国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 07/06/2021

OLED Panel Revenues Forecasted to Exceed $60B in 2025 Helped by Increased IT Market Penetration

David Naranjo, Senior DirectorSan Diego, CA USA -

[田村喜男の補足解説]

DSCCはOLEDメーカー世界各社の出荷データ及び対セットブランドとのサプライチェン動向を分析した Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) の最新号 (Q2'21版) を発刊した。そのパネル長期見通しでは、スマートフォンやTVに続くIT関連予測を引き上げた。ノートPC市場では、リジッドが2021年から500万パネル以上で本格的に立ち上がり、ハイエンド市場を侵食していく。タブレット市場では、Appleが2021年にMiniLED LCDモデルを投入したが、2023年からTFE (Thin Film Encapsulation: 薄膜封止) 型リジッドOLEDの採用を計画しており、以降需要増加が期待される。ノートPCもタブレットも、2023年以降にはフォルダブルの立ち上がりも期待される。いずれもトップのSDCをLGDやBOEなどが追随していく格好となる。モニター市場では、これまではインクジェットOLEDの特殊用途向けに限定されていたが、2022年からはLGDがWOLEDで42”/31”/27”などを投入していく。WOLED TV並みのインチコストをベースに、ゲーム用途などの大型モニター市場を開拓していくことが可能となる。以上、今後のOLED市場は従来のスマートフォンとTVの2本柱に加えて、IT用途を開拓していく流れとなる。

アジア代表・田村喜男 (7月8日 10:00版)

---------------------

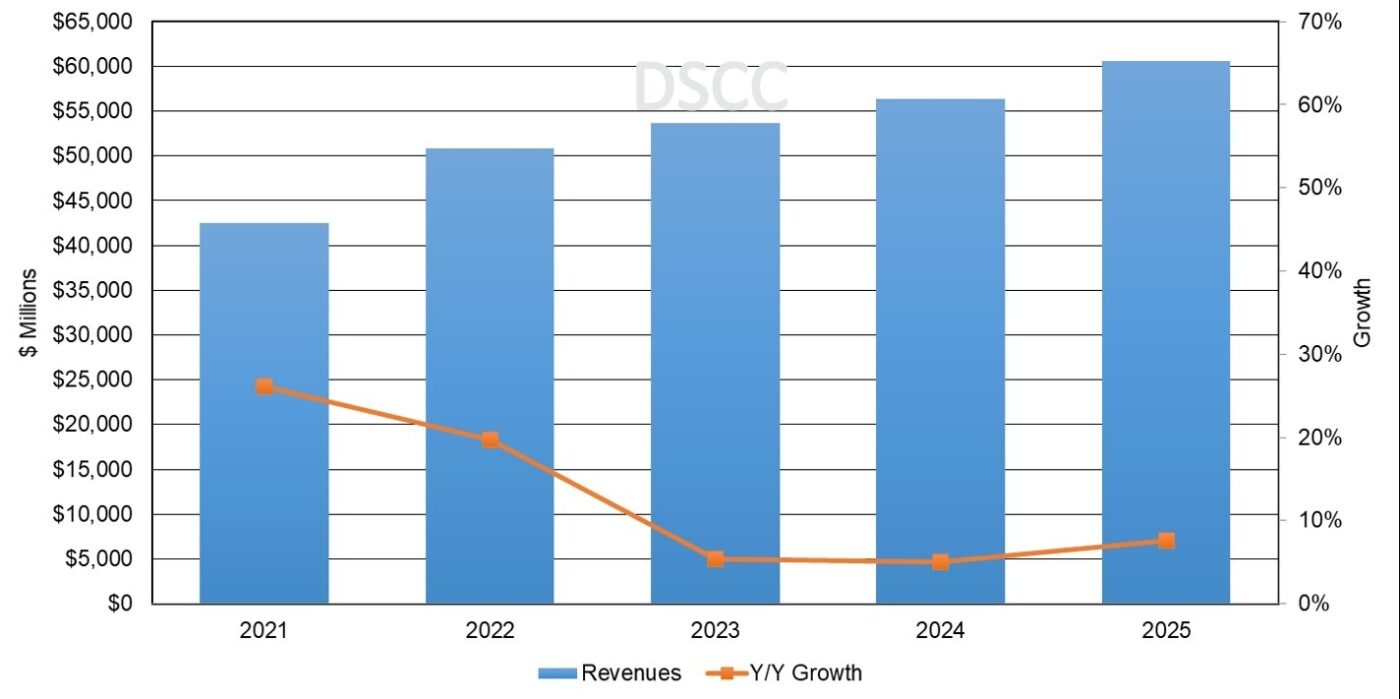

DSCC has upgraded both its near-term and long-term OLED forecasts. In its latest Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします), DSCC has raised its revenue outlook for 2021 by 9% to $42.5B on increased OLED smartphone volumes at higher prices helped by the driver IC shortages as well as higher OLED notebook volumes as Samsung Display has raised its OLED notebook PC panel target beyond 5M units.

Looking out to 2025, DSCC has raised its OLED revenue forecast by 11% to $60.6B helped again by higher volumes in smartphones as well as increased penetration into all three IT markets – tablets, notebook PCs and monitors. In tablets, Apple’s entry into the OLED tablet market expected in 2023 will boost the tablet market to over $1B in 2024. In notebook PCs, Samsung Display is expected to remain aggressive after 2021 resulting in over $1B in OLED panel revenues from 2023. In addition, both SDC and LGD will target the OLED monitor market with their TV panels through multi-model glass production with OLED monitor panels to exceed $500M in 2024. In total, DSCC has increased its OLED IT forecasts for 2022 -2025 by 40% for tablets, 13% for notebooks and 238% for monitors.

Annual AMOLED Panel Revenue Forecast, 2021-2025

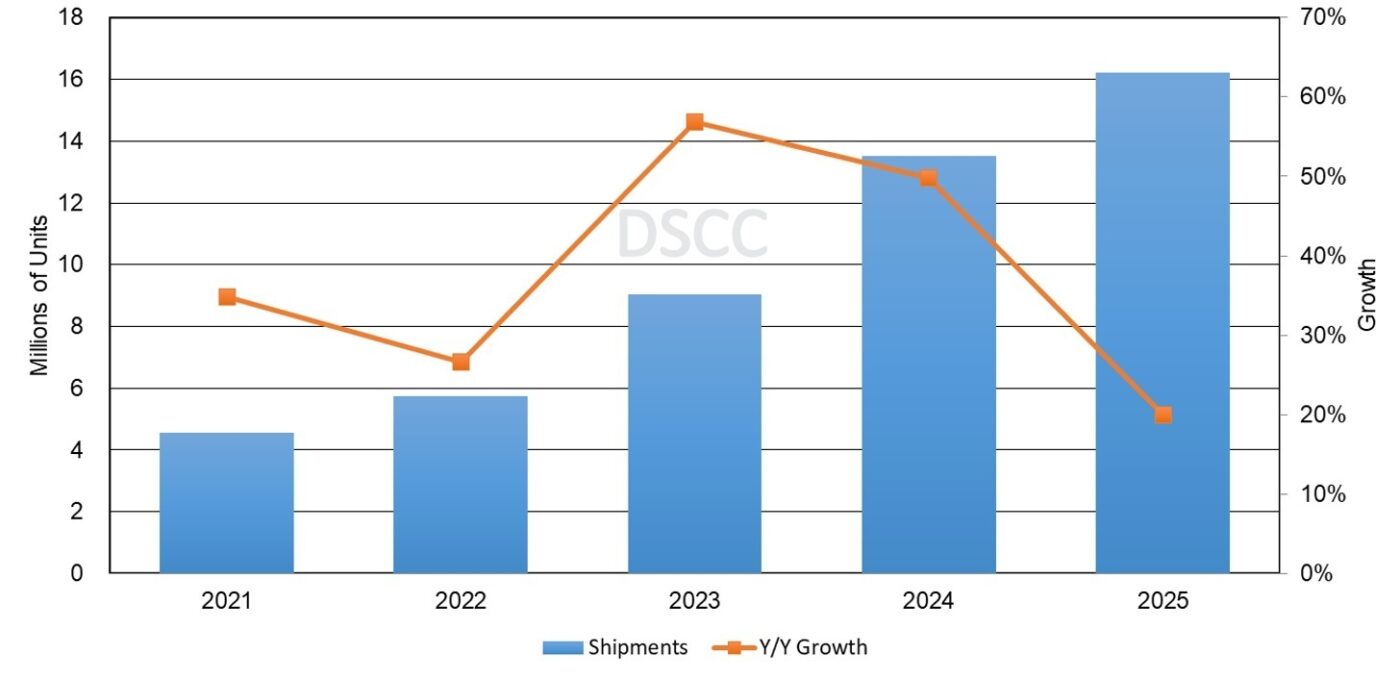

In 2022, for OLED tablets, we are forecasting 5.7M units, up from 5.4M units in the Q1’21 report, and $529M revenue, up from $447M in the Q1’21 report. Over the forecast period, we expect tablets to achieve 37% CAGR in units and 34% in revenue through 2025. OLED tablets will achieve 57% Y/Y revenue growth in 2023, its highest Y/Y growth during the forecast period.

Annual AMOLED Tablet Panel Shipment Forecast, 2021-2025

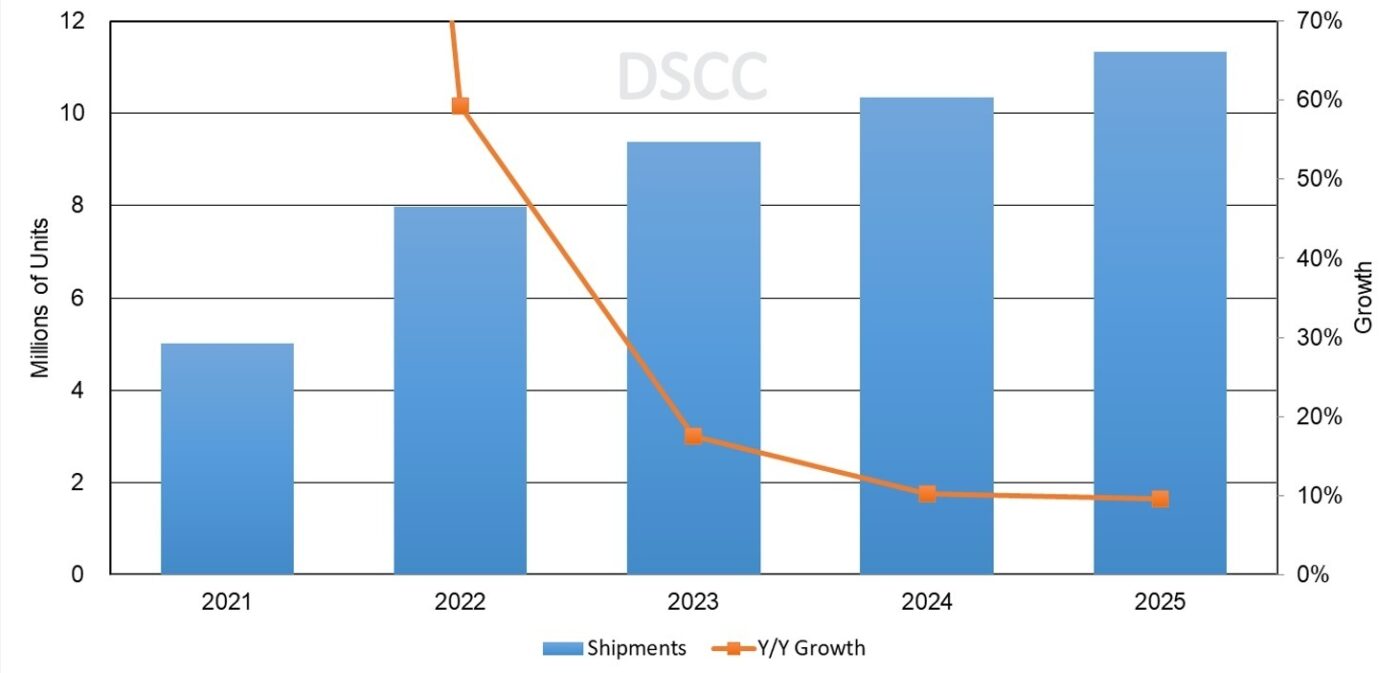

In 2023, for OLED notebooks, we are forecasting 9.4M units, up from 7.6M units in the Q1’21 report, and $1.1B revenue, up from $447M in the Q1’21 report. There are several brands already selling OLED notebooks. Those brands include Dell, Asus, HP, Lenovo, Razer and Samsung. Earlier this year, SDC announced plans to produce 90Hz OLED panels for notebooks and raised their 2021 target to 6M units. We expect SDC will remain aggressive in OLED notebooks to try and fend off the challenge from miniLEDs. Over the forecast period, notebooks will achieve a 23% CAGR in units and revenue through 2025. In units, notebooks will achieve 60% Y/Y growth in 2022, its highest Y/Y growth during the 2022-2025 forecast period. Despite the increase in rigid/flexible notebooks, we downgraded foldable notebooks due to the death of Windows 10X with brands expected to introduce their own software solutions for application continuity, etc.

Annual AMOLED Notebook Panel Shipment Forecast, 2021-2025

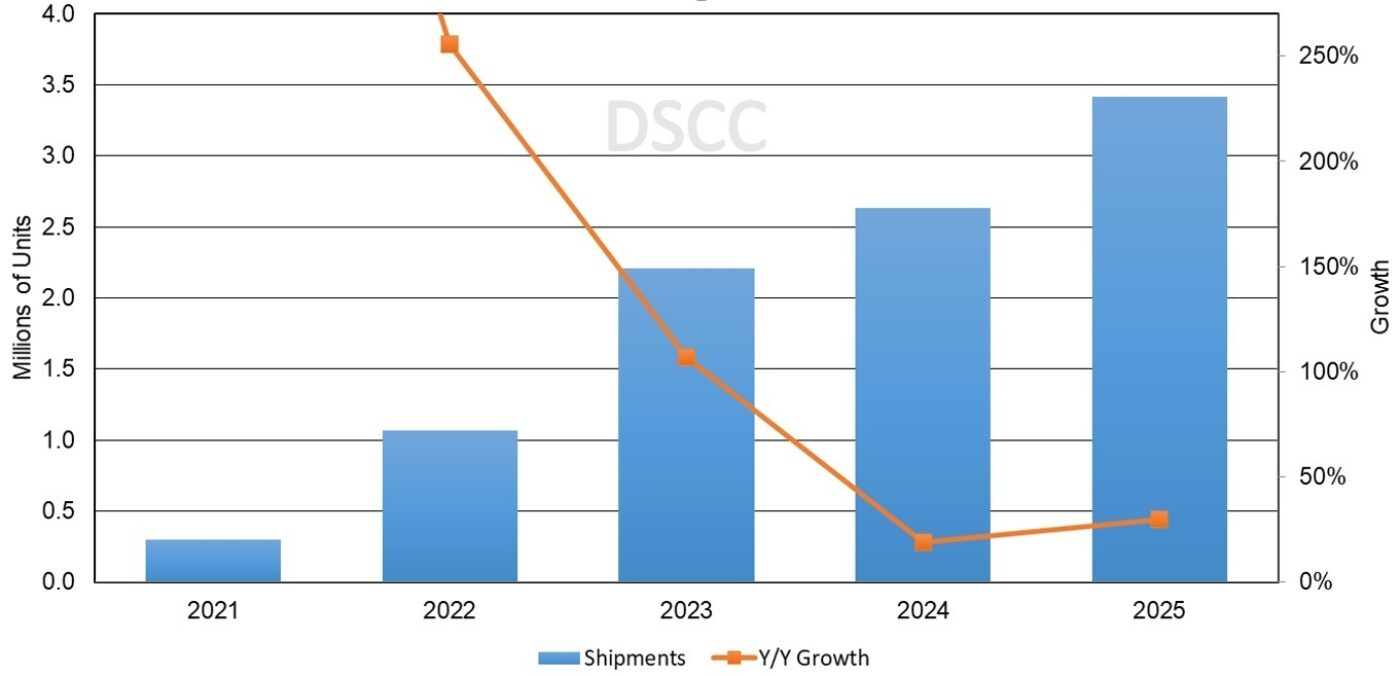

We have also updated the monitor forecast starting in 2022. SDC and LGD both have facilities that use MMG production. MMG production is an efficient way to either produce large panels or smaller panels from the same mother glass. For example, SDC may use the technology to produce 27” and 32” 8K gaming monitors. By adopting MMG technology, it will be able to produce two 82” and three 32” panels on the same G8.5 substrate, or two 78” and six 27” panels. Over the forecast period, monitors are forecasted to achieve 84% CAGR in units and 37% CAGR in revenue through 2025. In units, monitors will achieve 256% Y/Y growth in 2022, its highest Y/Y growth during the forecast period.

Annual AMOLED Monitor Panel Shipment Forecast, 2021-2025

The Q2’21 update of this report also provides quarterly updates by panel supplier, by application, by brand, by application for units, revenue and average selling price (ASP)

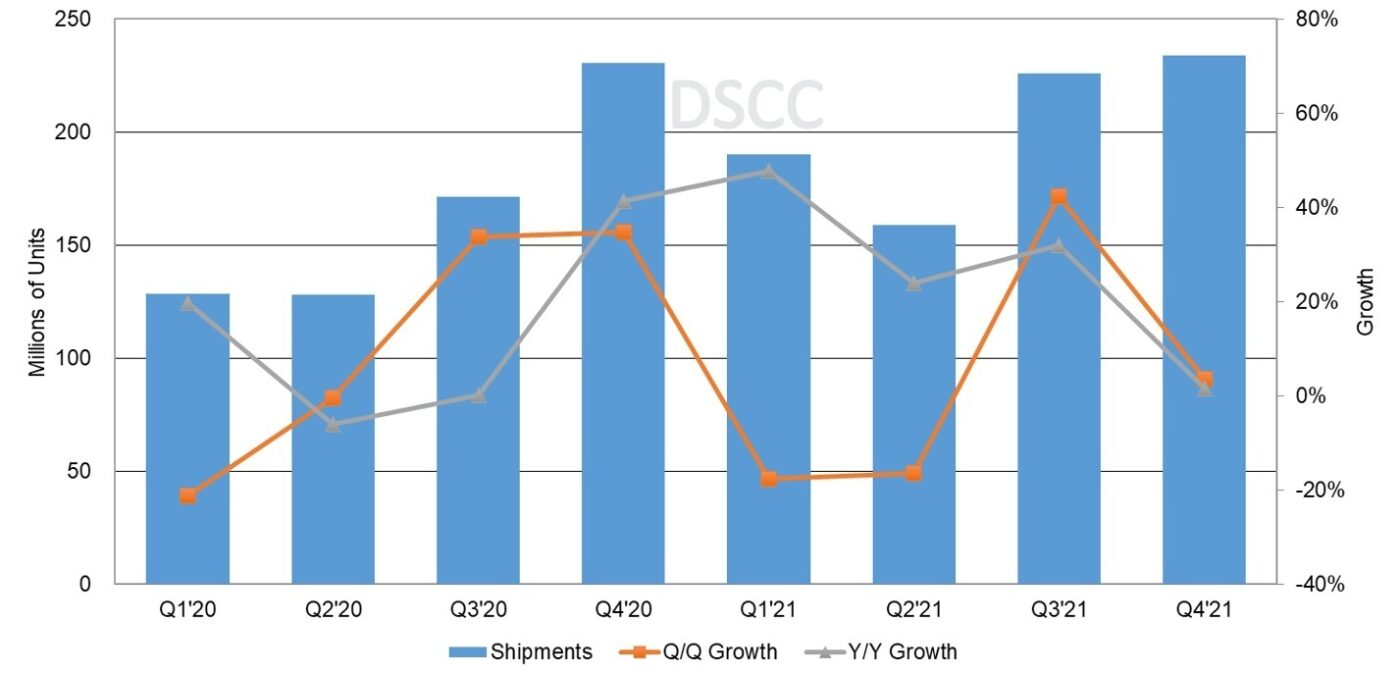

For mobile applications (excludes monitors and TVs), Q1’21 had shipment volume declines of 18% Q/Q but saw 48% Y/Y growth. We expect that Q2’21 will have a decrease of 16% Q/Q following normal seasonality, but Y/Y will see a 24% unit growth. Q3’21 is expected to increase Q/Q and will continue with double digit Y/Y growth.

Quarterly Mobile OLED Unit Shipment & Growth, Q1’20-Q4’21

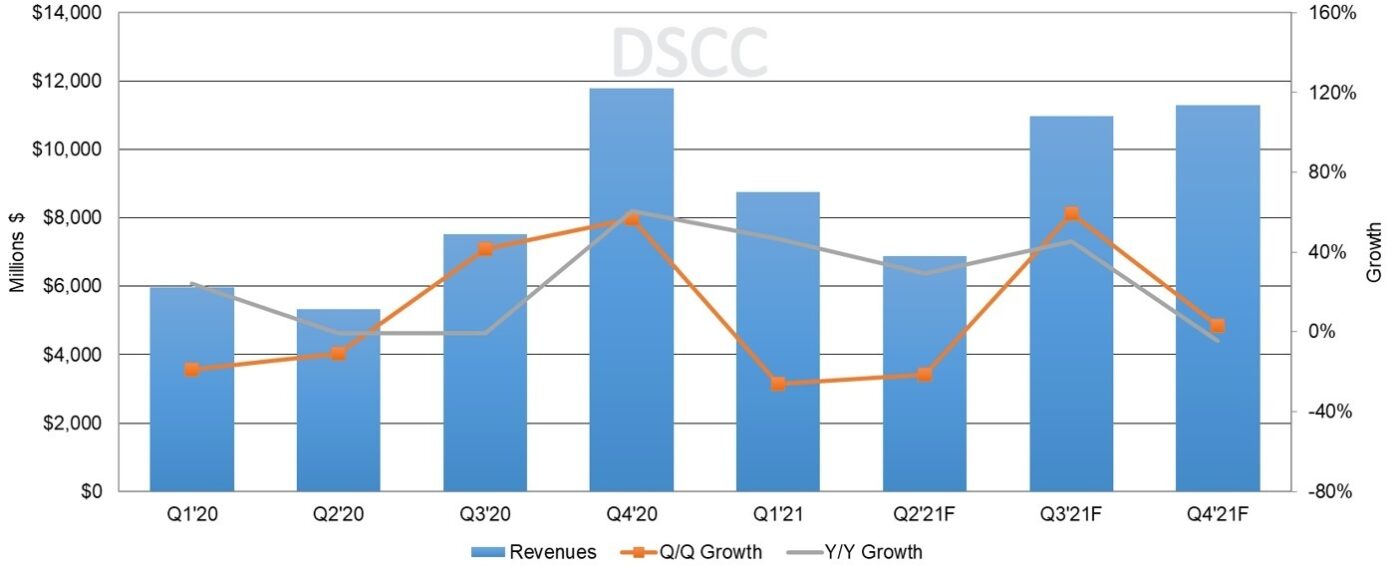

In terms of revenue, Q1’21 OLED revenues declined by 26% Q/Q and were up 47% Y/Y to $8.76B.

We expect Q2’21 to decrease 21% Q/Q but increase 30% Y/Y to $6.89B. We expect Q3’21 to grow significantly Q/Q and Y/Y but Q4’21 will show a 4% Y/Y revenue decrease with an earlier iPhone 12s series launch versus Q4’20 and as revenues are pulled forward to Q3.

Quarterly Mobile OLED Revenues & Growth, Q1’20-Q4’21

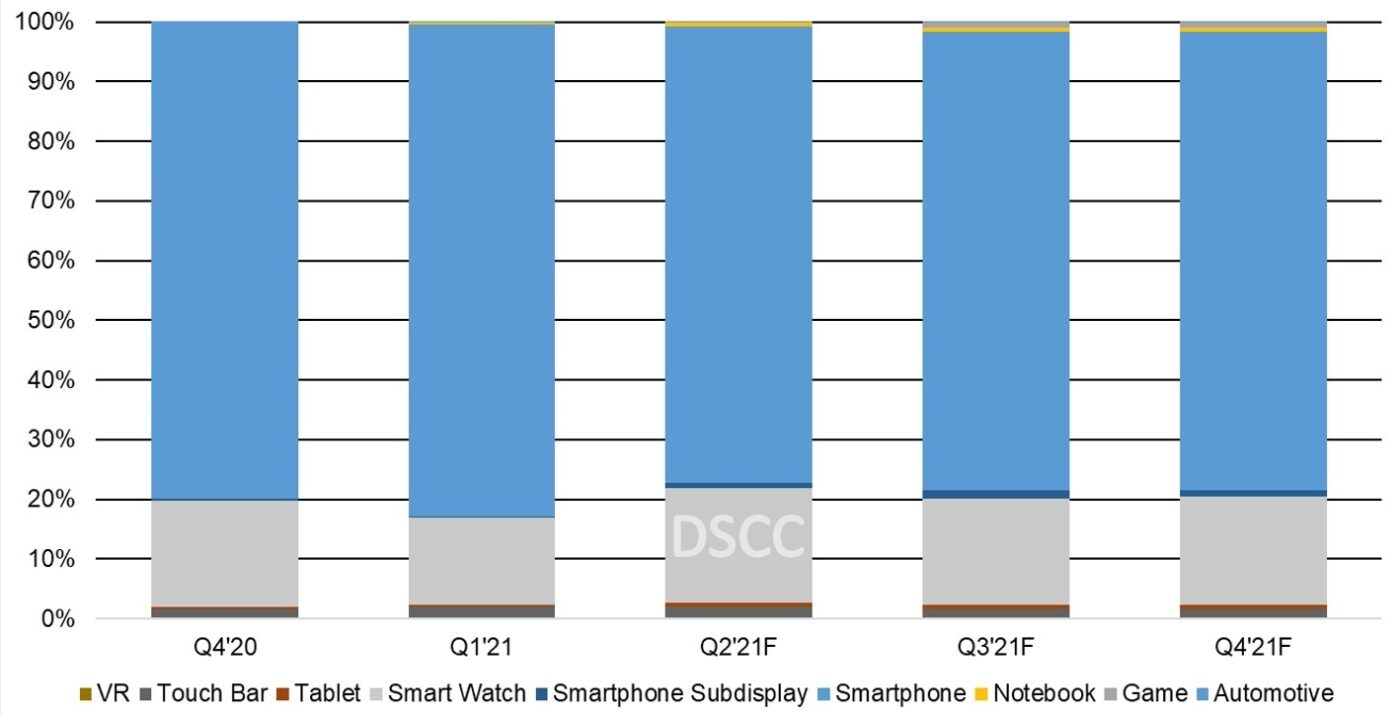

By mobile application, smartphones continue to dominate OLED volumes with an 82% share in Q1’21 and 76% share in Q2’21. In Q1’21, Apple had a 26% share of OLED smartphone shipments, followed by Samsung with a 20% share.

On a revenue basis, smartphones account for 91% share in Q1’21 and 87% share in Q2’21. Smartwatches remained the #2 application with a share of 14.9% in units and 6% in revenue for Q1’21. We expect to see an increase of 19.5% in units and 7.8% in revenue in Q2’21.

Touch Bars continue to be the #3 application with a 18% unit share and 1.2% revenue share in Q1’21. We expect Touch Bars to be exceeded by tablets when Apple starts the adoption of the 10.9” AMOLED iPad. Further, our sources suggest that Apple may cancel the Touch Bar in the future.

Quarterly Mobile OLED Shipments by Application, Q4’20-Q4’21

By smartphone panel supplier, SDC continued to lead with a unit share of 75.2% in Q1’21 up from 74.5% in Q4’20. LGD was the #2 supplier with an 8% unit share, down from 11% in Q4’20, followed by BOE with 6.6% unit share, down from 7.0% in Q4’20. In Q1’21, Tianma shipments increased by 55% to a 1.7% shipment unit share. EDO’s share increased by >200% rising from 0.8% in Q4’20 to 2.8% in Q1’21 due to an increase in rigid OLED capacity and design wins for products such as the new Honor Play5 5G smartphone.

On a revenue basis, In Q1’21, SDC had 73.7% revenue share followed by BOE which had a revenue share increase of 8.7% from 7.7% share in Q4’20 to 8.7% share in Q1’21 due to various design wins. LGD maintain the #2 position in Q1’21 with 10.6% revenue share down from 11.9% in Q4’20. Although EDO’s unit share skyrocketed by 200% in Q1’21, their revenue share increased by only 27% to 1.4% share due to the competitive nature of rigid OLEDs and their design win of the new Honor Play5 5G smartphone.

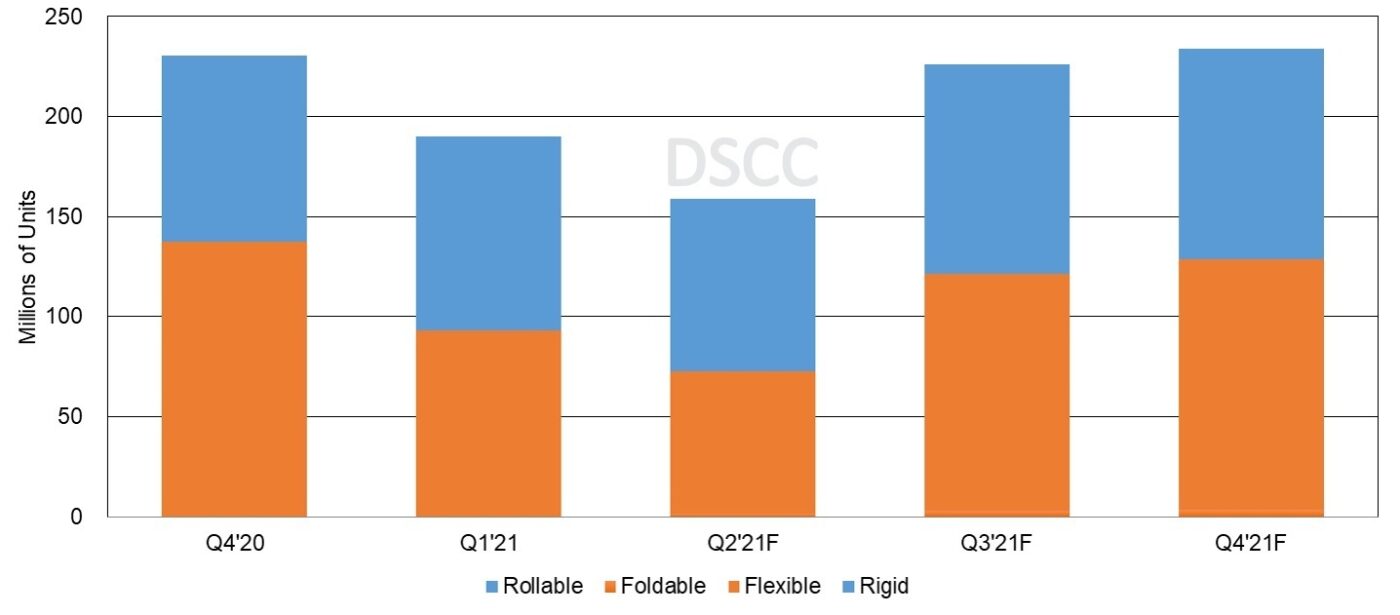

By form factor, rigid OLED accounted for 51% of shipments for mobile applications, followed by flexible OLED at 48.5% in Q1’21. We expect flexible OLED to take >50% unit share in Q3’21 due to surplus flexible capacity at Chinese panel suppliers as they are expected to offer lower pricing to other brands. Foldable will increase to a 1.4% unit share in Q3’21, as a result of new foldable launches from SDC, Xiaomi, Oppo and Vivo.

For rigid OLEDs for mobile applications in 2021, we expect Samsung to account for 23% unit share followed by Xiaomi with 16% unit share.

For flexible OLEDs for mobile applications in 2021, we expect Apple to account for 53% unit share followed by Samsung with 19% unit share. For foldable OLEDs for mobile applications in 2021, we expect Samsung to have the lion’s share at 77% unit share followed by Huawei with 7% unit share and Xiaomi with a 6% unit share.

Quarterly Mobile OLED Shipments by Form Factor, Q4’20-Q4’21

The report also provides roadmaps for all major smartphone brands revealing display sizes, resolution, refresh rate, cover glass type and panel supplier for 16 future smartphones and eight foldable smartphones including the S22 among others.

Readers interested in subscribing to the DSCC’s Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) should contact gerry@displaysupplychain.com.

本記事の出典調査レポート

Quarterly OLED Shipment Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご要請にて「国内販売価格」を24時間以内にご返信します。 2) 続いて、レポート最新号に基づく「商品サンプル」を作成の上、ご返信します。 3) さらに、ご希望されるお客様には、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 4) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。