国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 07/19/2021

Latest DSCC Advanced Smartphone Features Report Reveals and Predicts Latest Smartphone Trends – LTPO, Refresh Rates and 5G are Growing

David Naranjo, Senior DirectorSan Diego, CA USA -

[田村喜男の補足解説] iPhoneが2021年新モデルでLTPOを本格採用

DSCCは、スマートフォンのセット、パネルその他の主要構成部材の出荷・技術動向の詳細調査レポート Quarterly Advanced Smartphone Features Report (一部実データ付きサンプルをお送りします) を7月13日に発刊、下記グローバルブログにてその分析概要を速報している。今回さらに著書の視点で短く補足解説したい。

Apple Watchに採用されたLTPOの特徴は、移動度が大きく安定性が高いLTPSを利用していること、そしてTFTの均一性が良く、リーク電流が少ないIGZOの利点を一つに結合した技術である。従来のLTPSベースのフレキシブルOLED採用のApple Watchは、時刻を見るたびにスイッチをオンする必要があった。LTPOを採用することにより、デバイスの消費電力を低減し、時計画面の常時オン状態を実現した。

スマートフォンでは、Samsung GalaxyやSharp Aquos、OppoなどもすでにLTPOを採用しているが、Apple iPhoneでも2021年新モデルでLTPOを採用することになりそうだ。2021年モデル4モデルのうち、6.1” Proと6.7” Pro向けである。これらのLTPOを出荷するフレキシブルOLEDパネルメーカーはSDCのみである。LGDもiPhone向けLTPOパネルを開発中であり、2022年モデルから採用されるようだ。またBOEも開発中であるが、まずはHuawei向けなどが最初の顧客ターゲットとなるであろう。

アジア代表・田村喜男 (7月21日 13:30版)

---------------------

DSCC’s Quarterly Advanced Smartphone Features Report (一部実データ付きサンプルをお送りします) tracks and forecasts all major product trends in the AMOLED smartphone market, in addition to providing supply chain insights. The report provides a comprehensive listing of historical and forecasts insights through 2025 for panel unit shipments, panel suppliers, brands, device revenues, ASPs, models, screen sizes, resolutions, chipsets and much more for feature segmentations for all AMOLED smartphones.

Several of the major trends identified in the report are the rapid adoption of higher refresh rates, LTPO backplanes and 5G network band.

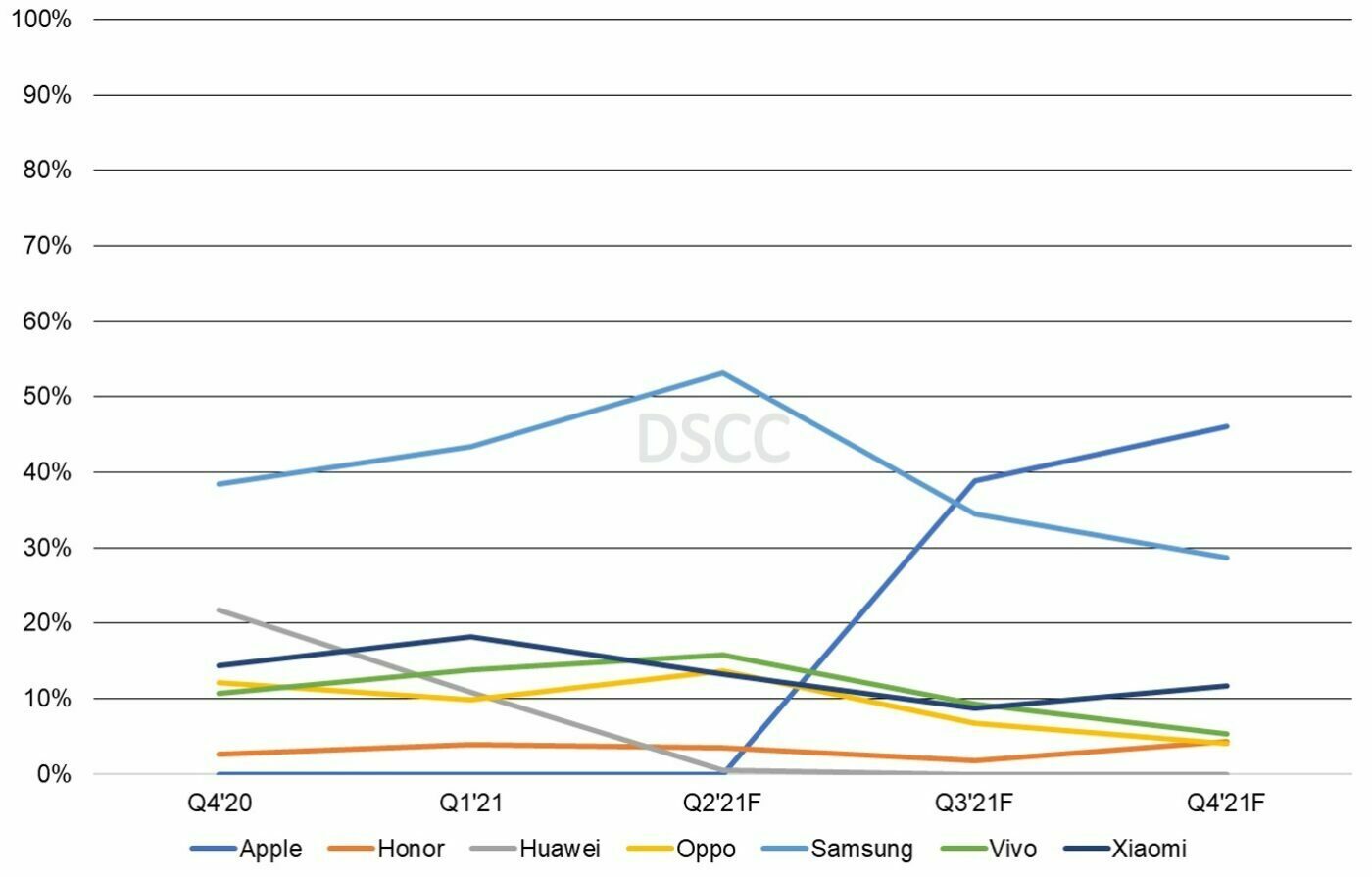

For higher refresh rates, 90Hz and higher panels are taking significant unit share in 2021, with the 60Hz share falling to 63% share in Q1’21 on a unit basis and 61% share on a revenue basis. 90Hz is holding steady and gained unit share in Q1’21 to 12% and is expected to rise to 19% in Q2’21 as a result of new 90Hz smartphones from Samsung, Vivo and Xiaomi. 120Hz also gained unit share in Q1’21 to 25% from 12% in Q4’20 as a result of smartphone introductions with this refresh rate by Samsung, Vivo, Oppo, Honor and Xiaomi. We expect 120Hz to increase to 29% unit share in Q2’21 and 37% unit share in Q3’21. Samsung has dominated the higher refresh market and is expected to continue to do so until Apple launches the 120Hz iPhone 13 Pro and iPhone 13 Pro Max models. We currently show Apple overtaking Samsung at higher refresh rates in Q3’21 with Apple at 39% revenue share. In Q4’21, we expect Apple at 46% revenue share and Samsung at 29% revenue share. On a model basis, in Q3’21, we expect Apple’s iPhone 13 Pro, iPhone 13 Pro Max and Samsung’s Galaxy S21 FE to be the top three models with higher refresh rates.

Quarterly High Refresh Rate (90Hz and Higher) Revenue Share for Top Brands, Q4’20-Q4’21

This continued demand for higher refresh rates is driven by higher refresh rates required for gaming, a small cost increase, a preference to sell more expensive drivers/panels/smartphones during the driver IC shortage and increased LTPO capacity. The report also reveals the latest LTPO fab schedules by panel manufacturer.

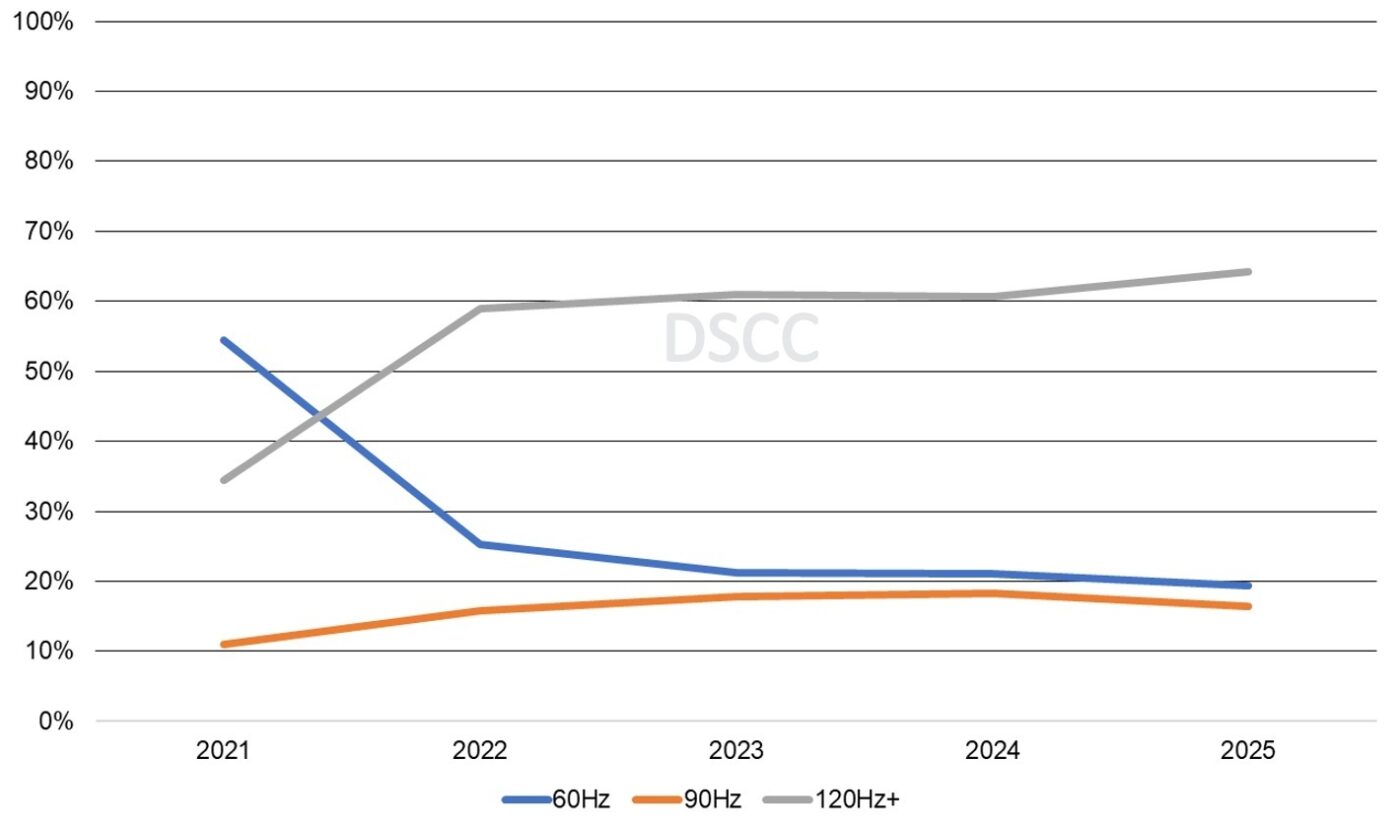

DSCC expects 120Hz to overtake 60Hz by 2022 with 59% unit share and 72% revenue share for the long-term forecast. The >120Hz segment is expected to be small for quite some time as major brands are not working on them. They are likely still a few years away from making large inroads.

Annual Refresh Rate Unit Share, 2021-2025

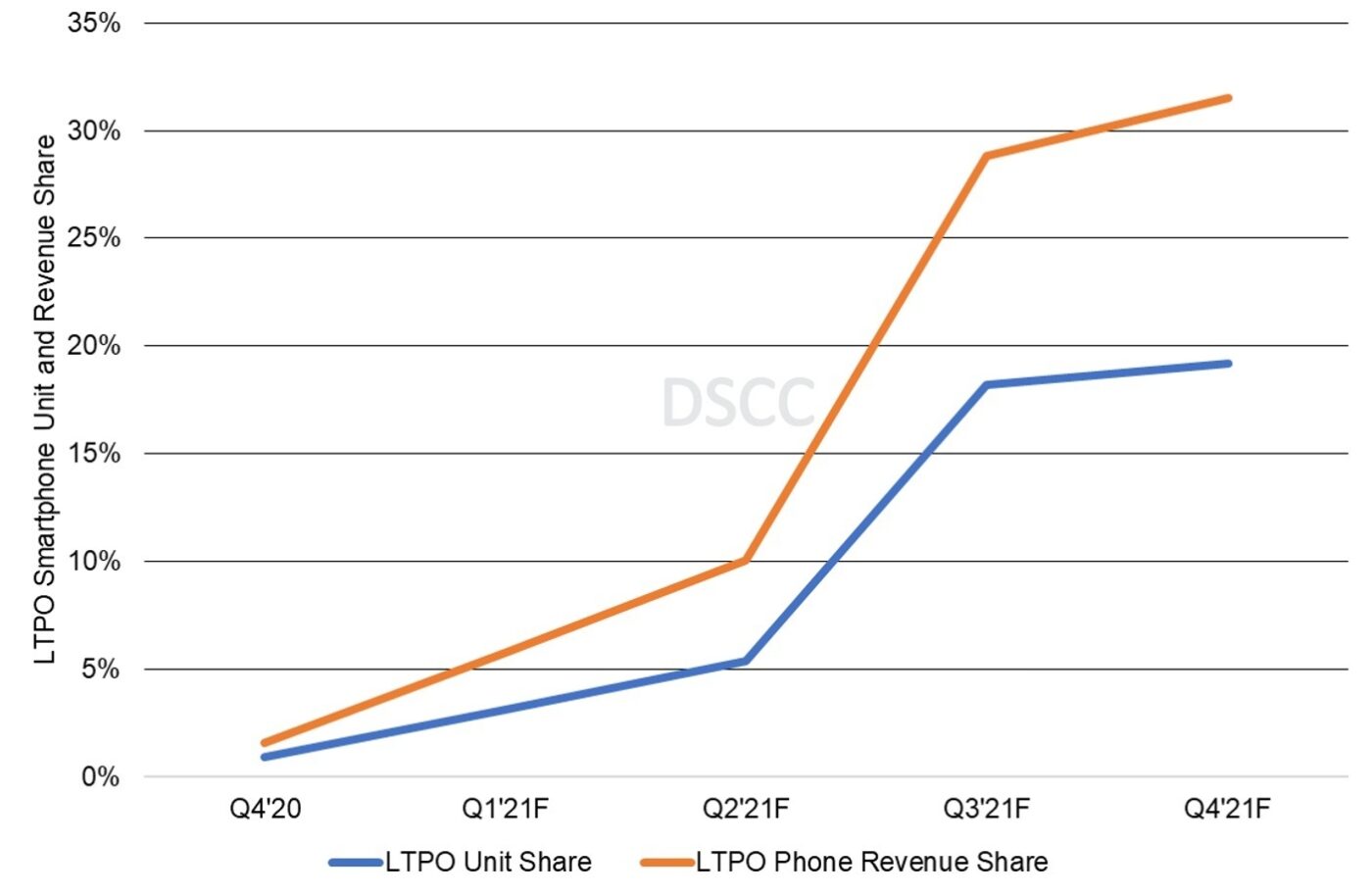

As a result of an increase in LTPO capacity, LTPO backplanes on smartphones are also expected to increase. LTPO replaces the LTPS, switching TFT with oxide. Due to its low off current and stable/flickerless operation at low refresh rates, it can significantly reduce power, allow for variable refresh and enable an always on display mode at low power. Refresh rates in LTPO devices can vary from as low as 1Hz to 120Hz, with overall power consumption declining 15% to 20%. DSCC expects LTPO smartphones to reach a 19% panel unit share and 31% smartphone revenue share by Q4’21. This is fueled by Apple launching iPhone 13 Pro and iPhone 13 Pro Max with LTPO backplanes and other flagship phones launching LTPO smartphones.

Quarterly LTPO Smartphone Unit and Revenue Share, Q4’20-Q4’21

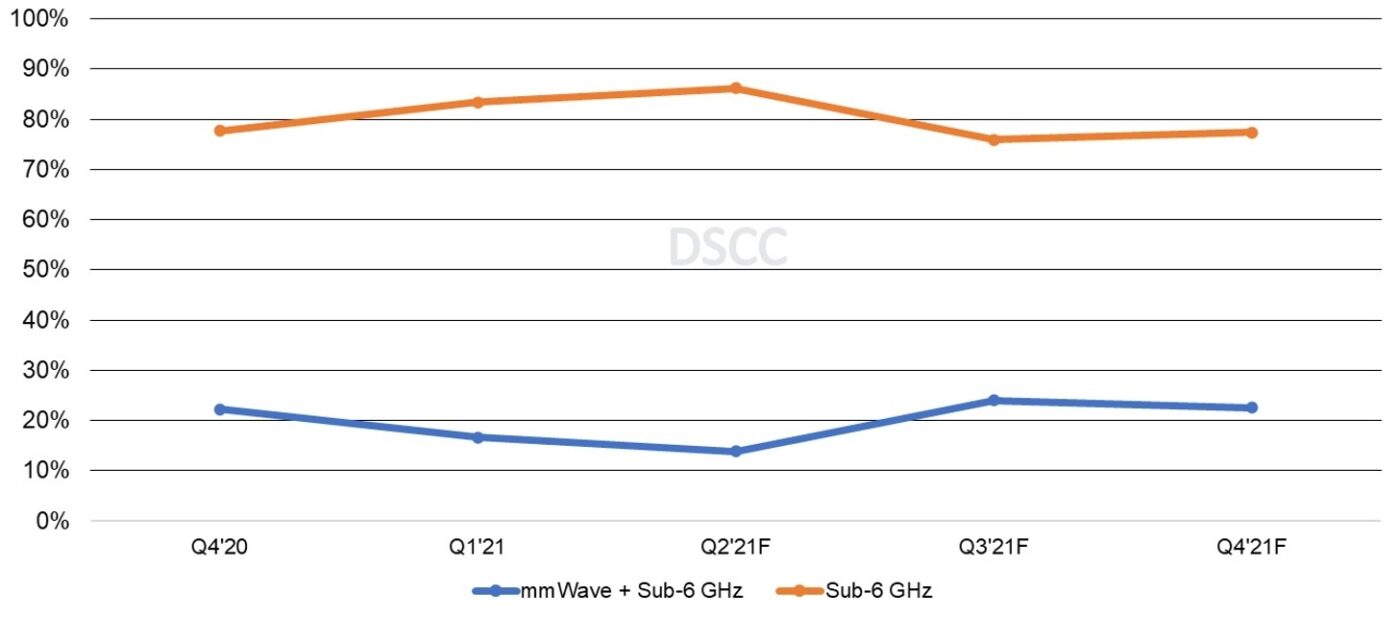

In addition to the increase in higher refresh rates and the use of LTPO backplanes, DSCC also sees significant growth in 5G. Most 5G smartphones were sub-6 GHz only due to the lack of 5G millimeter wave (mmWave) networks/coverage. mmWave functionality typically resulted in a $100 cost adder on some 5G phones. However, Apple outfitted all US iPhone 12 series products with mmWave + sub-6 GHz without a cost penalty, which is boosting investment in mmWave and its outlook. The US sees the most mmWave investment due to the lack of Sub-6 GHz bandwidth as much of the sub-6 GHz spectrum in the US is still owned and used by the government.

In Q1’21, mmWave + Sub-6 GHz declined 17% from 22% in Q4’20 as Apple’s iPhone 12 models lost share. While the iPhone 12 series was around 35% mmWave + Sub-6 GHz, the iPhone 13 series is expected to be closer to 55% mmWave + Sub-6 GHz as other regions roll out mmWave. Apple is also expected to roll out mmWave to Japan and Korea with the iPhone 13 series.

Quarterly 5G Network Band Unit Share, Q4’20-Q4’21

For the long-term forecast of 5G, AMOLEDs are expected to continue to lead the way in 5G due to their advantages in power, thickness and weight. 5G smartphones are expected to account for 67% of AMOLED demand in 2021, and 92% in 2022 and close to 97% by 2025, helped by a declining price gap between 4G and 5G components and continued network availability. In 2021, 5G demand is expected to grow by 68% to 418M, with 46% unit growth in 2022 to 690M and 10% unit growth in 2023 to 761M. 5G is expected to reach 930M units by 2025.

Annual Forecast Network Type Unit Share, 2021-2025

Other highlights of the latest report include:

- Smartphone panels are expected to rebound, rising 6% in 2021 and 8% in 2022 after falling 8% in 2020;

- AMOLED smartphone panel shipments are expected to rise 25% in 2021 to earn a 41% unit share. LCDs are expected to fall by 3% in 2021 to reach a 59% unit share;

- In Q1’21, smartphone panel shipments were down 15% Q/Q on normal seasonality and up 56% Y/Y. It was 7% higher than our forecast of 143M panels;

- As expected, flexible volumes lost unit share in Q1’21 to 51% share from 64% in Q4’20. In Q1’21, rigid and flexible volumes declined 15% Q/Q, and were up 56% Y/Y. Flexible volumes are expected to continue to fall 23% in Q2’21 before making a comeback in Q3’21 with 42% Q/Q and 39% Y/Y growth;

- Rigid OLEDs grew 17% Q/Q and 54% Y/Y to 77M panels. Rigid OLEDs are expected to maintain their volumes in 1H’21 on a 20% Q/Q unit decline and 19% Y/Y unit increase in Q2’21. This is due to continued gains from Honor, Huawei, Oppo, Vivo, Xiaomi and Samsung;

- In Q1’21, AMOLED smartphone panel revenues declined 27% Q/Q and was up 48% Y/Y to $7.8B;

- In Q1’21, AMOLED smartphone device revenues on a panel shipment timeline were down 24% Q/Q and up 47% Y/Y. ASPs were down 11% Q/Q and 6% Y/Y due to clearing out inventory of older models by brands. In Q2’21, revenues and units will decrease by 24% based on seasonality and in Q3’21, revenues will grow by 56% Q/Q and 48 Y/Y due to new product introductions;

- Rigid panel revenues were up 19% Q/Q and 40% Y/Y to $1.8B in Q1’21 and are expected to fall 15% Q/Q but up 12% Y/Y to $1.5B on seasonal weakness. In Q3’21, rigid OLED panel revenues are expected to increase 17% Q/Q and 23% Y/Y as a result of increased panel capacity from EDO and Visionox;

- Flexible revenues declined 34% Q/Q and was up 51% Y/Y to $6B in Q1’21. Revenues are expected to fall 30% Q/Q in Q2’21 on seasonal weakness but will be up 77% Q/Q and 52% Y/Y in Q3’21 due to new flexible OLED smartphone products from Apple and Samsung.

- Forecasts are provided out to 2025 for:

- AMOLED smartphones;

- Rigid AMOLED smartphones;

- Flexible AMOLED smartphones;

- Panel shipments, prices and revenues by size, resolution, refresh rate and backplane technology;

- Smartphone shipments, prices and revenues by size, resolution, refresh rate, network type (4G vs. 5G) and backplane (LTPO vs. LTPS) technology;

- Brand units and revenues;

- Display size, aspect ratio, resolution, PPI, touch sensor type, chipset, cover glass type, etc.;

- And much more.

Readers interested in subscribing to the DSCC Quarterly Advanced Smartphone Features Report (一部実データ付きサンプルをお送りします) should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced Smartphone Features Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご要請にて「国内販売価格」を24時間以内にご返信します。 2) 続いて、レポート最新号に基づく「商品サンプル」を作成の上、ご返信します。 3) さらに、ご希望されるお客様には、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 4) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。