国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 04/05/2021

LCD TV Panel Prices Keep Going Up

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

[田村喜男の補足解説] LCD TV用パネル価格の高騰が引き続いている。2020年6月から2021年3月で、既に9か月連続の値上がりが続いている。6月まで値上がりが引き続くと1年間に渡る値上がりとなり、2016年の1年間に匹敵する長期の値上がりとなる。今回のポイントは、長期の継続であることに加えて、過去最大級の騰落率、32インチと55インチサイズのパネル価格が2倍を上回る水準に達するという点である。値上げ率は、2020年9月をピークに2021年1月まで減少傾向であったが、2月・3月と再度値上げ率も上昇に転じている。LCD TV及び全LCDパネル需要は好調であるが、ドライバーICやガラス基板などの供給不足も引き続いており、パネル出荷は増加傾向継続との状況ではなく、2020年下半期から高水準で頭打ちというものである。このような状況下でパネル価格の上昇率はなぜ再度上振れに転ずるのか?ディスプレイ部材の供給不足に加えて、米国テキサス州のSamsung Electronics半導体工場や日本Renesas Electronicsの車載用半導体工場のトラブルも、パネル価格上昇に拍車をかけている模様である。それではパネル価格上昇のピークは一体いつやってくるのであろうか?Q2’21もパネル価格上昇は引き続き、2021年下半期の早めのタイミングでピークアウトするというのが当社の現時点の見解となる。 (4月6日13:30 DSCC アジア代表・田村喜男)

------------

Continuing strong demand for LCD products coupled with increasing concerns about shortages in key components have driven LCD TV panel prices to significant increases in Q1, and prices show no signs of slowing down in Q2. The widespread problems in the supply of Display Driver ICs (DDICs) and the recent announcement by Corning that glass prices will increase, add to the general logistics problems to create an atmosphere where price increases appear to be not only accepted but expected.

In our last update, midway through Q1, we anticipated that price increases would decelerate from Q4 levels, and while this has happened, it is more like a tap on the brakes than a real slowdown. Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, and our current estimate is that average LCD TV panel prices in Q1 2021 increased by another 14.5%. Our outlook for Q2 2021, is for prices to increase another 12%.

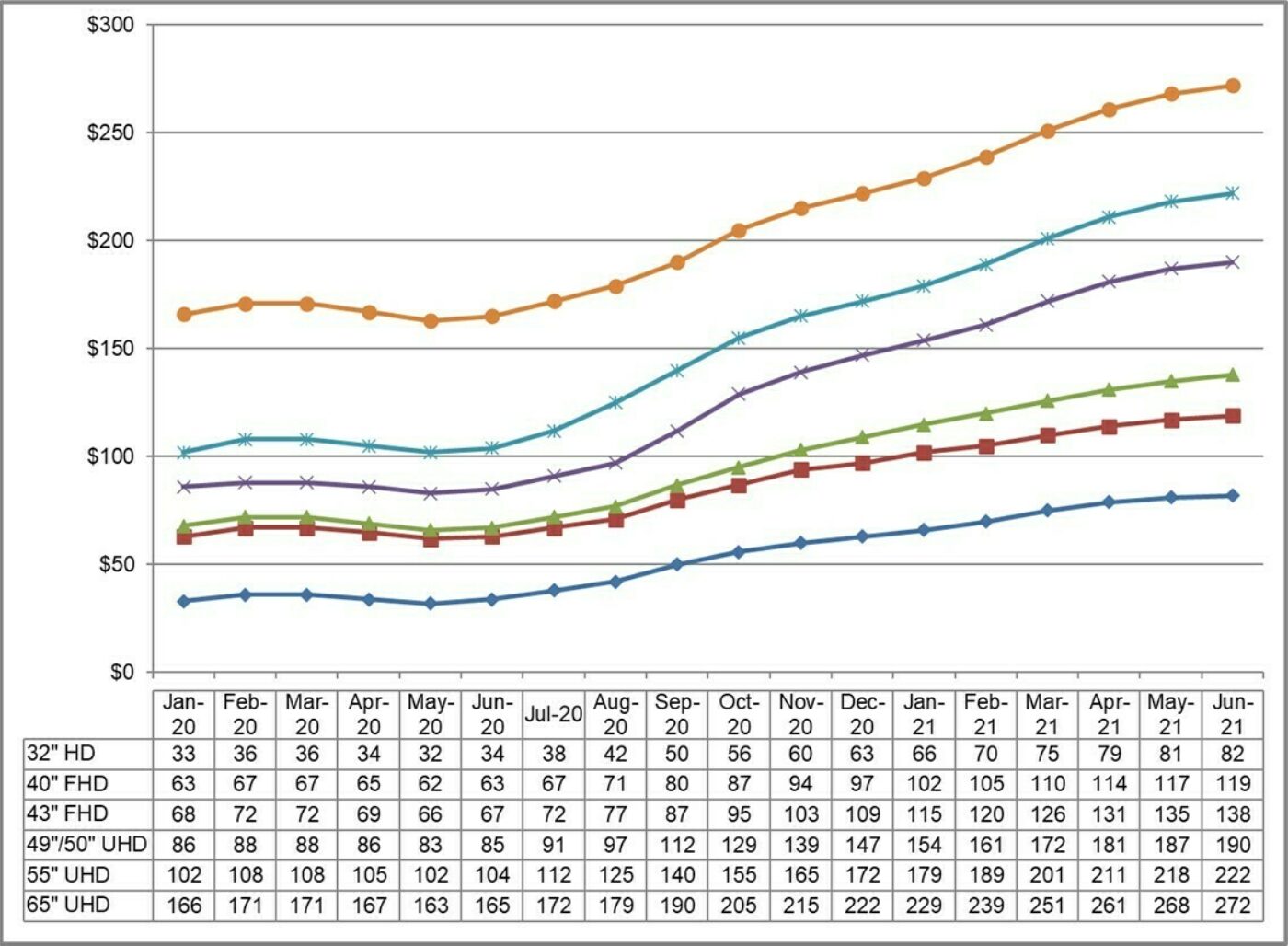

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to a high point in June of this year which may or may not represent a peak. The inflection point for this cycle, the month of the biggest M/M price increases, was passed in September 2020 and the price increases have been slower since then, but after slowing in January to an average of 4.1%, the price increases accelerated in March to 5.4%. Prices in March 2021 reached levels last seen in December 2017.

Prices increased in Q1 2021 for all sizes of TV panels, with double-digit percentage increases in sizes from 32” to 65” ranging from 12% to 18%. Prices for 75” increased by 7% as capacity has continued to increase on Gen 10.5 lines, where 75” is an efficient 6-cut.

Prices for every size of TV panel will continue to increase in Q2 at a similar rate, ranging from 8% for 75” to 15% for 32”, and although we now expect that prices will peak in June or July and will start to decline in Q3, the situation remains fluid.

LCD TV Panel Prices January 2020 – June 2021

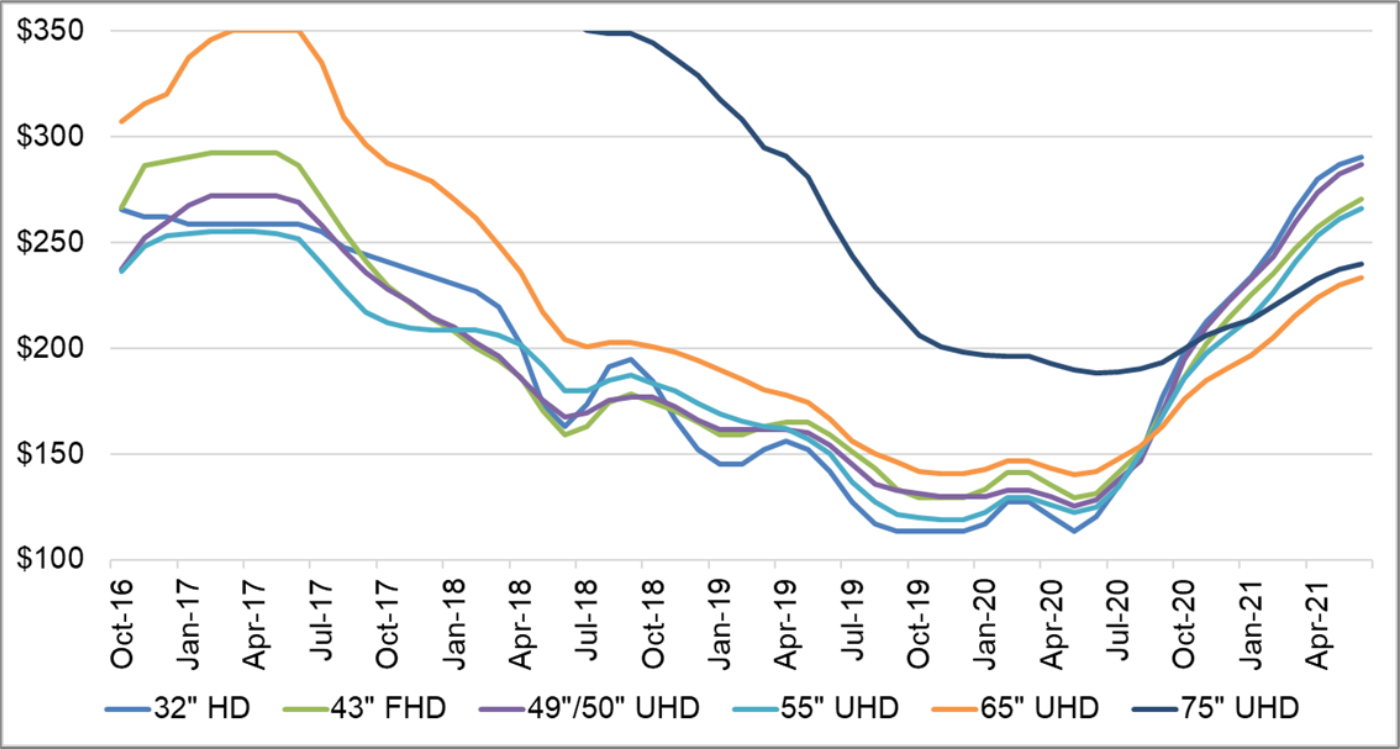

The current upturn in the Crystal Cycle has seen the biggest trough-to-peak price increases for LCD TV panels, and the recent acceleration of prices has further extended this record. Comparing our forecast for June 2021 panel prices, when we expect prices to peak, with the prices in May 2020, we see trough-to-peak increases from 27% for 75” to 156% for 32”, with an average of 100%. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48%, and prior cycles saw smaller increases.

Before the current upswing, the largest panels sold with an area premium, but the current cycle has flipped that upside down, as shown in the next chart. Whereas in May 2020, 75” panels sold at an area premium of $77 per square meter higher than the 32” panel price, as of March 2021 they sold at a $40 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32” panels than from 75” panels. The pattern for 65” is even more severe, and 65” now is the lowest-priced size on an area basis, selling at a $51 per square meter discount (alternately, a 19% area discount) compared to 32”.

Monthly Area Prices per Square Meter for TV Panels, October 2016 – June 2021

The improved pricing for LCD TV panels will boost the profitability of panel makers, especially the two prominent Taiwanese players and LG Display, who have Gen 7.5 and Gen 8.5 fabs but no Gen 10.5 fabs. Chinese panel makers HKC and CEC Panda have a similar industrial profile and stand to benefit, while the leading companies with Gen 10.5 fabs (BOE, CSOT, and Foxconn/Sharp) stand to benefit less, because the price increases on the largest sizes are more modest.

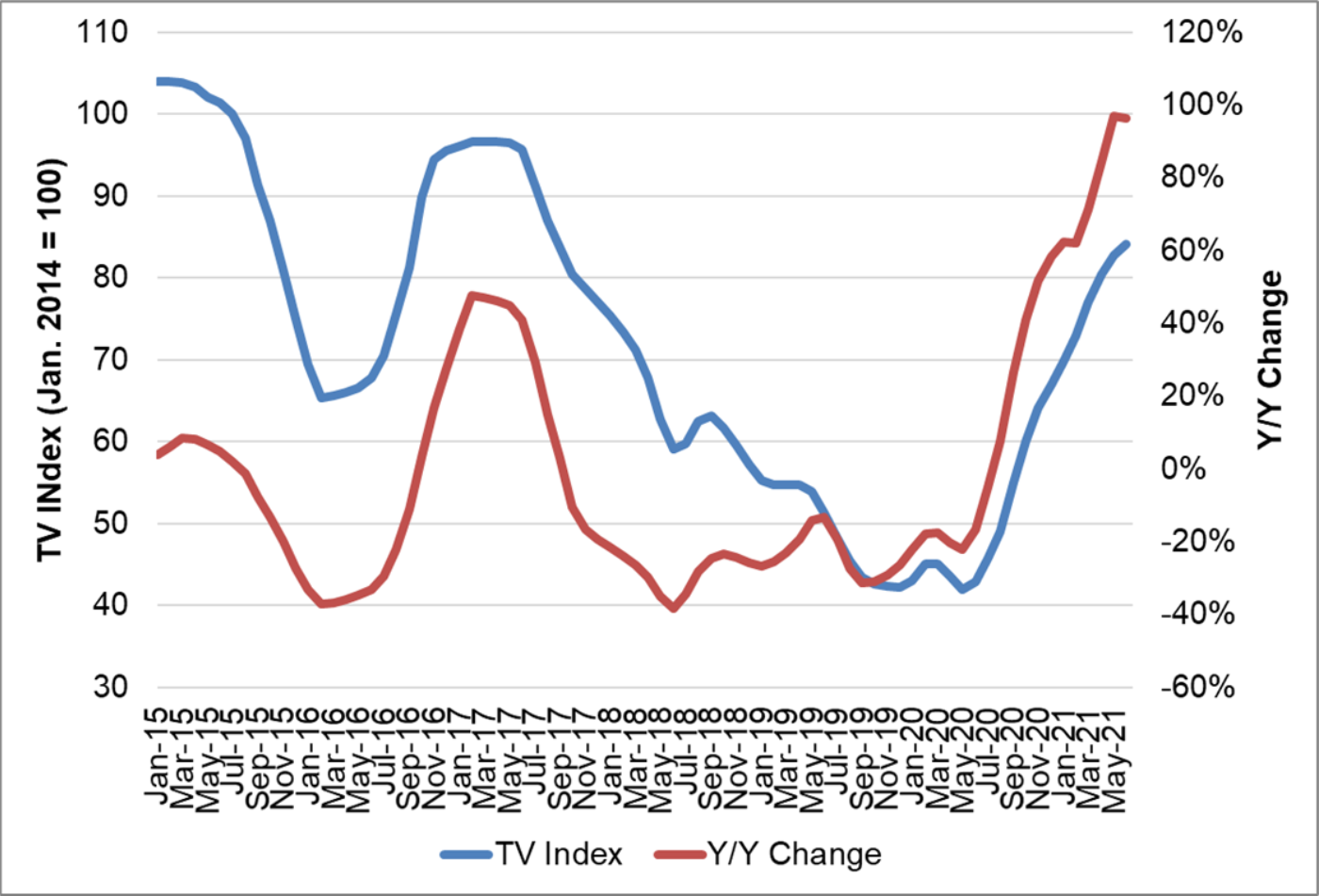

The last chart here shows our TV price index, set to 100 for prices in January 2014, and the Y/Y change of LCD TV panel prices. Our index has increased from its all-time low of 42.0 in May 2020 to 77 in March, and we expect it to reach 84.1 in June before declining in the second half of 2021. The Y/Y increase reaches nearly 100% in May 2021 and will remain at elevated levels throughout the second half of 2021.

TV Panel Price Index and Y/Y Change, January 2015 – June 2021

In addition to being an exceptionally large upcycle, the current upswing matches some of the longest stretches of increasing prices ever seen, a full year from trough to peak. The length of the upswing can be attributed to several factors: glass and driver IC shortages, the pandemic-driven demand or the potential for Korean fab downsizing.

Based on their most recent financial reports, TV makers continued to make strong profits in Q4 2020 despite increasing panel prices. The TV market typically slows down in Q1 and Q2, and TV maker profits typically decline as well. As we noted in our last update, a shift in the retail environment caused by the pandemic may have helped: in-store sales have declined sharply during the pandemic, while online sales have increased. The shift online may have helped TV brands reduce promotional expenses, allowing for greater profitability despite the panel price increases.

For three years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, panel prices are spiking. We saw Korean and Taiwanese panel makers reporting robust margins in Q4 2020 and we expect the good news for panel makers to get even better when those companies report Q1 2021 results.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。