国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 03/16/2021

Display Capacity Growth Upgraded, Now Expected to Fall in 2023 on Korea Shutdowns

Ross Young, Founder and CEOAustin, TX USA -

DSCC has upgraded its display capacity outlook in its latest Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) as a growing number of manufacturers add capacity in response to stronger than expected demand from work from home (WFH), learn from home (LFH) and entertain from home (EFH). In addition, the arrival of miniLED backlights which boosts LCD performance and narrows the performance gap with OLEDs at the high-end of IT and TV markets, should enable LCD manufacturers to raise prices for a growing percentage of its output justifying additional capacity investments.

DSCC upgraded its 2025 display capacity forecast by 9% vs. last quarter’s report and now shows a 2020-2025 CAGR of 4.3%. Most of that increase is coming from LCDs where nearly all LCD manufacturers in China are investing in small expansions or new fabs in response to strong demand and rising prices. LCD capacity is now forecasted to rise at a 3% CAGR vs. 1% previously. Chinese manufacturers also recognize they will be gaining share from Korean LCD manufacturers as they exit or reduce their exposure to the LCD market. We expect SDC and LGD to eventually shut down LCD capacity in Korea which in 2020 accounted for 13% of total LCD capacity. Both SDC and LGD will hold onto their LCD capacity for longer than previously anticipated due to improved market conditions with SDC shutting down all of its LCD capacity by the end of 2021 and LGD expected to shut down all but P9 and AP3 by the end of 2022. As a result of the shutdowns, LCD capacity is expected to decline in 2023 which will temper price reductions which should start from late 2021 or early 2022 as supply improves and component shortages end. It could also lead to another upturn in LCD pricing from late 2022 or 2023. However, the new fabs expected to come online should boost capacity by 5% in 2024 which could result in another cycle of lower prices.

G7 + LCD Supply

The report also converts LCD capacity to yielded supply vs demand and also factors in component shortages. The component shortages in glass and driver ICs are tightening the LCD supply vs. demand picture and are expected to reduce the available supply by at least 2%.

The report also shows a 4% upgrade in OLED capacity based on additional investments and conversions. In 2025, OLEDs will still only account for 13% of total display capacity, up from 7% in 2020 with capacity rising at a 19% CAGR. The report also provides forecasts by:

- Backplane technology

- Flexible vs. rigid form factors

- Display capacity by region

- LCD capacity by region

- OLED capacity by region

- Mobile and flexible OLED capacity by region

- Capacity by application

- Capacity by application by region

- Display, LCD and OLED capacity by generation

- Display, LCD and OLED, mobile OLED and flexible OLED capacity by manufacturer

- Each company’s LCD vs. OLED capacity

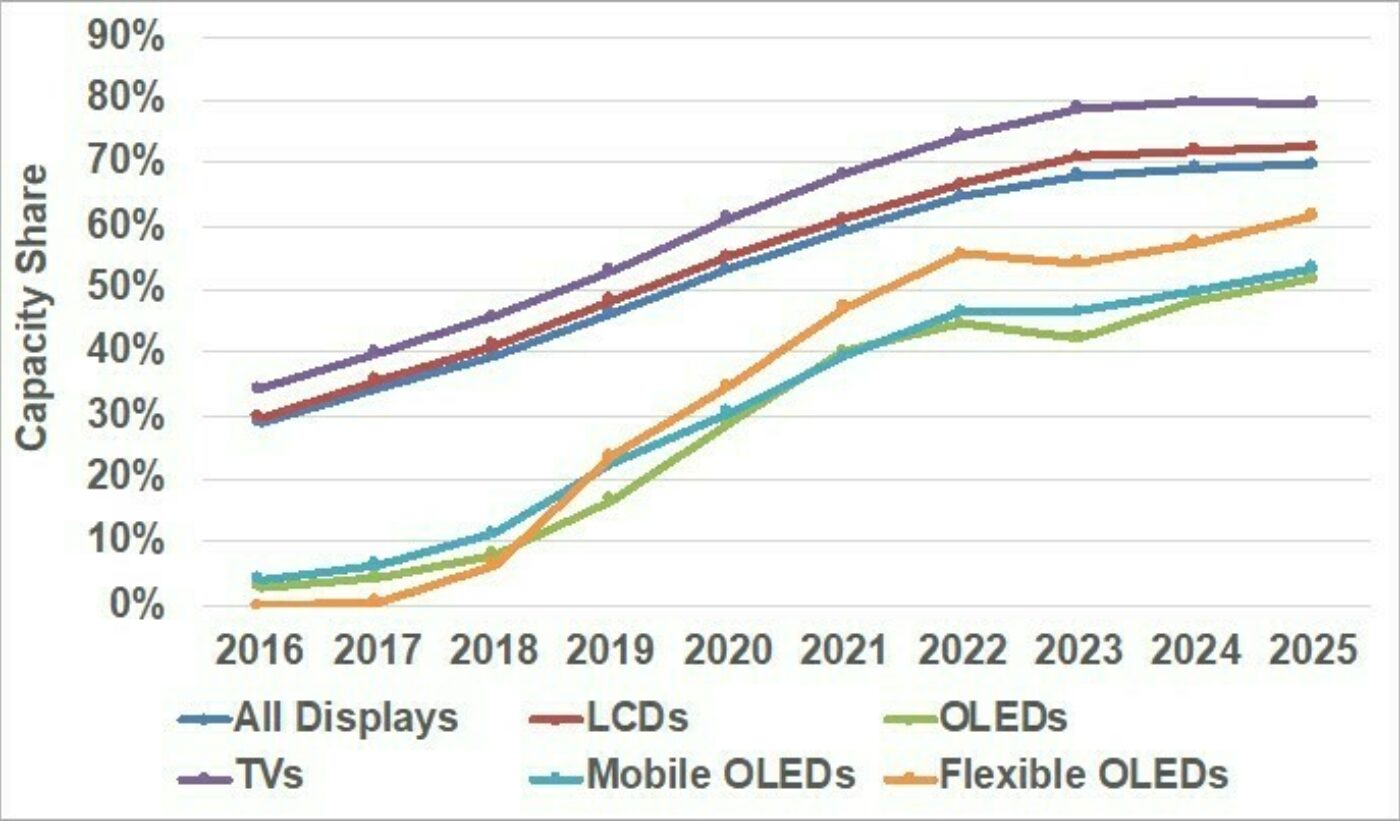

Of note, China’s capacity share by application and technology shows China enjoying more than a 50% share in each major technology and application by 2025. By manufacturer, BOE and China Star are expected to control over a 40% combined share of total display capacity by 2023.

China’s Capacity Share by Technology and Application

For more information on this report, please contact info@displaysupplychain.com.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。