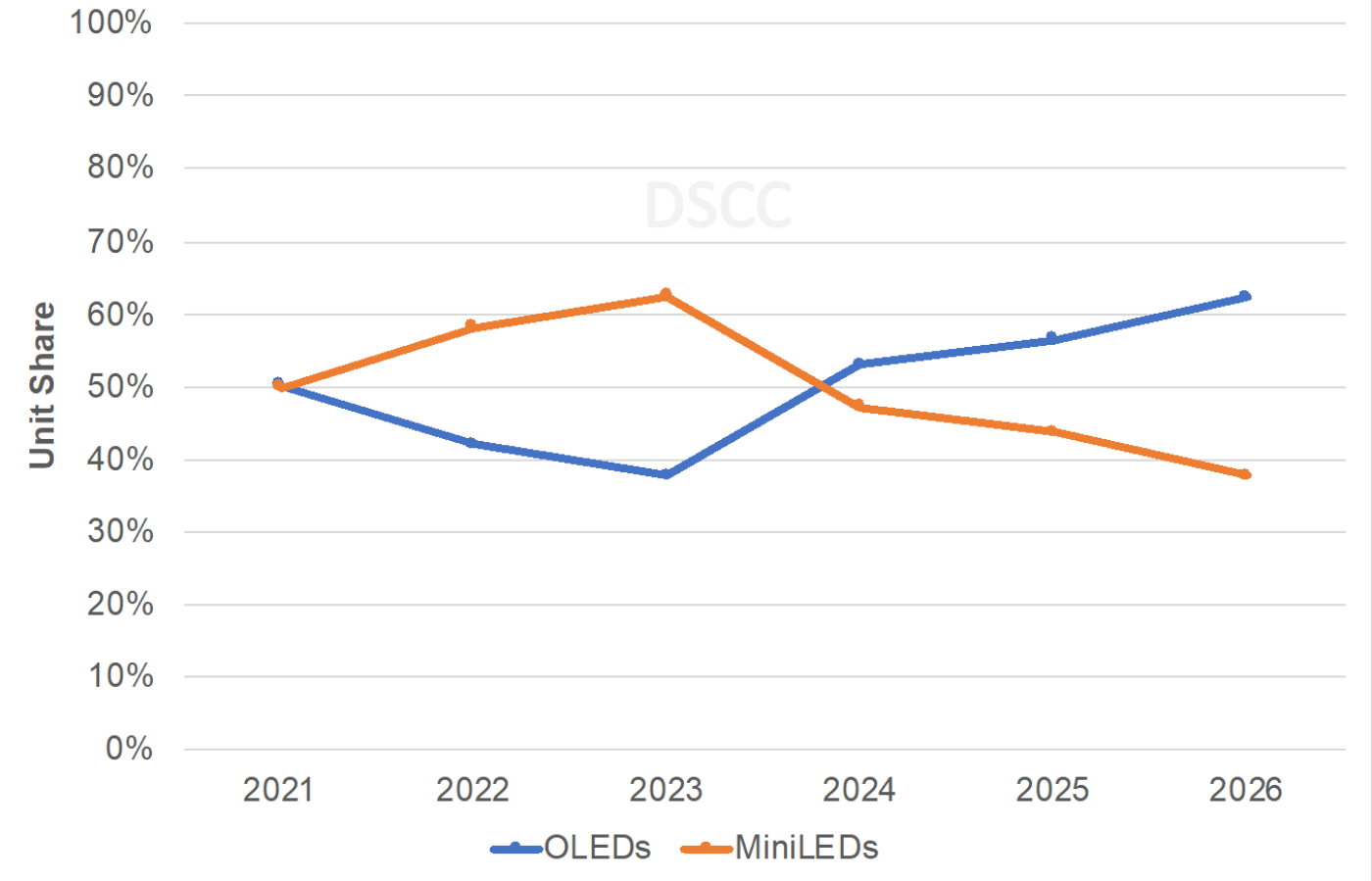

- Competition in tablets is expected to be dominated by brand technology choices. Apple is the leader in advanced tablet displays and their display technology choices will be the largest indicator of which technology is likely to win this market. DSCC expects Apple to adopt OLEDs in 11” and 12.9” iPad Pro models in 2024 which will swing the tablet market from MiniLED to OLED as shown below. Improved OLED performance through tandem structures along with low cost/thin/light weight rigid+TFE implementations will boost the OLED outlook. We do expect Apple to introduce an 11” MiniLED iPad Pro in 2022. We also believe Apple will scale MiniLEDs in tablets beyond 12.9” in the forecast period.

Advanced Tablet Forecast

Q3’21 highlights for advanced notebooks include:

- Advanced notebook display shipments fell 20% Q/Q while rising 370% Y/Y in Q3’21 to 1.2M. Q3’21 shipments were somewhat constrained by chip shortages. In Q4’21, advanced display shipments to the notebook market are expected to rise 152% Q/Q and 1050% Y/Y to 3.0M panels.

- OLEDs accounted for nearly 100% share in Q3’21, but MiniLEDs should account for around 1/3 of the market in Q4’21 due to Apple launching new MiniLED Apple MacBook Pro’s at 14” and 16”. SDC is also expected to enjoy significant growth in Q4’21 as it aggressively promotes its OLED notebook panels.

- The Asus Vivobook Pro 14 consumed the most advanced panels in Q3’21 followed by the Samsung GalaxyBook Pro.

- Asus had the highest share in Q3’21, but Apple is expected to lead in Q4’21.

- SDC was the dominant panel supplier in Q3’21 with nearly a 100% share. In Q4’21, its share will likely fall to 67% as MiniLEDs gain share.

- DSCC expects OLEDs to lead this segment in 2021 with an 84% share and to continue to maintain the leading share over the forecast period despite gains by MiniLEDs. Apple’s eventual migration to OLEDs will also help the OLED cause.

- The report goes into detail explaining how OLED performance will improve and how both OLEDs and MiniLEDs are likely to reduce cost to succeed in notebooks. The adoption of lower cost G8.5 oxide FMM VTE RGB OLED fabs will boost OLED capacity while reducing costs and the adoption of increased pin count LED driver ICs with more zones per chip and single sided backplanes will reduce MiniLED costs.

Q3’21 highlights for advanced monitors include:

- Shipments rose 44% Q/Q and 450% Y/Y in Q3’21 to over 250K panels and should rise 2% Q/Q and 189% Y/Y in Q4’21 to close to 270K panels.

- MiniLEDs led Q3’21 with an 87% share and should continue to dominate this segment through 2026. However, OLEDs will gain share from increased allocation at TV fabs in 2022 from LGD and SDC and optimized, lower cost fabs in 2025/2026 from RGB OLED fabs. The report addresses which OLED technology is best positioned over time in the monitor market.

- Asus was the #1 brand in Q3’21 with a 42% share and should lead in Q4’21 as well.

- 32” was the #1 size with a 78% share.

- AUO was the #1 panel supplier with a 61% share.

The report also includes:

- Brand product roadmaps

- Panel supplier roadmaps

- Display technology roadmaps

- Analysis of key display technology advances

- Panel cost forecasts by technology by size, etc.

- Panel price forecasts by technology by size, etc.

- And more.

For more information on the Quarterly Advanced IT Panel Shipment and Technology Report, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。