国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 04/12/2021

OLED Production to Increase 94% Y/Y in Q2 2021

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

A recovery from the pandemic, combined with strong demand for OLEDs in smartphones, TVs and other devices, and coupled with capacity increases, will lead OLED production to grow 94% Y/Y in the second quarter of 2021, according to the latest update to DSCC’s Quarterly OLED and Mobile LCD Fab Utilization Report (一部実データ付きサンプルをお送りします) released last week. Growth in OLED input area for small & medium displays is expected to come in at 68% Y/Y, while growth in OLED TV input area will more than double at +134% Y/Y.

The report details monthly capacity and utilization for OLED lines and LTPS LCD lines, with capability to sort by parameters such as country, substrate type, supplier, form factor and TFT generation. The report includes actual utilization through Q1 2021, a forecast for LTPS LCD utilization for Q2 2021, and a forecast for OLED utilization through Q4 2021.

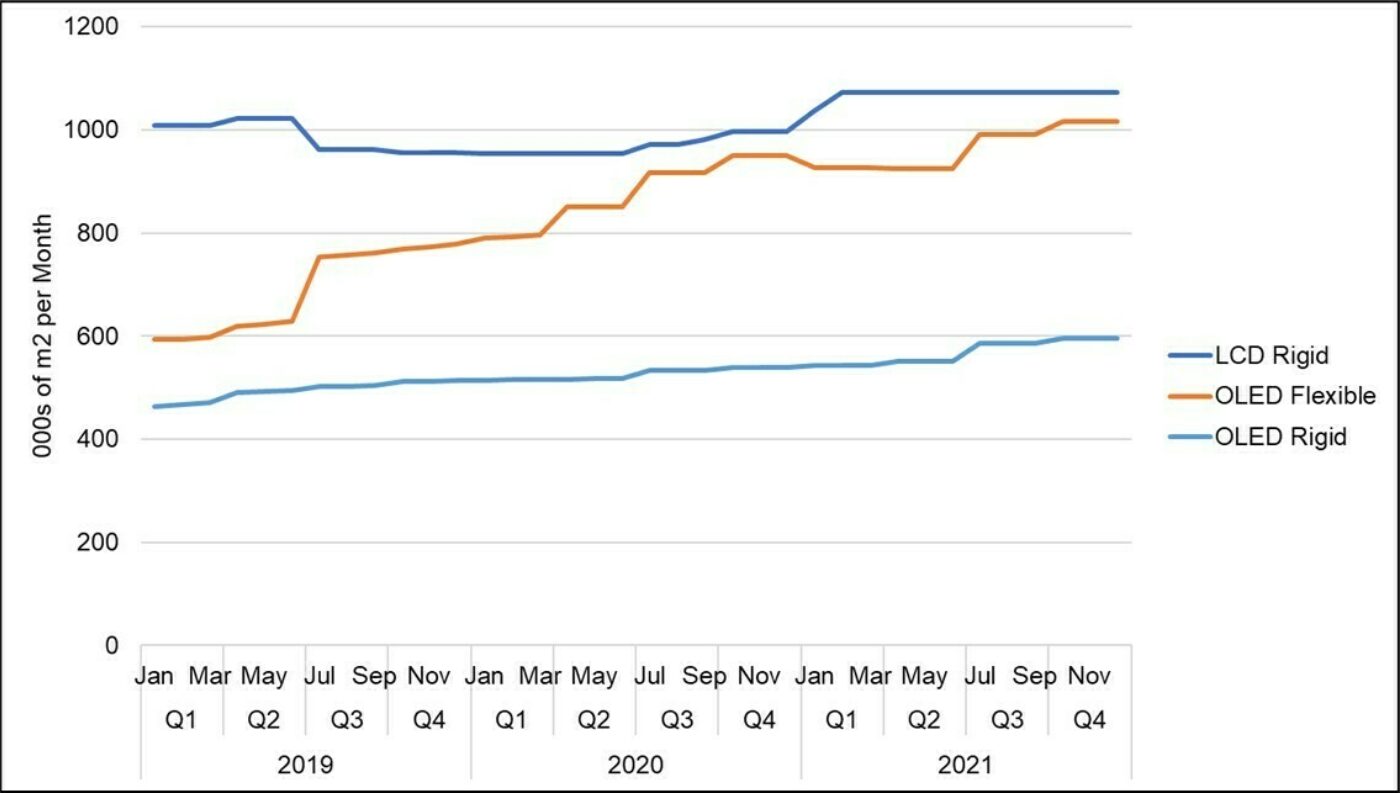

The first chart from the report included here shows the total monthly industry TFT capacity for flexible and rigid OLED for mobile devices and LTPS LCD. While total OLED capacity surpassed LTPS LCD in 2018, the component parts rigid and flexible remain lower than LTPS LCD, which maintains a slim lead in 2021. The shutdown of Japan Display’s Hakusan plant in mid-2019 removed roughly 7% of the industry’s LTPS LCD capacity, but that capacity returns to the industry in 2021 managed by Sharp. Meanwhile, expansions by CSOT Wuhan, Tianma Wuhan and Visionox Hefei will continue to increase flexible OLED capacity, while expansions at Everdisplay and JOLED are increasing rigid OLED capacity in 2021.

OLED and Mobile LCD TFT Capacity, 2019-2021

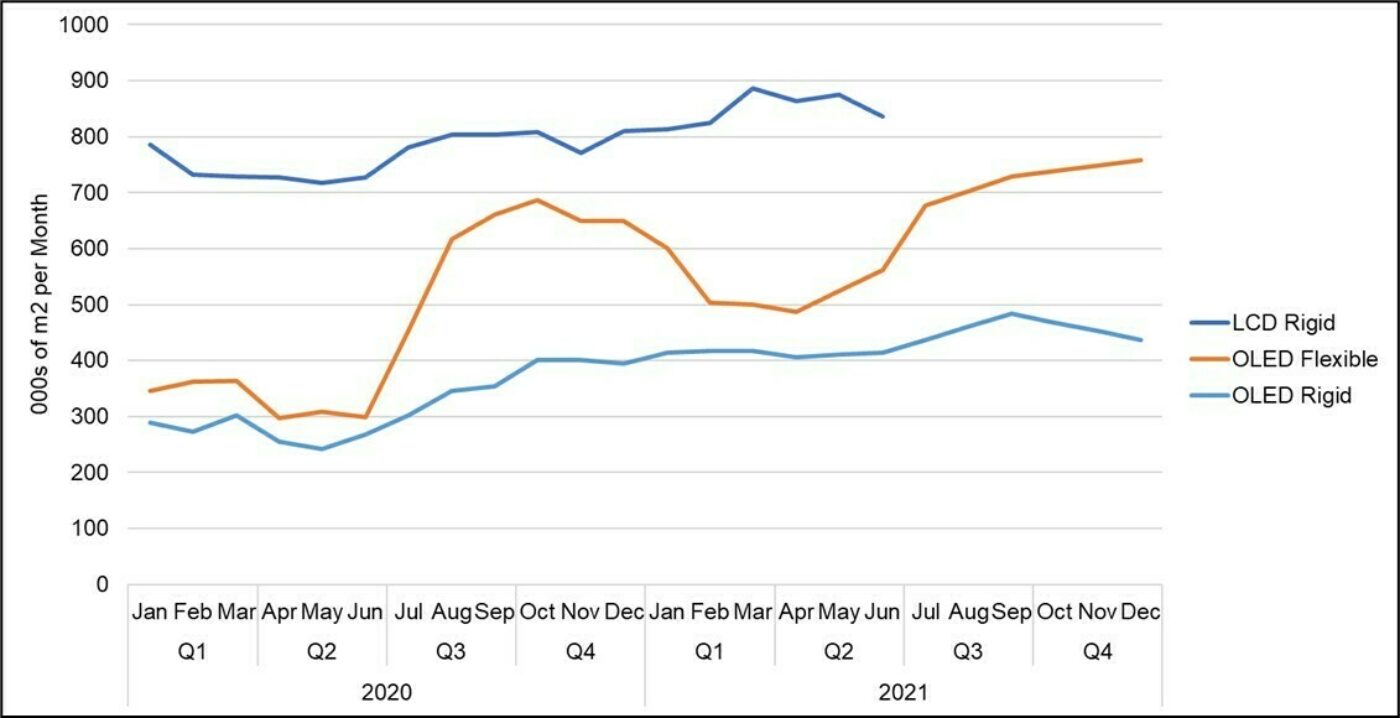

The following chart shows TFT input across the same splits. Flexible OLED has now established a consistent pattern of slower input in the first half of every year, and increasing input in the second half, a pattern which is largely attributable to seasonal demand from Apple and other smartphone makers. This pattern continues in 2021, but with a significant increase in input area, especially in the first half. This first half growth comes from multiple factors: the growth of OLED in the smartphone market, combined with a shift in the timing of Apple’s product launch in 2020, which led to a panel shortage at the end of the year and required continued high production in Q1.

In 2020, rigid OLED utilization was suppressed as LTPS LCD took back some share of the mid-range smartphone market, but rigid OLED is rebounding in 2021 as Samsung has gotten more aggressive on rigid OLED panel pricing. Rigid OLED input area was up 41% Y/Y in Q1 and is expected to be up 61% Y/Y in Q2. LTPS LCD is also showing growth in the first half of 2021 compared with soft demand in the pandemic-affected first half of 2020, with growth of 13% in Q1 and expected growth of 19% in Q2.

OLED and Mobile LCD TFT Input, 2020-2021

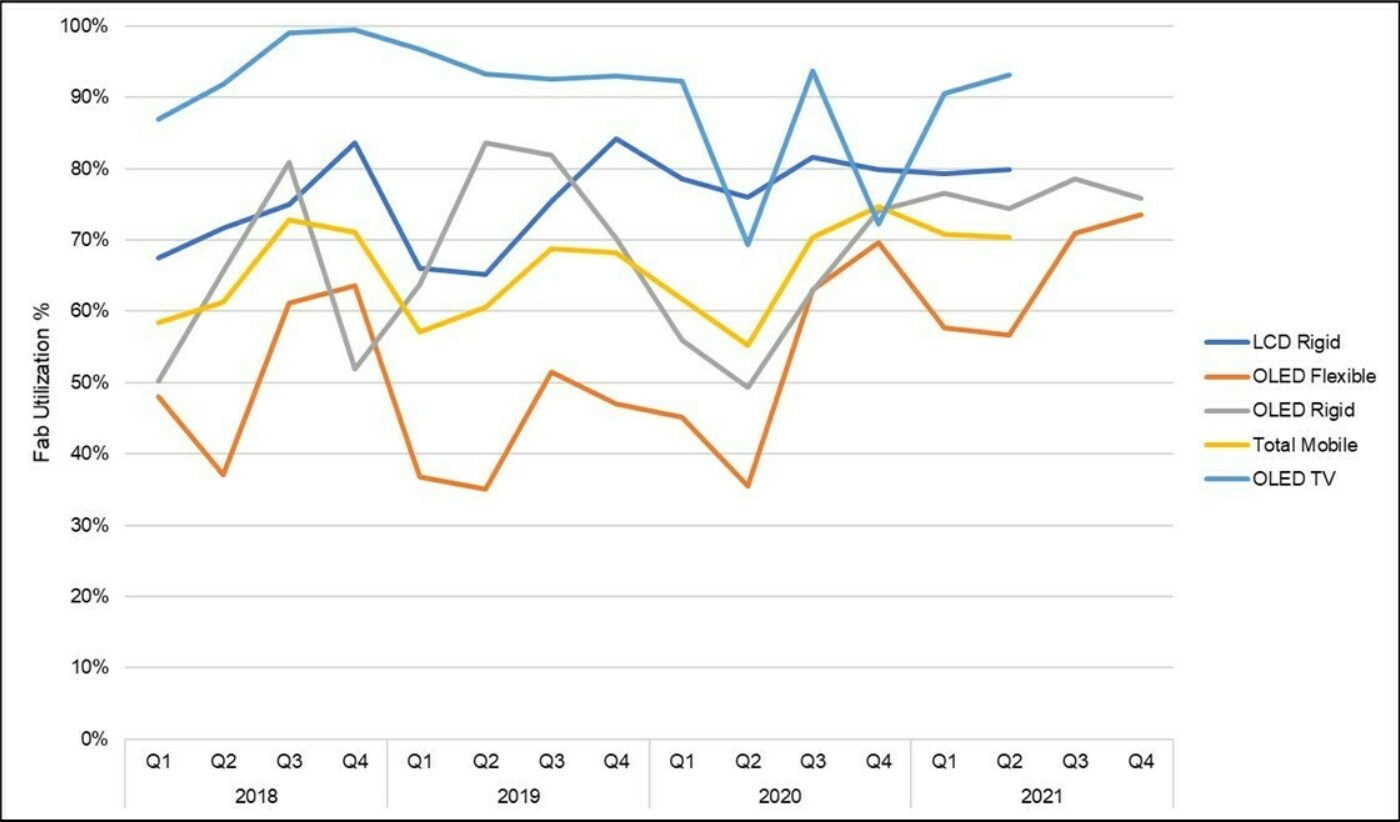

The final chart here shows the resulting utilization numbers, this time with a view by quarters and including OLED TV. Utilization in Q2 2021 is expected to be higher than Q2 2020 for all these groups. OLED TV utilization will be sustained at very high utilization in Q2 as demand for TV panels continues to be strong. The overall flexible OLED utilization is expected to rebound in the second half of 2021, but the overall figure masks some significant differences by fab.

OLED and Mobile LCD Utilization, 2018-2021

With respect to individual fabs, Samsung’s A3 fab is by far the largest flexible OLED fab in terms of capacity. A3 ran at 94% utilization in the second half of 2020, and we expect it to run even higher at 97% in the second half of 2021. LG Display’s E6 fab also benefits from the same seasonality, and we expect it to run at 89% in the second half. On the other hand, BOE continues to struggle with low utilization as it has lost the demand from Huawei and replacing that demand has been challenging. BOE’s B7 line in Chengdu had only 35% UT in the first quarter, and while we expect BOE’s UT to improve during the year steadily, it remains far behind the industry leaders.

DSCC’s Quarterly OLED and Mobile LCD Fab Utilization Report (一部実データ付きサンプルをお送りします) tracks TFT capacity and utilization across 42 OLED and LTPS LCD fabs across this industry, allowing segmentation by supplier, TFT generation, country, backplane technology, frontplane technology and substrate type. For more information about the report, please contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。