国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 08/30/2021

OLED Shipments Expected to Increase 12% Y/Y in 2H 2021

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

OLED panel shipments will increase by 12% Y/Y in the second half of 2021, according to the flash update of the DSCC Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします), as increased panel shipments for smartphones combined with growth in IT applications drives the technology toward the mainstream. Starting in Q2’21, we introduced an expedited “flash” deliverable in advance of the full report file. This flash edition analyzes quarterly and annual units through 2022 by application, panel supplier, brand and form factor.

The Q3 Flash update of this report gives actual shipments through Q2 2021 and DSCC’s forecast for Q3 and Q4 2021, with detailed figures for units and splits by application, panel supplier, substrate (rigid/flexible/foldable) and brand. Last week we covered the smartphone results, and this week we will address the other applications. Subscribers to the report, of course, can see all the results in the Excel file.

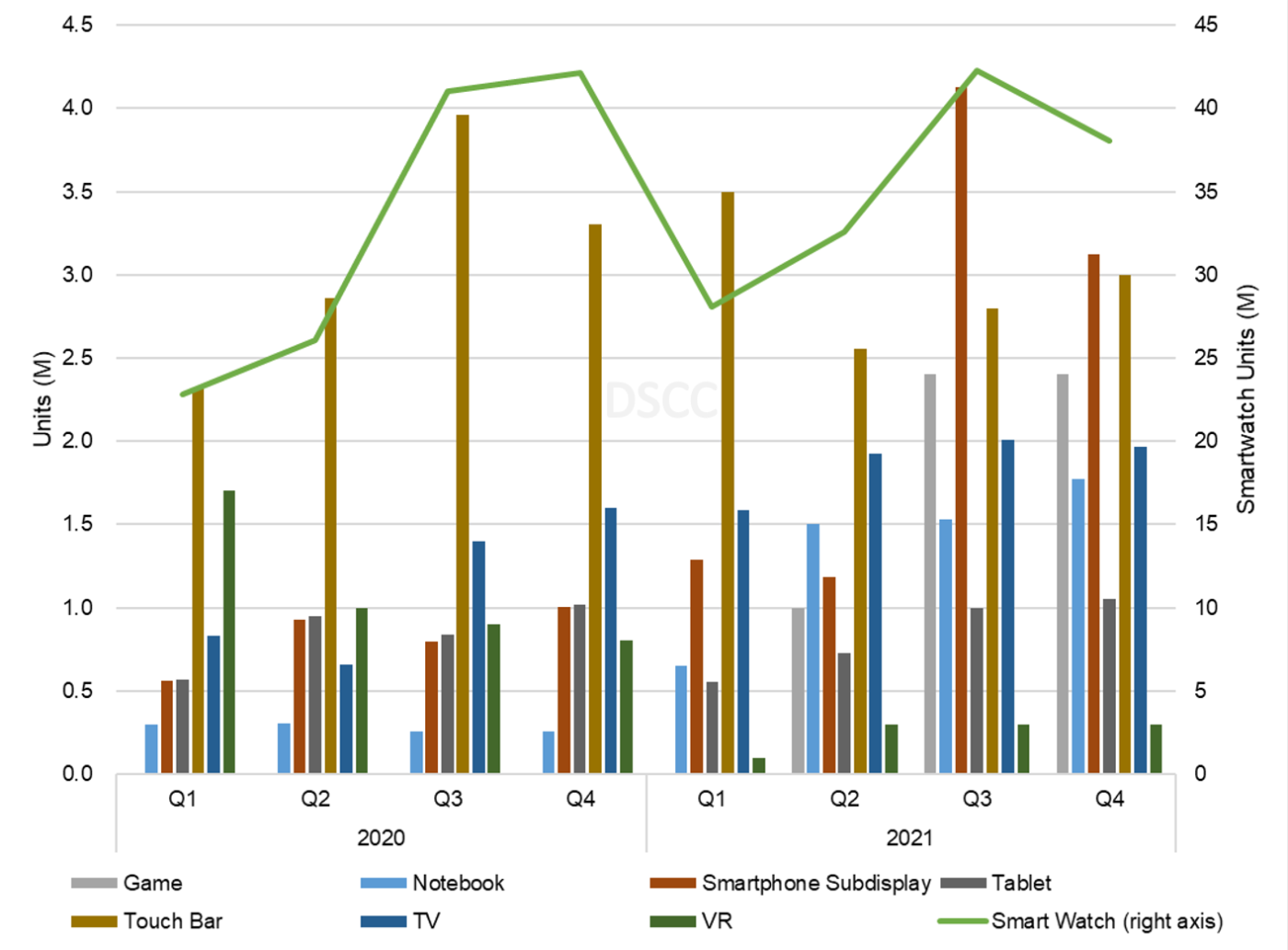

Although smartphones make up about ¾ of OLED panel shipments in unit terms, shipments in other applications are showing even more impressive growth, as shown in the first chart. Panels for games, in particular the Nintendo Switch, are growing from nothing in 2020 to 4.8M in the second half of 2021. Notebook panel shipments are expected to grow by 550% Y/Y to 3.3M units in the second half, and shipments of OLED panels for smartphone subdisplays are expected to grow 303% Y/Y as they are increasingly important for foldable smartphones.

While the percentage growth is less impressive, the unit growth in OLED TV panel shipments may be more important to the industry than those smaller applications. OLED TV panel shipments are expected to grow 32% Y/Y in the second half of 2021 to 4.0M units, bringing the total shipments for the year to 7.5M.

Quarterly OLED Panel Shipments by Application, 2020-2021

While most applications will see growth in OLED panel shipments, a few applications are expected to decline in 2021. The most important of these is smartwatches, which have surged in recent years to become the #2 category for OLED panel shipments in unit terms. We expect that 80M smartwatch panels will be shipped in the second half of 2021, but this is down 3% from last year. We believe that the smartwatch category is mostly saturated, and the lack of a compelling Apple Watch upgrade suggests a pause in growth. Similarly, we expect that OLED panels for touch bars will decline by 20% Y/Y in 2H’21, as Apple is not expected to announce major upgrades to its MacBook series.

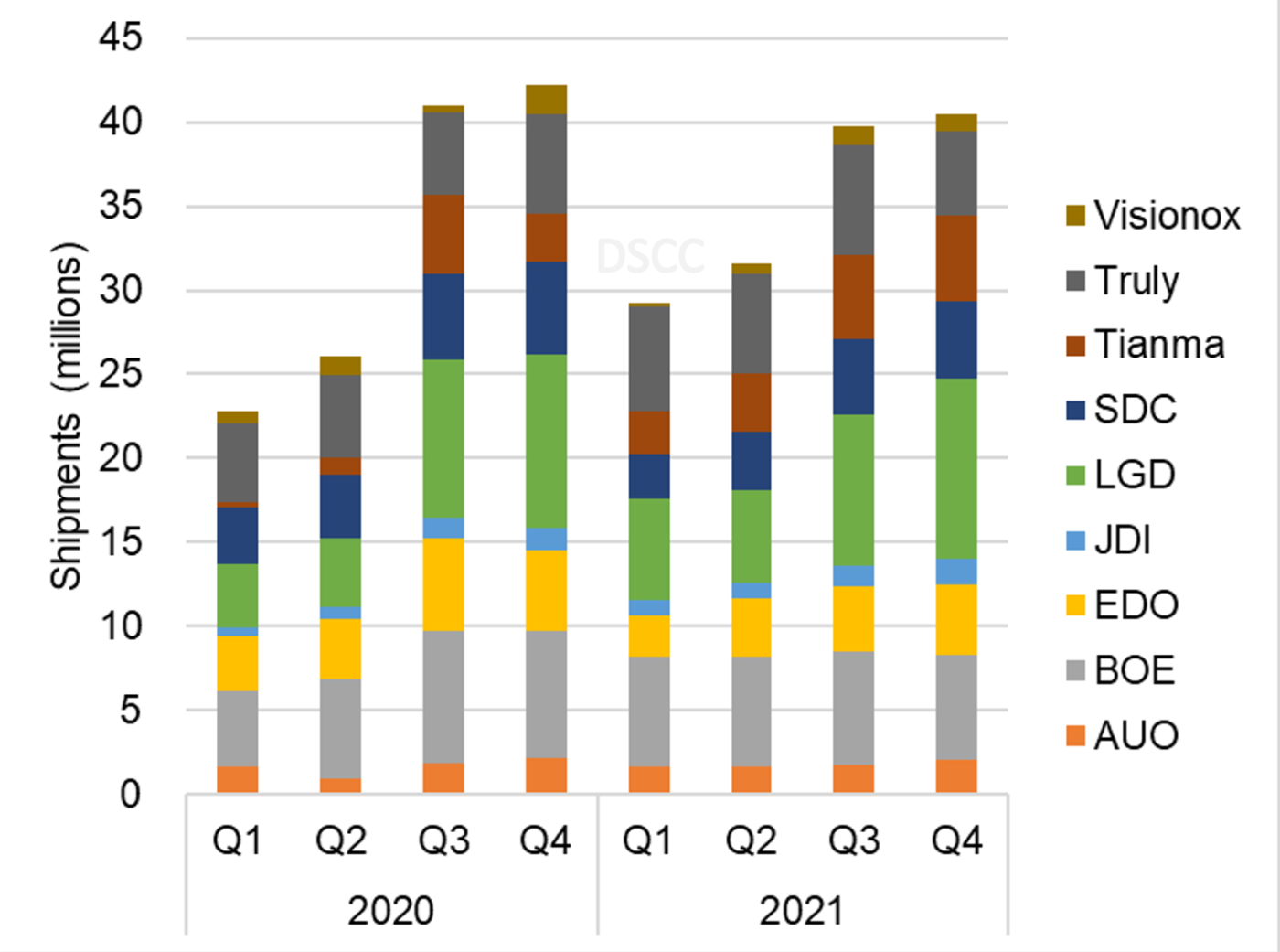

The next chart shows the market for smartwatch panels by panel maker. While Samsung dominates the smartphone panel market, and LG Display has a monopoly on TV panels, the market for OLED smartwatch panels remains a true battleground. LGD is expected to lead the market in 2H’21, with 23% share based on supplying a majority of the panels used in the Apple Watch, but BOE, Truly, Tianma and SDC are all expected to garner at least 10% share of this category.

Quarterly OLED Smartwatch Panel Shipments by Panel Maker, 2020-2021

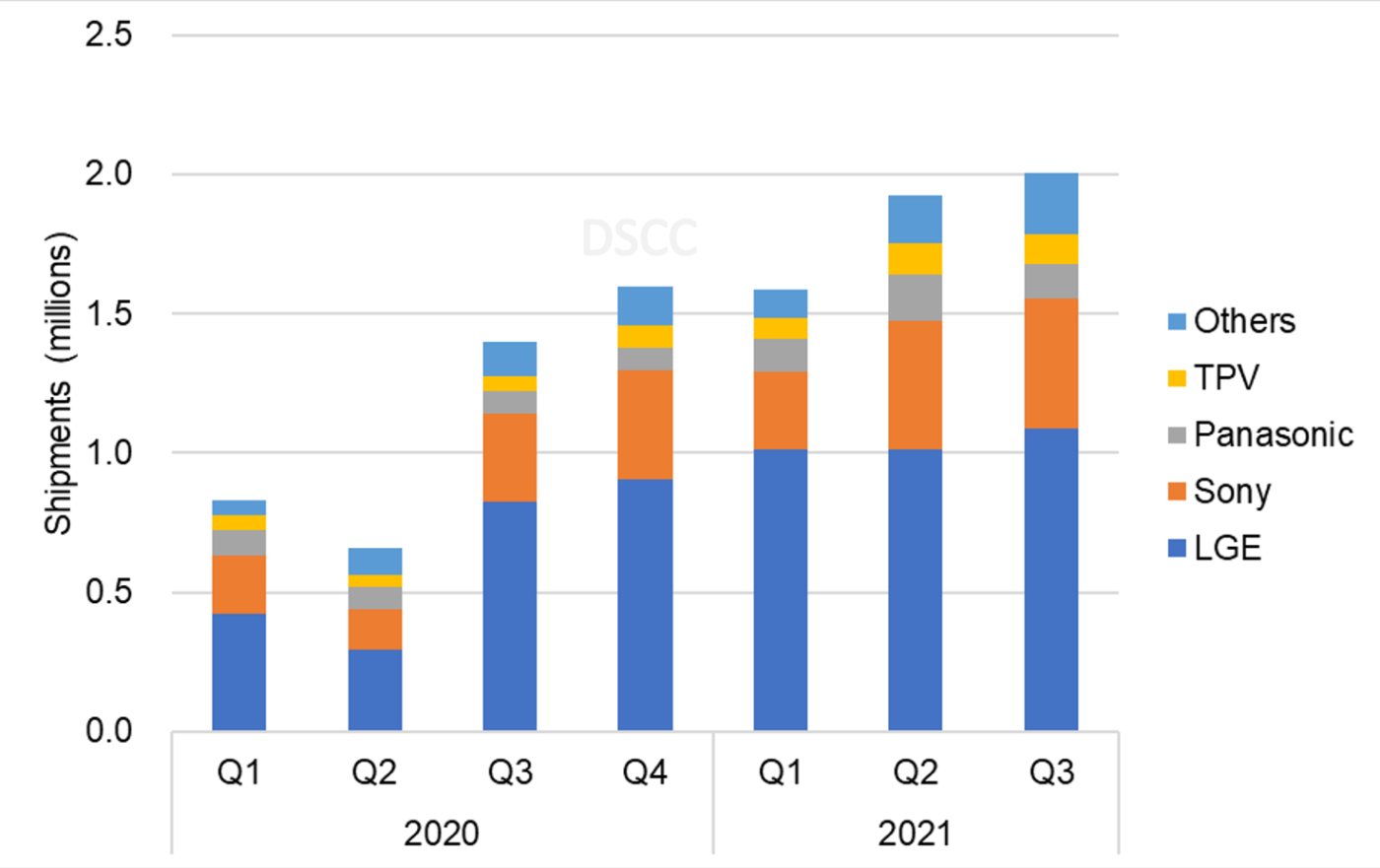

In TV, the growth of OLED shipments has been driven by growth among all the major brands, as shown in the next chart here. Shipments were constrained by the pandemic in Q2 2020, so Q2 2021 saw unusually high percentage growth, with an increase of 192% Y/Y. Each of the top four brands had more than 100% growth Y/Y in Q2 2021. The growth is expected to continue in Q3 with LGE’s OLED TV panel procurement increasing 32% Y/Y as the slowest growth among the top four. OLED TV panel shipments to Sony are expected to increase by 46% Y/Y, and shipments to Panasonic and TPV (Philips brand) are expected to increase by 54% and 115%, respectively.

Quarterly OLED TV Panel Shipments by Brand, 2020-2021

LGE’s share of OLED TV panel procurement is expected to remain above 50% in Q3 2021 at 54%, down from 59% in Q3 2020. Sony’s and Panasonic’s shares are expected to remain stable Y/Y at 23% and 6%, respectively, while the share for TPV/Philips is expected to increase from 4% to 5%. Among the other brands, Skyworth has the biggest portion of OLED TV panel shipments for #5 overall, but Xiaomi and Sharp are both seeing exceptionally large increases in Q3 2021. LGD’s OLED TV shipments to ‘other’ brands (outside the top four) are expected to increase by 75% Y/Y in Q3, and the share of those other brands is expected to increase from 9% a year ago to 11% in the current quarter.

As noted above, the DSCC Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) provides a comprehensive listing of historical panels shipments for all applications, plus a forecast of units, ASPs, screen sizes, resolutions, panel suppliers, and revenues for each application. Readers interested in subscribing to the DSCC Quarterly OLED Shipment Report should contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。