国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 04/21/2021

OLED Revenues Expected to Increase 36% Y/Y in 1H 2021

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

[田村喜男の補足解説] OLED需要が非常に力強い。当社の最新調査レポートによると、2021年のOLED出荷面積は前年比40%増もの見通しとなった。OLED市場はスマートフォンとTVが2台アプリケーションとなっており、両者とも2020年後半から成長速度が加速してきた。2021年上半期は季節要因により2020年下半期より微減となっているが、前年同期比では+70%もの増加が見込まれる。スマートフォン用OLEDは、リジッドとフレキシブルに大別される。フレキシブルOLED市場は、Apple iPhoneの2020年秋モデルでのフレキシブルOLED全モデル採用により、2020年下期に需要が急増した。Honor、Xiaomi、Oppo、Vivoなど中国ブランド向けフレキシブルOLED需要も増加してきている。リジッドOLEDもこれら中国メーカー向けで需要が増加、SDCのA2ラインの稼働率が90%以上まで回復している。TV用OLEDは、LGD中国広州工場の量産開始により、2020年下半期からパネル出荷量が急増した。供給増加に対応して、パネルサイズのラインナップも拡張している。主要55/65/77インチサイズに加えて48インチを追加して大きく増産、さらに83インチも追加されている。2021年下半期には42インチも量産開始する見込みである。また、Samsung VDのWOLED TVパネル採用の可能性が大きな話題となってきている。(4月23日12:50 DSCC アジア代表・田村喜男)

------------

OLED panel revenues will increase by 36% Y/Y in the first half of 2021, according to the latest update of the DSCC Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします), as increased panel shipments for smartphones are combined with revenue growth in TVs, smartwatches and other applications.

The Q1 update of this report gives actual shipments for Q4 2020 and DSCC’s estimates for Q1 and Q2 2021, plus DSCC’s forecast for 2021 to 2025 for eleven different applications for OLED panels, with detailed figures for units, revenue, area, Average Selling Price (ASP), and other parameters with splits by application, panel supplier, substrate (rigid/flexible/foldable/rollable) and brand. The report also provides a quarterly forecast for 2021 with the same detail. In this article, we will cover DSCC’s estimated results through the first half of 2021, and a separate article on DSCC’s OLED Supply/Demand report will cover the long-term forecast. Subscribers to the report, of course, can see all the results in the Excel file.

Like many other things in the electronics industry, the Q4 2020 and Q1 2021 numbers have been affected by the timing of Apple’s iPhone 12 model releases. The later release dates of 2020 accelerated sales in Q4 and pushed some sales into Q1 2021 as capacity was unable to meet demand in the fourth quarter. OLED panel revenues in Q4 2020 totaled $11.9B, up 46% Y/Y, and revenues for the full year 2020 increased 20% Y/Y to $33.2B. Our estimate for Q1 2021 shows revenues at $9.1B, up 38% compared to Q1 2020, and we expect Q2 2021 revenues of $7.5B, up 34% from the prior year.

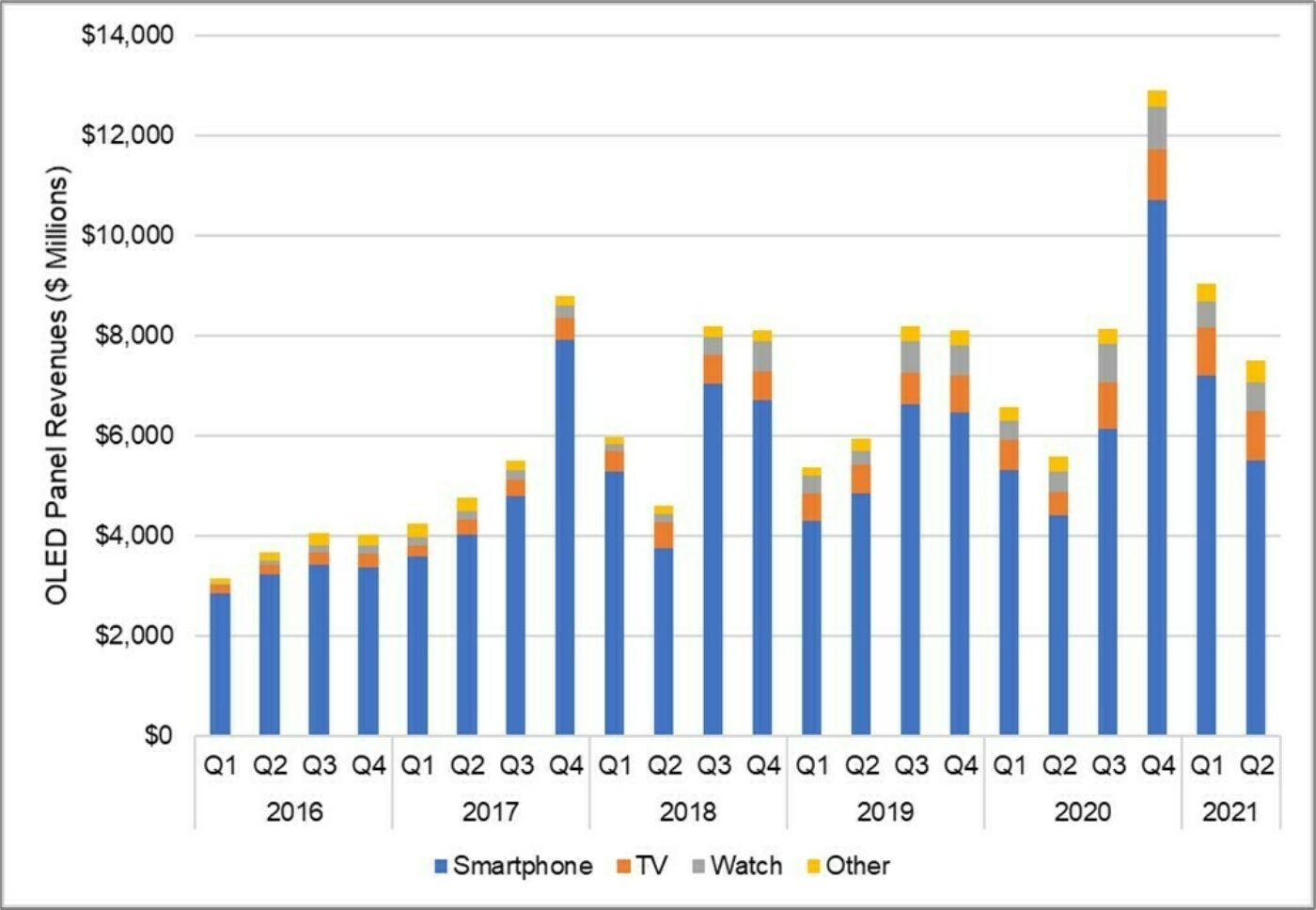

The pattern of OLED panel revenues is heavily weighted by smartphones, by far the largest application by revenues for OLED technology, as shown in the next chart. OLED panel revenues increased across all applications: we estimate that OLED smartphone revenues will rise 36% Y/Y in Q1 2021, while OLED TV panel revenues will grow 55% Y/Y, smartwatch panel revenues will increase 35% Y/Y and the revenues for all other applications will expand 40% Y/Y.

Quarterly OLED Panel Revenues by Application, 2016-2021

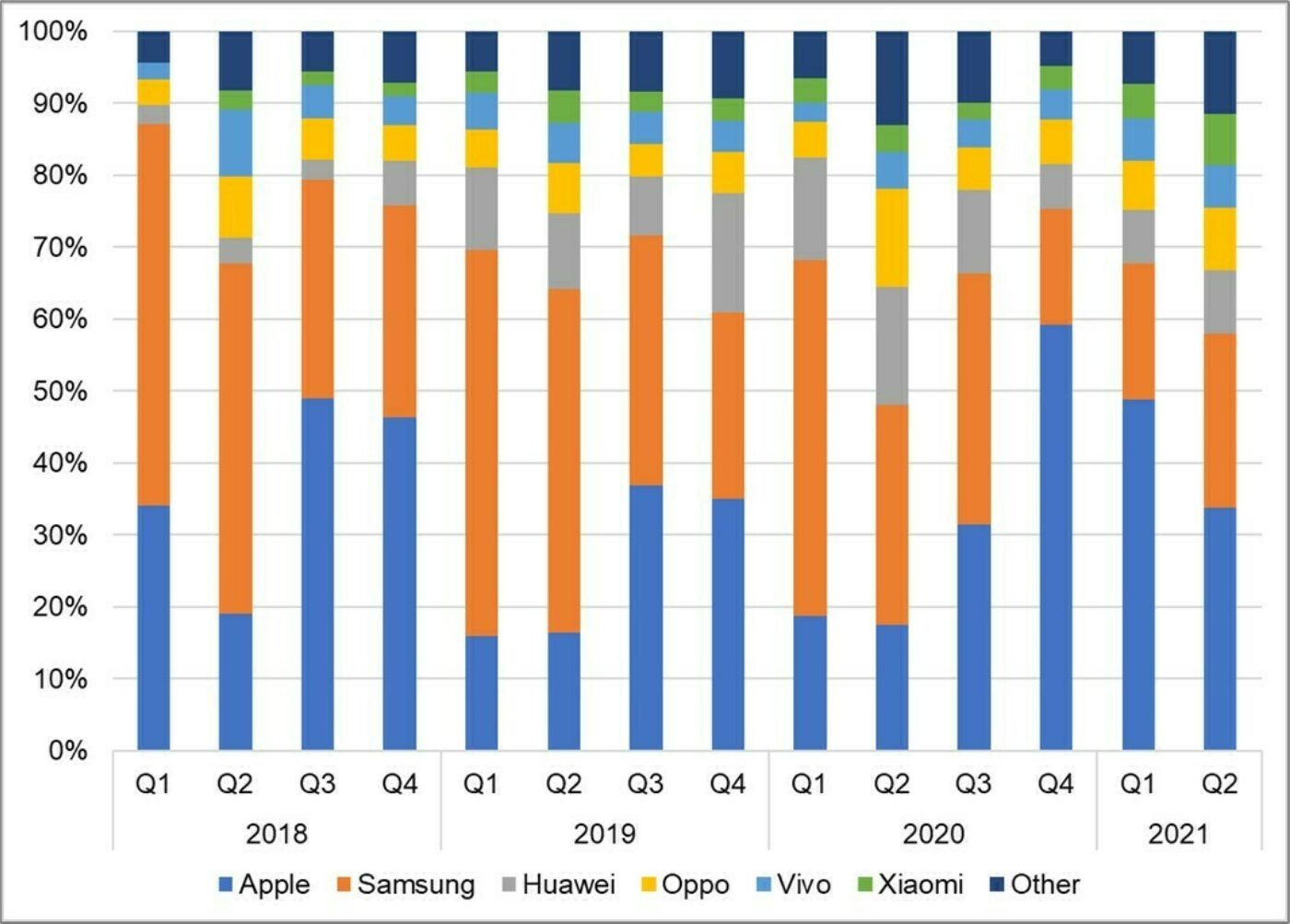

Within the smartphone category, the report allows an analysis of brand trends with detail to the model level on major smartphone brands. The influence of Apple can be seen by the next chart on smartphone panel revenue share by brand. Since it first introduced OLED panels into iPhones in 2017, Apple has shown a persistent seasonal pattern of a weak first half and a strong second half. But the delayed launch of iPhone 12 meant that Apple continued to dominate OLED smartphone panel revenues in Q1 2021. The strength of the iPhone 12 product line means that we expect Apple to maintain the leading revenue share in Q2 2021.

Quarterly OLED Smartphone Panel Revenue Share by Brand, 2018-2021

DSCC estimates that OLED panel unit shipments across all applications will increase 41% Y/Y in Q1 2021 to 181M, driven mostly by increases in smartphone and smartwatch units. OLED smartphone panel shipments are estimated to be up 45% Y/Y to 143M, while OLED smartwatch shipments are estimated to increase by 28% to 29M. We estimate that growth in OLED TV units will be even more impressive in unit terms, increasing 89% Y/Y to 1.6M, and this will accelerate further with 133% Y/Y growth in Q2 2021.

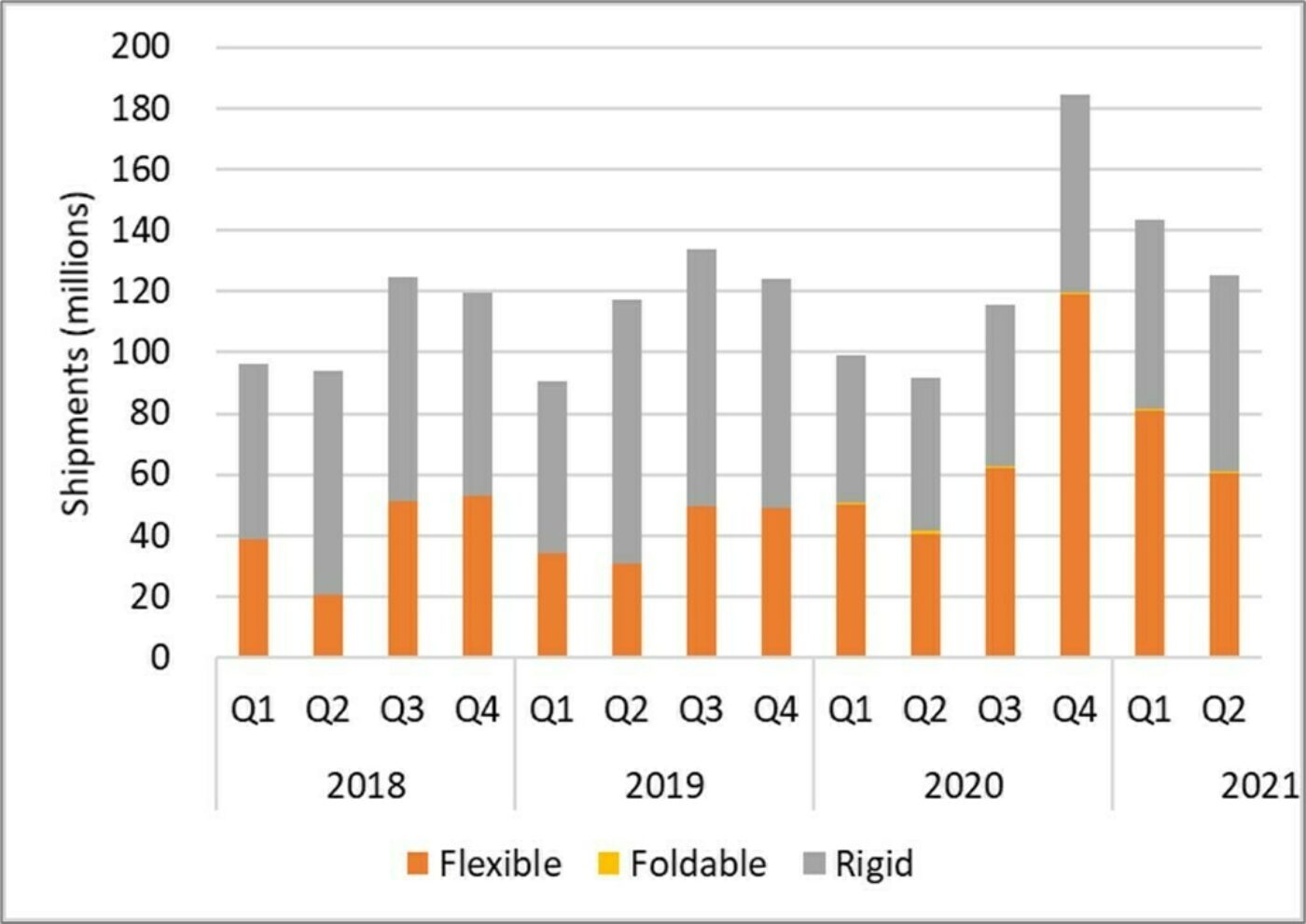

The report includes segmentation by substrate type, as shown in the next chart. While rigid OLED panels were the majority of smartphone shipments through 2019, flexible OLED panels surpassed rigid panels in 2020 and continue to outnumber rigid panels in Q1 2021. Flexible OLED panels represented an estimated 62% of all OLED smartphone panels, with rigid panels at 37% and foldable panels at less than 1%. Our report includes a forecast for rollable OLED panels, and we will start tracking that substrate configuration when the shipments start.

Quarterly OLED Panel Shipments by Substrate, 2018-2021

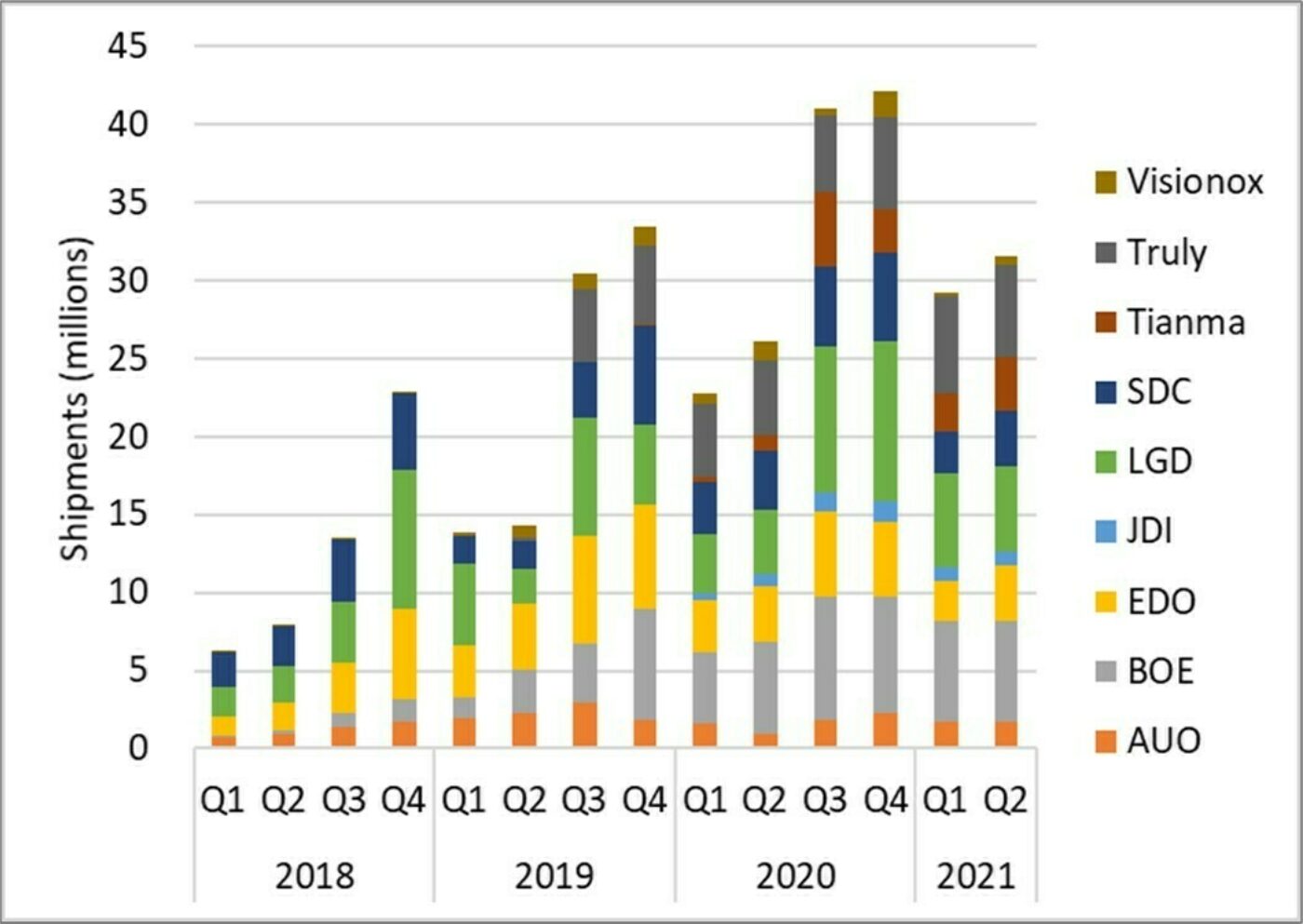

The report allows a comparison of shipments by panel maker. While OLED smartphone shipments continue to be dominated by Samsung, and OLED TV shipments remain a monopoly for LGD, there is healthy competition among many panel makers in the growing smartwatch segment, as shown in the next chart. LGD captured a leading share in 2020 with strong shipments to Apple for the Apple Watch, but we estimate that BOE narrowly outpaced LGD and Truly in Q1 2021 for the #1 spot. All three of those panel makers – BOE, LGD and Truly – are estimated to have captured more than 20% of the smartwatch market in Q1 2021.

Quarterly OLED Smartwatch Panel Shipments by Brand, 2018-2021

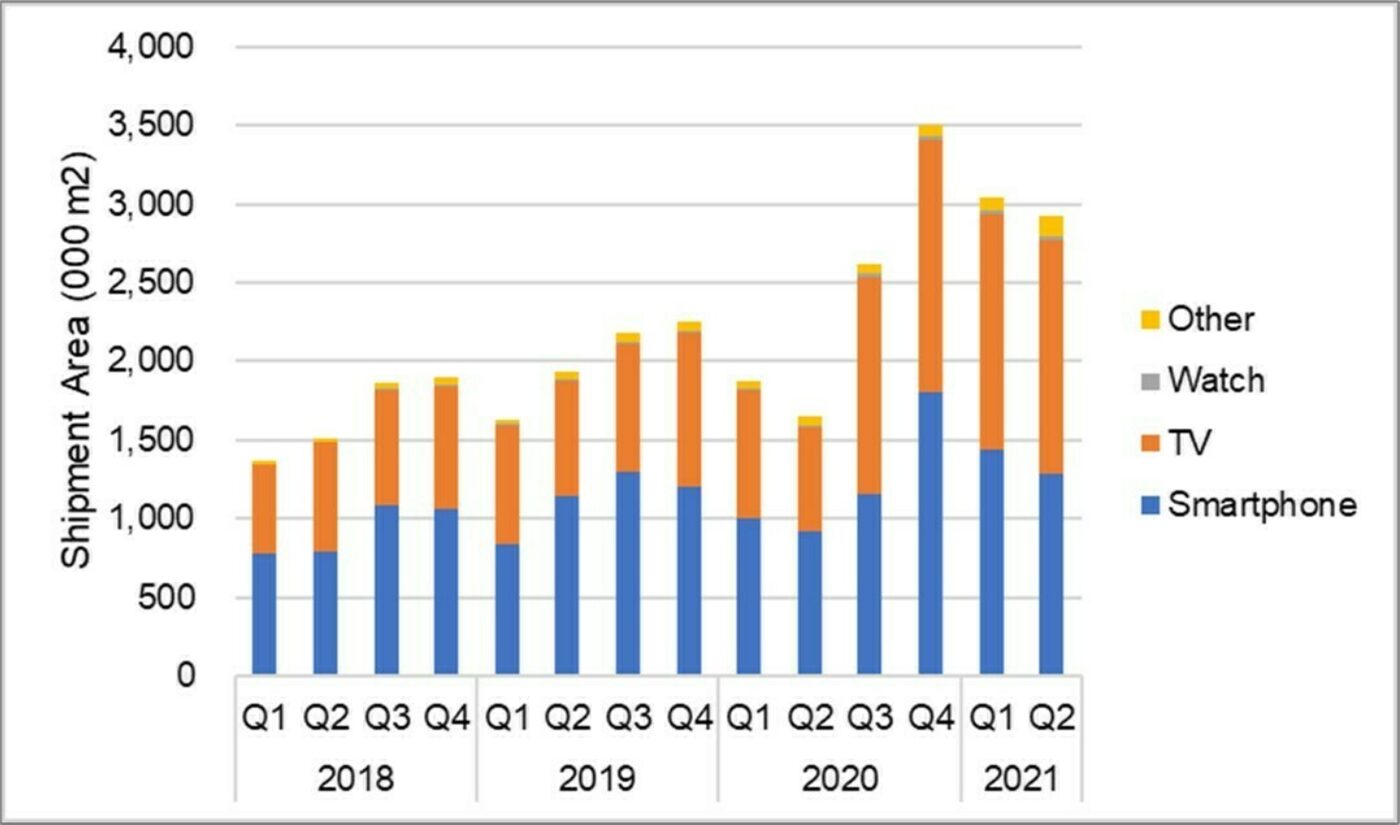

In area terms, TV surpassed smartphone for the first time ever in Q3 2020, and although smartphone surged past TV in Q4, we estimate that TV area will again reclaim the lead in Q1 2021, as shown in the following chart. OLED shipment area across all applications is expected to increase by an estimated 63% Y/Y in Q1 2021 to 3.0M square meters. OLED TV panel shipment should increase by 85% Y/Y in Q1 2021 to 1.5M square meters to account for 49% of all OLED panel area, while OLED smartphone panel shipment area will increase 44% to 1.4M square meters.

Quarterly OLED Area Shipments by Application, 2018-2021

As noted above, the DSCC Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) provides a comprehensive listing of historical panels shipments for all applications, plus a forecast of units, ASPs, screen sizes, resolutions, panel suppliers, and revenues for each application. Readers interested in subscribing to the DSCC Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) should contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。