国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 09/13/2021

Worldwide TV Shipments Continued Recovery in Q2, per DiScien Report

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

In 2020, the COVID-19 pandemic caused big shifts in TV shipments caused by supply and demand disruptions, but on a worldwide basis, the full year ended up about where it was expected to land, with TV shipments up 1% for the full year over 2019. TV shipments in the first half of 2021 have continued to recover past pre-pandemic levels on a worldwide basis, but with some great differences between regions, according to the latest update of the DiScien (※DSCCの提携調査会社) Major Global TV Shipments and Supply Chain Report, available to subscribers through DSCC. The report covers shipments of the top 15 global brands: Samsung, LGE, TCL, Hisense, Sony, Skyworth, TPV (Philips), Sharp, Xiaomi, Vizio, Haier, Panasonic, Changhong, Konka and Toshiba.

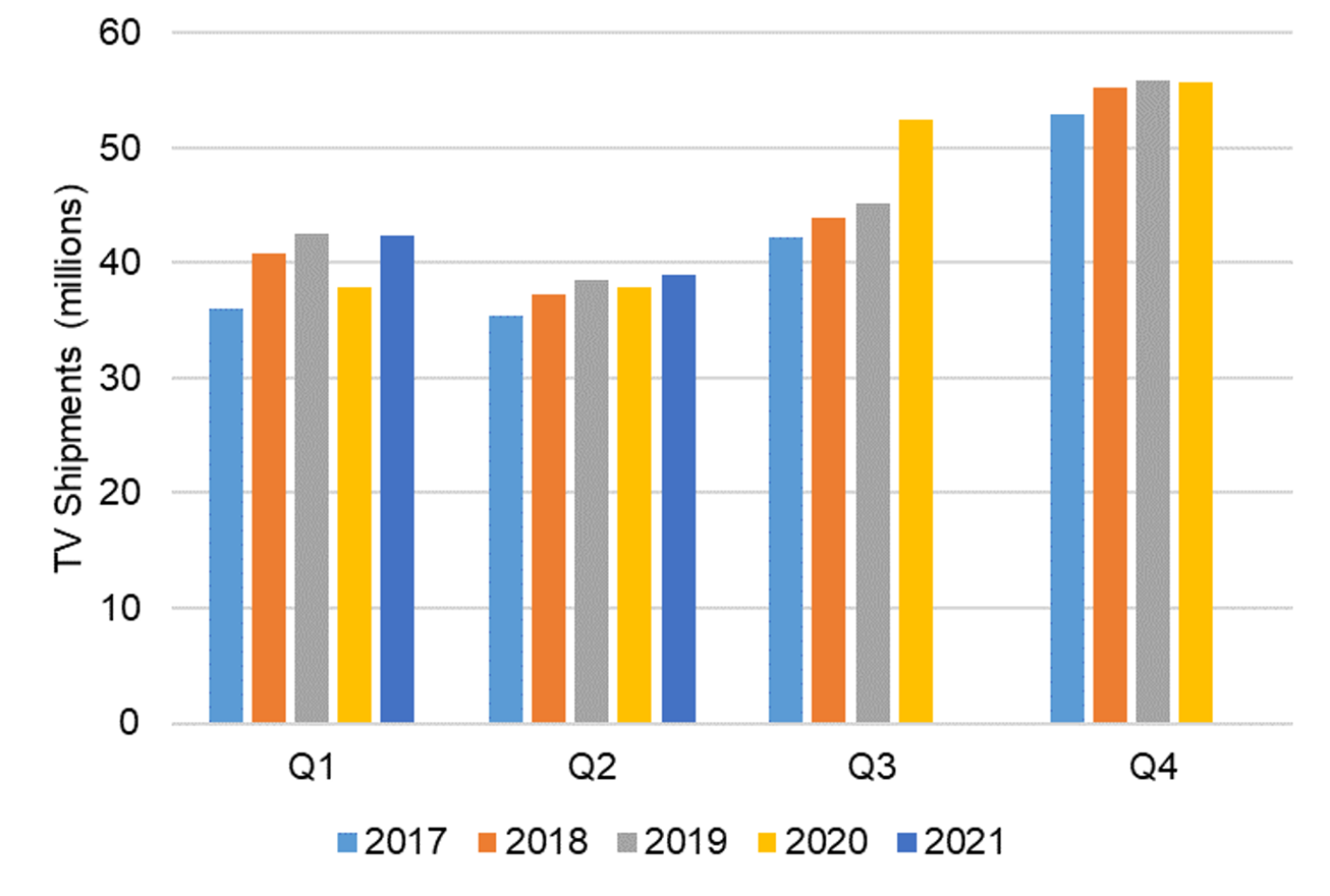

Q2 2021 worldwide TV shipments totaled 40.0M, an increase of 3% over Q2 2020 and an increase of 1% over Q2 2019. The relatively calm worldwide picture masks some big differences in the performance by region, which just happen to offset each other.

Global TV Shipments of Top 15 Brands by Quarter, 2017-2021

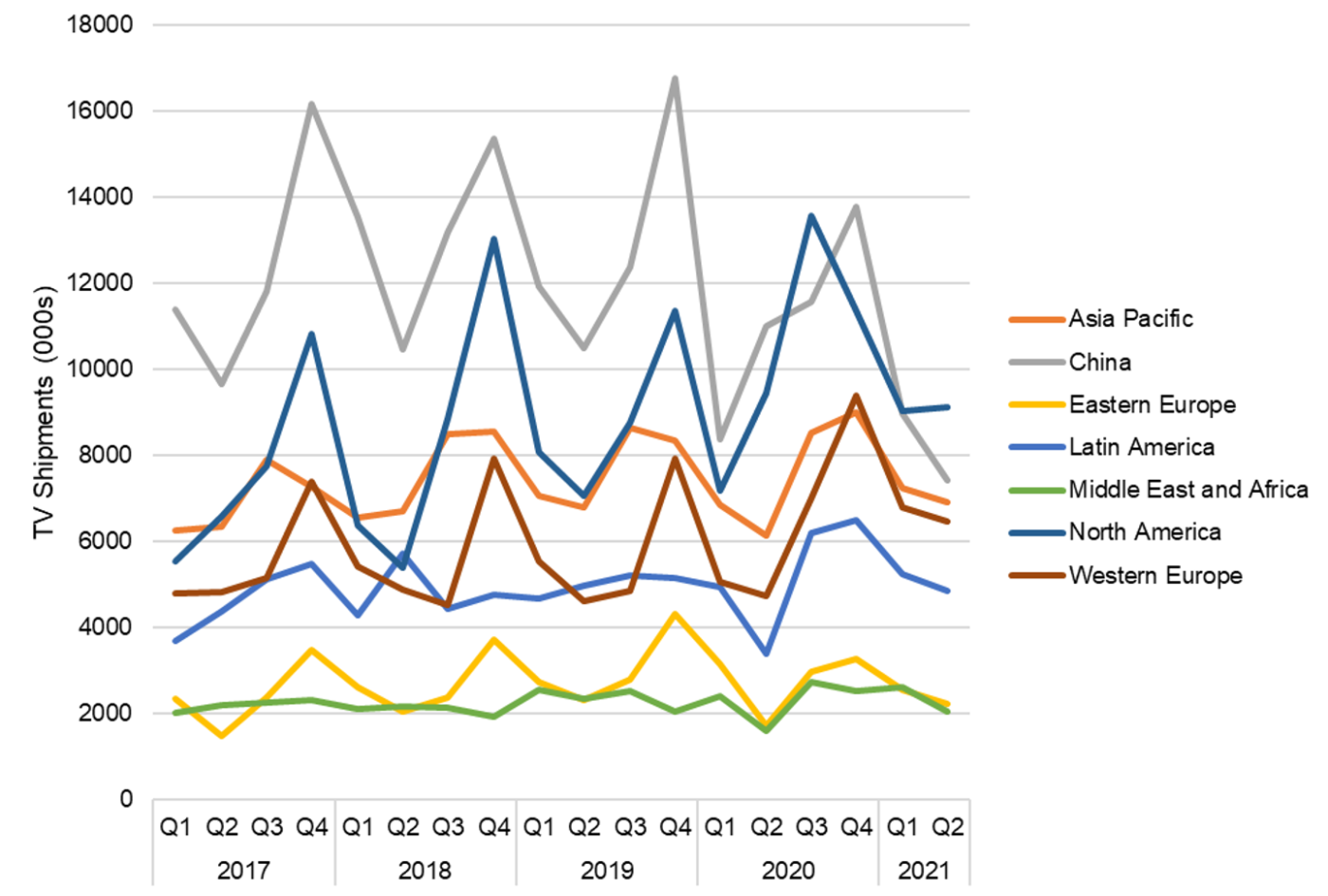

On a regional basis, compared to the pre-pandemic level of Q2 2019, the good news primarily came from the developed regions of North America and Western Europe. This was nearly offset by a drop in the market in China. North America TV shipments decreased 4% Y/Y compared to Q2 2020, but pandemic demand was already surging in North America in the spring of last year, and shipments were up 29% from Q2 2019 levels to 9.1M. Western Europe shipments in Q2 2021 increased by an even stronger 37% Y/Y to 6.5M units, which was a 40% increase over Q1 2019.

In both regions with continued strong demand, three factors have combined to support the TV market. First, government support for consumers has kept incomes stable. Second, the pandemic lockdowns have forced stay-at-home consumers to find entertainment with new TVs. Third, the relative affluence of these regions makes them much less sensitive to higher TV prices.

China, which before the pandemic was the biggest regional market, appears to be going in the other direction. TV shipments in China decreased by 32% from Q2 2020 and they were down 29% from Q2 2019 at 7.4M. For the third time in the last five quarters, China was surpassed by North America as the largest regional market. Compared to the developed regions where demand has been strong, China has shared the first factor – stable incomes – but has not had lockdowns to the same extent. The China market is more sensitive to prices, particularly because most of the local brands must buy LCD TV panels on the open market, rather than benefitting from higher prices as part of a vertically integrated corporation (the exception to this is TCL/CSOT).

The markets in Eastern Europe, Latin America and MEA have all recovered from a pandemic-driven low point in Q2 2020 with big Y/Y increases, but shipments to each of those three regions remained lower than Q2 2019. Shipments in the Asia Pacific were up 12% Y/Y and up 2% over Q2 2019 levels.

TV Shipments of Top 15 Brands by Region, 2017-Q2 2021

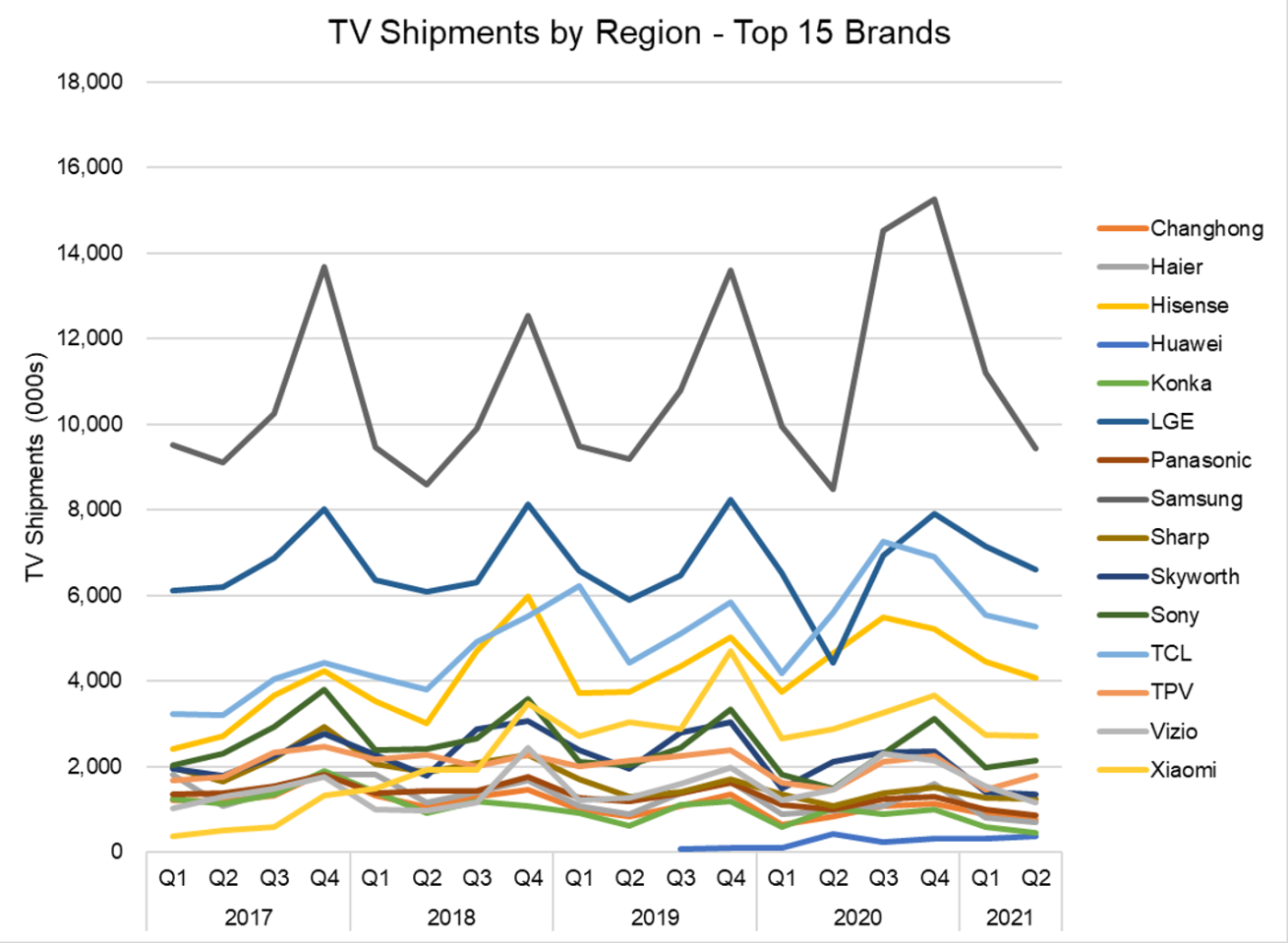

Among the top brands, given the regional market dynamics, the brands relying on the China market have fared poorly, while brands that are stronger in NA and WEU have done well. As shown in the next chart, Samsung continues to lead the industry and improve its position, increasing shipments by 11% Y/Y and by 3% compared to Q1 2019. LG Electronics has fared even better, reclaiming the #2 spot from TCL, with shipments increasing 49% Y/Y and 12% compared to Q2 2019. Sony also benefited from the surge in demand in North America and Western Europe, with shipments up 45% Y/Y and 6% compared to Q2 2019 at 2.1M.

Within the brands based in China, the two with the greatest focus on the international market fared the best. TCL saw shipments decrease by only 6% Y/Y to 5.3M, and this was up 19% from the figure in Q2 2019. Hisense shipments of 4.1M were down 13% Y/Y, but up 9% compared to two years ago. Other Chinese brands had double-digit percentage drops compared to Q2 2019, including Haier, Konka and Skyworth.

TV Shipments of Top 15 Brands, 2017-Q2 2021

The DiScien (※DSCCの提携調査会社) Major Global TV Shipments and Supply Chain Report covers TV shipments from the top 15 global brands and provides shipment information by screen size, resolution, and region, allowing users to analyze market demand, brand dynamics and product trends by region. DSCC Weekly Review readers interested in subscribing to this report should contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。