国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 04/12/2021

DSCC Smartphone Report Reveals and Predicts Latest Smartphone Trends – High Refresh Rate Penetration Surging

Ross Young, Founder and CEOAustin, TX USA -

DSCC’s Quarterly Advanced Smartphone Features Report tracks and forecasts all major product trends in the AMOLED smartphone market in addition to providing supply chain insights for panels and chipsets.

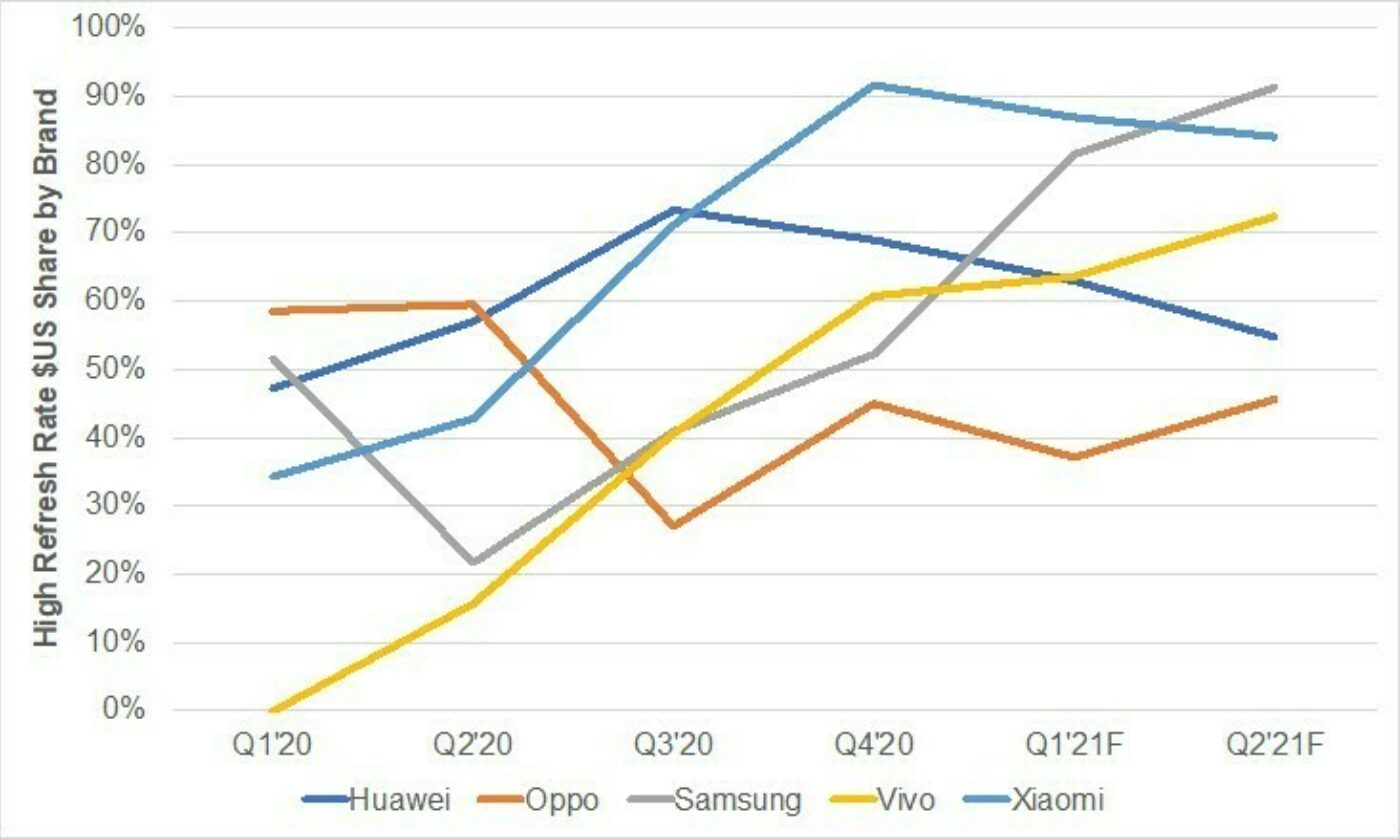

One of the major trends identified in the report is the rapid adoption of higher refresh rates, 90Hz and higher. This report tracks all AMOLED smartphone shipments by model and sees a significant uptick in higher refresh rates for most brands. In fact, in Q2’21, higher refresh rates should reach a 46% share of panel procurement on a unit basis and a 50% share on a smartphone revenue basis, up from 20% and 31% respectively in Q2’20. In Q2’21, 92% of Samsung’s AMOLED smartphone revenues are expected from high refresh smartphones, up from just 22% in Q2’20. Xiaomi is expected to see its high refresh rate AMOLED smartphones account for 84% of its Q2’21 revenues, up from 43%. Vivo follows a similar trend with Huawei declining due to its challenges. Apple and Oppo are the two major brands seeing less than a 50% share of revenues from high refresh rates. However, with Apple expected to launch LTPO smartphones in the 12s Pro and Pro Max, its high refresh rate will also surge.

High Refresh Rate Revenue Penetration for Top Brands

The high refresh rate smartphone market is surging for a few reasons.

- First, it improves display performance when scrolling or gaming and users are increasingly playing games on their smartphones. So, there is strong demand pull;

- Second, it is a relatively low-cost way to differentiate a smartphone and command a premium. 90Hz only adds a couple of dollars versus 60Hz and 120Hz on LTPS backplanes only adds a few more versus 90Hz;

- Third, with driver ICs in shortage and panel prices rising, driver IC suppliers, panel suppliers and smartphone brands are all prioritizing higher end, higher margin products which favors high refresh rate devices;

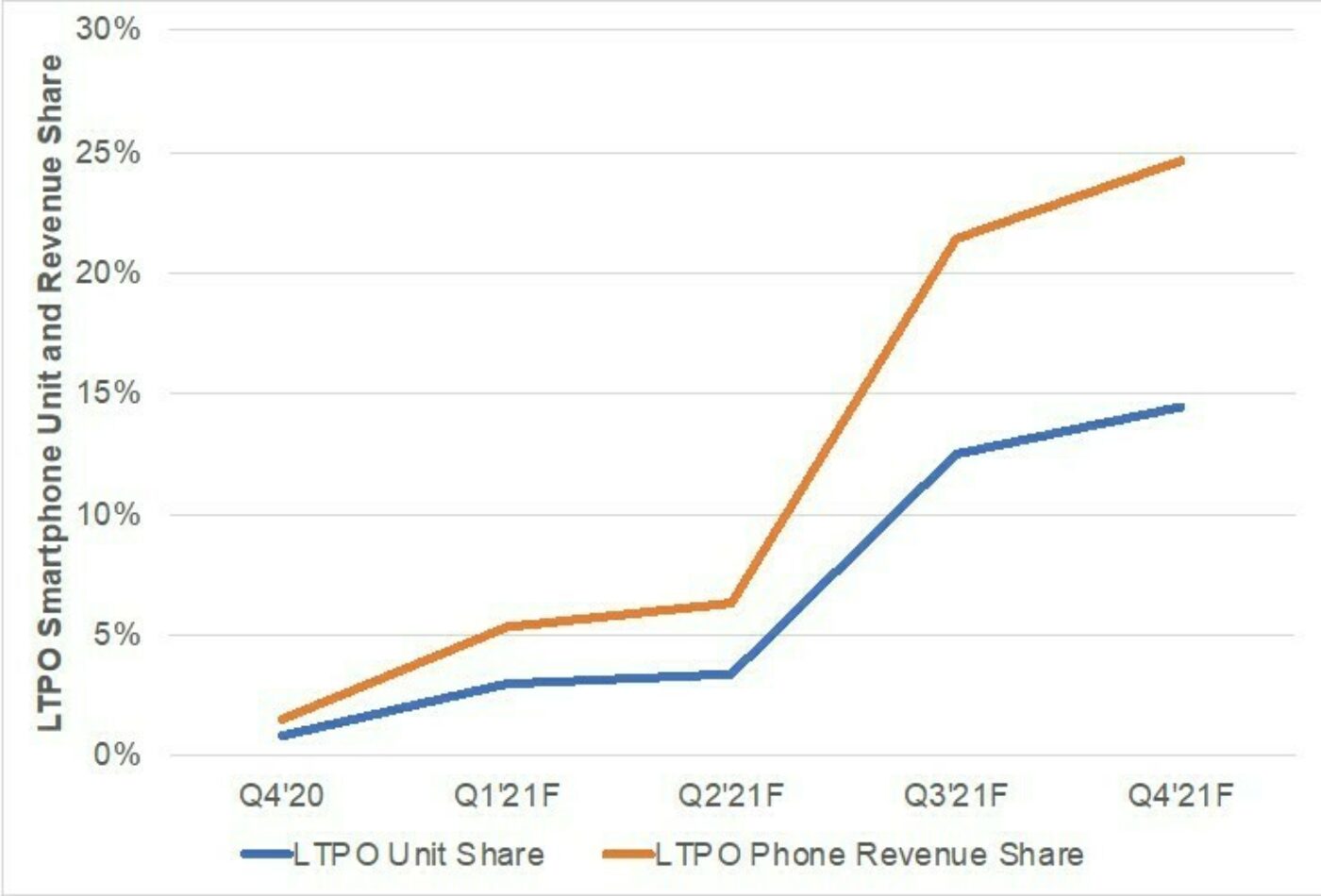

- Fourth, with Low Temperature Polysilicon (LTPO) capacity surging which offsets the higher power consumption from high refresh rates with the ability to operate at lower refresh rates depending on the content and reduce power consumption, more smartphone brands are looking to integrate LTPO AMOLEDs. Refresh rates in LTPO devices can vary from as low as 1Hz to 120Hz with overall power consumption declining 15% to 20%. While only six different LTPO smartphones have been introduced so far, this number will surge over the next 12 months. With LTPO displays and smartphones also selling at a premium, they too will be prioritized during the semiconductor shortage. DSCC believes LTPO displays are warranting a double-digit increase in $US today. DSCC expects LTPO smartphones to reach a 14% unit share and 25% smartphone revenue share by Q4’21 fueled by Apple launching LTPO on its 12s Pro and 12s Pro Max and other flagship phones also adopting LTPO. The report also reveals the latest LTPO fab schedules by panel manufacturer.

LTPO Smartphone Unit and Revenue Share

Other highlights of the latest report include:

- Smartphone panels are expected to rebound rising 7% in 2021 after falling 8% in 2020;

- AMOLED smartphone panel shipments grew 5% in 2020 to earn a 34% share and are expected to rise 27% in 2021 to earn a 40% share. LCDs fell 14% in 2020 and are expected to fall 4% in 2021 to reach a 60% share.

- Q4’20 was a record quarter as expected for AMOLED smartphone panels, up 61% Q/Q and 49% Y/Y to 184M. It was 37% higher than any other quarter. The strong quarter can be attributed to:

- Apple’s all OLED launch, much of which was delayed into Q4;

- A stronger launch for Apple than usual due to 5G;

- Samsung pulling in its S21 launch by one month with panel shipments starting a month earlier in Q4;

- 5G momentum, mostly outside of the US;

- Pent-up demand after a weak Q2 and Q3 with some economies recovering.

- Flexible AMOLED volumes surged in Q4’20 rising 92% Q/Q and 144% Y/Y to a record 119M panels on the delayed iPhone 12 launch and pulled in S21 launch. Q4’20 represented 44% of total 2020 flexible smartphone panel shipments;

- Flexible smartphone revenues have exceeded rigid since Q3’19 and accounted for a record 80% share of AMOLED smartphone revenues in Q4’20, up 91% Q/Q and 119% Y/Y to $104B;

- Q1’21 AMOLED smartphone panel procurement is expected to be down 22% Q/Q but still up 45% Y/Y at 143M panels. This represents the second-best quarter ever for AMOLED smartphone panels. Apple is expected to again drive the growth up over 300% on the delayed iPhone 12 launch. We also see triple digit Y/Y growth at Honor, Oppo and Vivo as they take share from Huawei;

- Q2’21 is expected to be down another 12% Q/Q while rising 38% Y/Y to 125M panels, the fourth best quarter. Once again, Apple’s volumes should be up over 100% along with Honor and Xiaomi;

- AMOLED smartphone panel area grew 58% Q/Q and 50% Y/Y in Q4’20 to 1.8M square meters. Despite a predicted double-digit drop in both Q1’21 and Q2’21 on seasonal weakness, area growth will still be up at least 40% Y/Y on beneficial comparables due to COVID-19 shutdowns in 1H’20 and positive 5G and Apple iPhone 12 momentum;

- Flexible smartphones widened their advantage over rigid on an area basis to 64% to 36% in Q4’20. That advantage is expected to decline to 12% in Q1’21 and a 4% deficit in Q2’21 as lower priced rigid OLED smartphones from Samsung and Chinese brands take share;

- Apple ended Samsung’s long-running reign on top of the AMOLED brand share charts in Q4’20 with a 41% unit share on 75M panels procured, up from an 18.5% share in Q3’20 and 17.5% in Q4’19. Boosting its share was the delayed launch of the Pro/Pro Max from Q3’20 to Q4’20 and the inclusion of 5G where there was pent-up demand. Apple is expected to continue to lead in Q1’21 with a 30% share on 43M panels procured. It is expected to lose its top position in Q2’21 as Samsung regains leadership.;

- Apple also led on a revenue basis in Q4’20 with an even higher share of 52.6%, the highest share for any brand since Samsung’s 53.1% share in Q1’19. Apple is also expected to lead in Q1’21 and Q2’21 on its higher blended ASPs versus Samsung helped by using only higher priced flexible AMOLEDs;

- While Apple uses only flexible AMOLEDs, other companies rely significantly more on lower priced rigid OLEDs. In Q4’20, only 34% of Samsung’s AMOLED panel procurement was flexible with Oppo and Vivo below that figure;

- On a unit basis, the iPhone 12 Series accounted for the top four models due to their delayed launch into Q4. Samsung led with seven models in the top 20, Oppo joined Apple with four models in the top 20 followed by Huawei and Xiaomi with two each and Vivo with one. Of the top 20 models, 12 models used flexible OLEDs, same as last quarter;

- On a revenue basis, the iPhone 12 Series was even more dominant, accounting for a 52.5% share versus 40.5% in units and led by the more expensive Pro Max. Samsung had six models in the top 20 with Huawei, Oppo and Xiaomi having three each and Vivo with one. 17 of the top 20 AMOLED models in Q4’20 were flexible. The top 20 models accounted for a 77% share on a $US basis;

- The top 20 best-selling models, best-selling rigid and best-selling flexible models are all predicted for Q1’21 and Q2’21 on a unit and revenue basis;

- Samsung Display accounted for a 74% unit and revenue share in AMOLED smartphone panels in Q4’20, when it operated at close to 100% of capacity. Although utilization will drop in Q1’21 and Q2’21, it is still expected to maintain more than a 70% share in both units and revenues;

- LGD overtook BOE for the #2 position in AMOLED smartphone panels in Q4’20 on strong iPhone 12 growth. It is expected to maintain a 10% share in Q1’21 as the iPhone 12 gains share as its strong performance continues;

- Apple led in AMOLED smartphone chipset units in Q4’20, while Qualcomm is expected to lead in Q1’21 and Q2’21;

- As a result of the strong iPhone 12 launch, 5G penetration in AMOLED smartphones surged in Q4’20 to 69% on a unit basis and 82% on a revenue basis. A small decline is expected in Q1’21 and Q2’21 as a growing number of rigid OLED 4G phones are launched and gain share, but then there will be another 5G upturn in 2H’21 and beyond;

- Triple camera configurations led with a 41% share followed by quad and dual;

- $501-$700 was the leading price band in Q4’20 while $251-$500 will lead in Q1’21 and Q2’21.

- Forecasts are provided out to 2025 for:

- AMOLED smartphones;

- Rigid AMOLED smartphones;

- Flexible AMOLED smartphones;

- Panel shipments, prices and revenues by size, resolution, refresh rate and backplane technology;

- Smartphone shipments, prices and revenues by size, resolution, refresh rate, network type (4G vs. 5G) and backplane technology;

- Brand units and revenues;

- Display size, aspect ratio, resolution, PPI, touch sensor type, cover glass type, etc.;

- And much more.

For more information on this report including a sample, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。