国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 08/23/2021

DSCC Upgrades Foldable Forecast as Chip Shortage Causes Brands and Panel Suppliers to Emphasize More Expensive Devices

Ross Young, Founder and CEOAustin, TX USA -

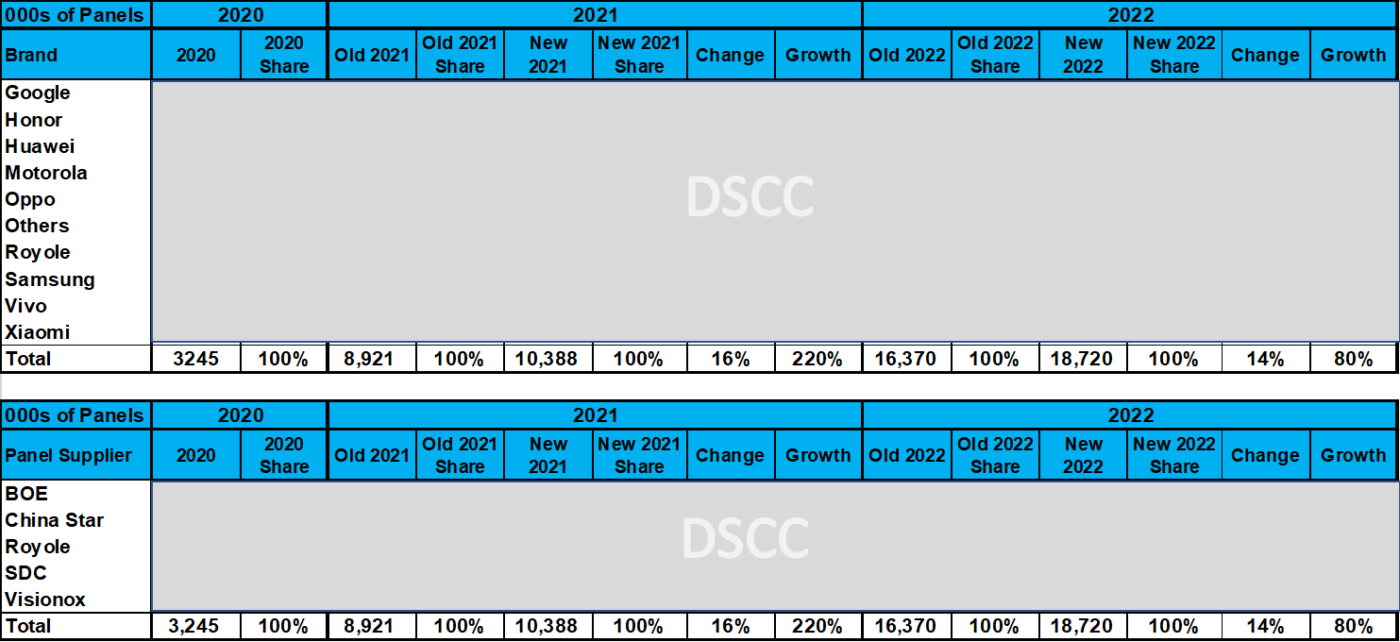

DSCC released a flash report last week as part of its Quarterly Foldable/Rollable Display Shipment and Technology Report (一部実データ付きサンプルをお送りします). The flash report features a pivot table with monthly foldable smartphone panel procurement by brand, panel supplier, size, resolution, cover material, refresh rate, backplane, chipset supplier and other features by month through 2021 and by year for 2022.

A few developments have caused us to upgrade our foldable smartphone panel shipment/procurement numbers by 14% in 2021 to 10.4M and by 16% to 18.7M in 2022 as shown below. As a result, we now see foldable smartphone panels up 220% in 2021 and 80% in 2022. These developments include:

1. Both brands and panel suppliers are prioritizing foldable smartphones and panels due to the semiconductor shortage. Since brands can only get so many processors and panel suppliers can only get so many driver ICs, they are emphasizing higher priced devices and panels to maximize revenues. We are seeing this at market leader Samsung, which is boosting its emphasis on foldables and delaying lower priced devices.

2. Chinese brands Huawei and Honor are getting more aggressive in foldables than we previously estimated.

a. For Huawei, we had conservative expectations given their position on the US entity list. However, they recently extended the life of the Mate X2 by introducing a 4G version and we believe they are preparing a new foldable to launch by the end of the year as well as a new device to launch in 2022. More insight into these devices can be found in our report.

b. For Honor, we increased our forecast for them in 2021 and 2022 based on supply chain checks. They are expected to launch a new foldable smartphone by the end of the year followed by a second-generation device in 2022. More insight into these devices can be found in our report.

3. Samsung has been more aggressive than previously expected with its Z Flip 3 pricing as well as very aggressive with discounts on both the Z Flip 3 and Z Fold 3. Our supply chain checks with visibility to nearly the end of the year have caused us to upgrade our Z Flip 3 panel procurement by 16% and our Z Fold 3 panel procurement by >16%.

Other developments in the report include:

• As Chinese brands and panel suppliers increase their emphasis on this market, Samsung Display’s share is expected to fall to 84% in 2021 and 80% in 2022, still dominant;

• Samsung’s share of foldable smartphone panel procurement is expected to fall from 83% in 2020 to 78% in 2021 and 69% in 2022;

• Updated timing on rollable smartphones;

• Possible ultra-thin glass (UTG) adoption on Chinese made foldable smartphone panels in 2022;

• Under panel camera (UPC) adoption will extend beyond Samsung in 2022 and is predicted to appear on as many as eight models in 2022. The report will include a deep dive on the UPC in the Galaxy Z Fold 3 and other non-foldable smartphones and how this feature is likely to evolve in the next few years;

• The full report will also include the latest outlook for foldable and rollable tablets, notebook PCs and TVs.

If you are interested in learning more about this report, please contact info@displaysupplychain.co.jp.

DSCC’s Foldable Smartphone Panel Forecast Changes

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。