国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 02/22/2021

[Blog] DSCC TV Cost Report Highlights Battle Between OLED and MiniLED

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

DSCC has released its Q4 2020 update of our Advanced TV Display Cost Report, with updates to OLED and LCD cost outlines. This quarter’s edition includes cost models for new sizes of OLED TV panels to be introduced later this year, along with updates to other OLED and LCD sizes including LCD with MiniLED backlights, which will compete with OLEDs for the premium TV space.

The cost report provides detailed cost profiles of 96 distinct LCD products, including combinations of screen size, refresh frequency (60Hz/120Hz), backlight (conventional /QDEF/MiniLED), gen size and manufacturing location (Korea / China) and including open cell models. The report covers 62 distinct OLED products, ranging in size from 31” to 88”, with resolutions from FHD to 8K, and manufactured on Gen 8.5 and Gen 10.5 in China and Korea.

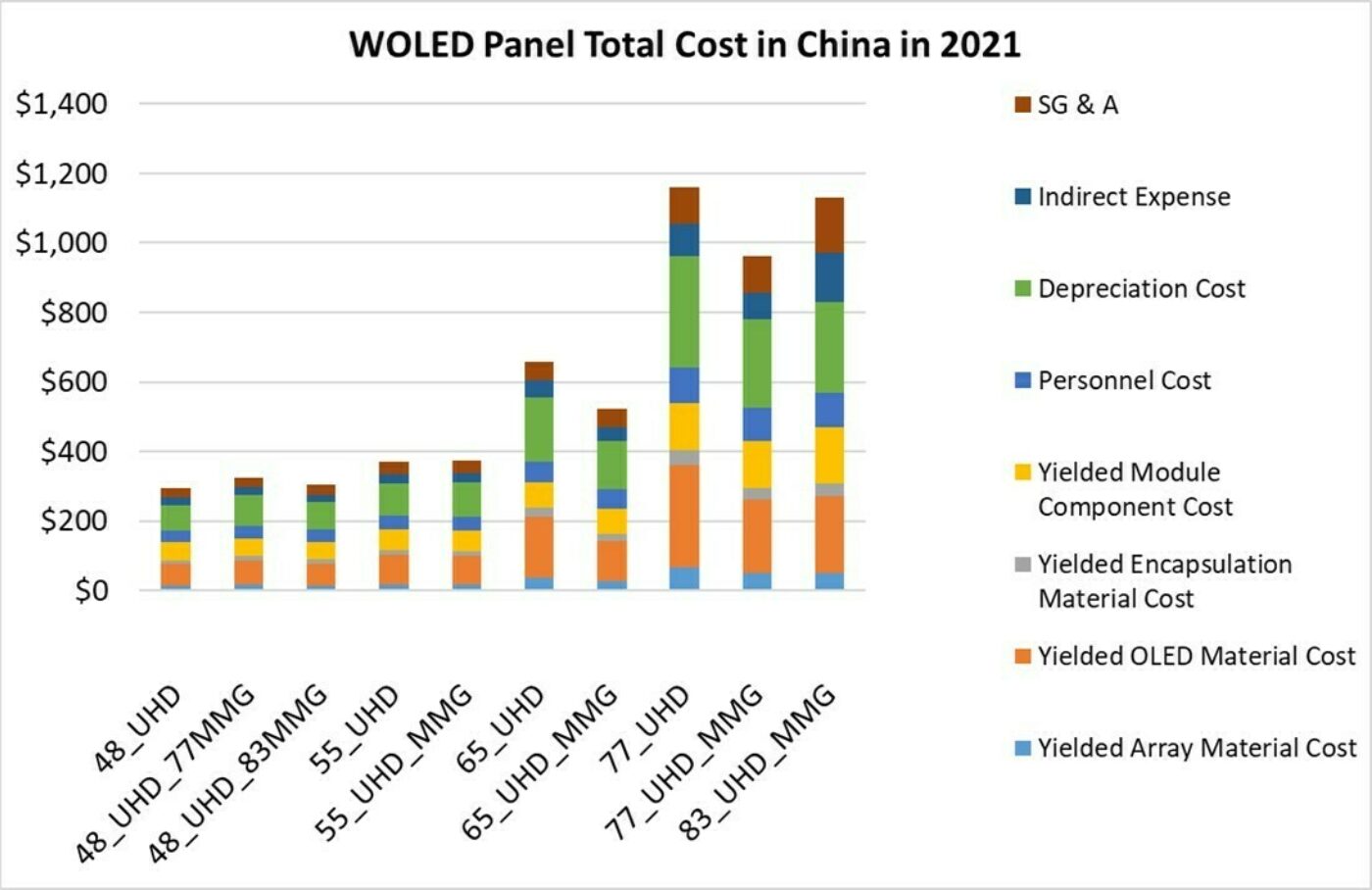

LGD is continuing to improve production at its Gen 8.5 White OLED (WOLED) fab in Guangzhou, China. While our cost report shows that total panel costs from China production in 2020 were higher than the costs for comparable panels made in Korea, by this year the advantages for China production allow lower total costs. China has lower costs for depreciation, personnel, indirect, and SG&A, leading to lower total costs even though yields in Korea will remain higher than China. We estimate that 55” total costs in 2021 in China will be ~14% lower than Korea production, with a similar advantage for 65”.

WOLED TV Panel Cost for China in 2021

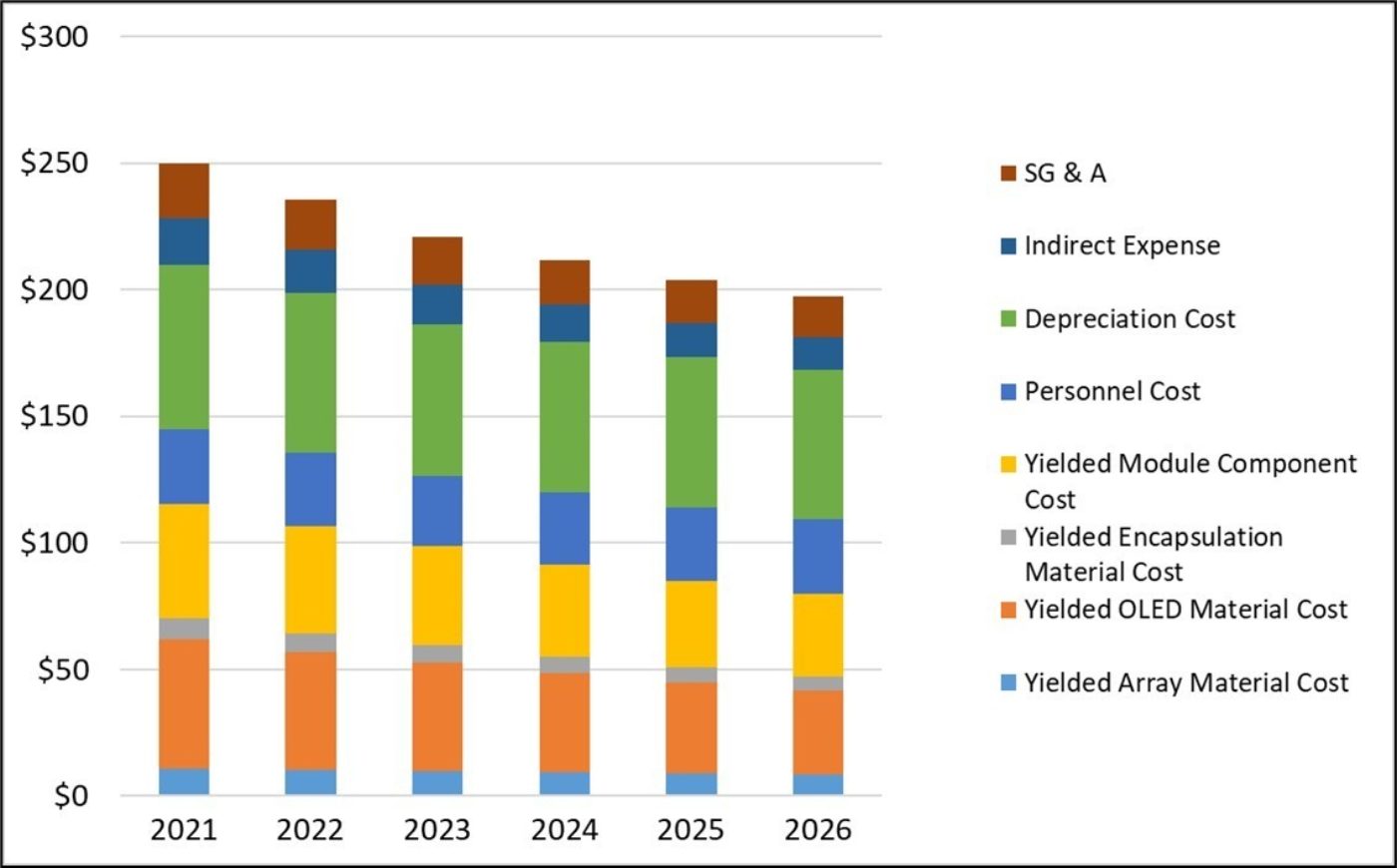

New for this quarter, we include cost models of 31” FHD and 83” UHD panels, plus cost models for 42” UHD panels made in an MMG configuration. LGD’s Gen 8.5 fab can efficiently make 55” and 48” panels in a conventional configuration (6-up and 8-up, respectively), but 42” panels cannot be made efficiently without MMG. As a comparison, whereas 55” 6-up reaches 90% glass utilization and 48” 8-up reaches 91%, a standard configuration for 42” (also 8-up) achieves only 70% utilization. The MMG for 42” involves 8-up panels in landscape mode, plus 2-up 42” panels in portrait mode, to achieve 87% glass utilization.

Bottom Emission 42” WOLED UHD Panel Total Cost on G8.5 in China with MMG

LGD hopes to sell 7M to 8M OLED TV panels in 2021, compared to 4.4M in 2020, and to help this effort it will introduce new screen sizes that can allow lower price points. Whereas prior to 2020 LGD’s lowest cost OLED TV panel was a 55”, the cost of 48” UHD panels is 20% lower than 55” UHD, and the cost of 42” UHD panels is 33% lower. This will allow LGD’s customers to introduce OLED TVs at lower price points which will broaden the market.

In our prior update to this report in Q3 2020, we introduced MiniLED cost models for the first time, and the Q4 report updates these. The report allows for comparison across the wide range of performance (and cost) within LCD, from conventional LCD with 60Hz refresh to 120Hz to QDEF panels and finally MiniLED + QDEF. Combined with the OLED cost models, the report allows a complete comparison of the cost of all large-screen TV types.

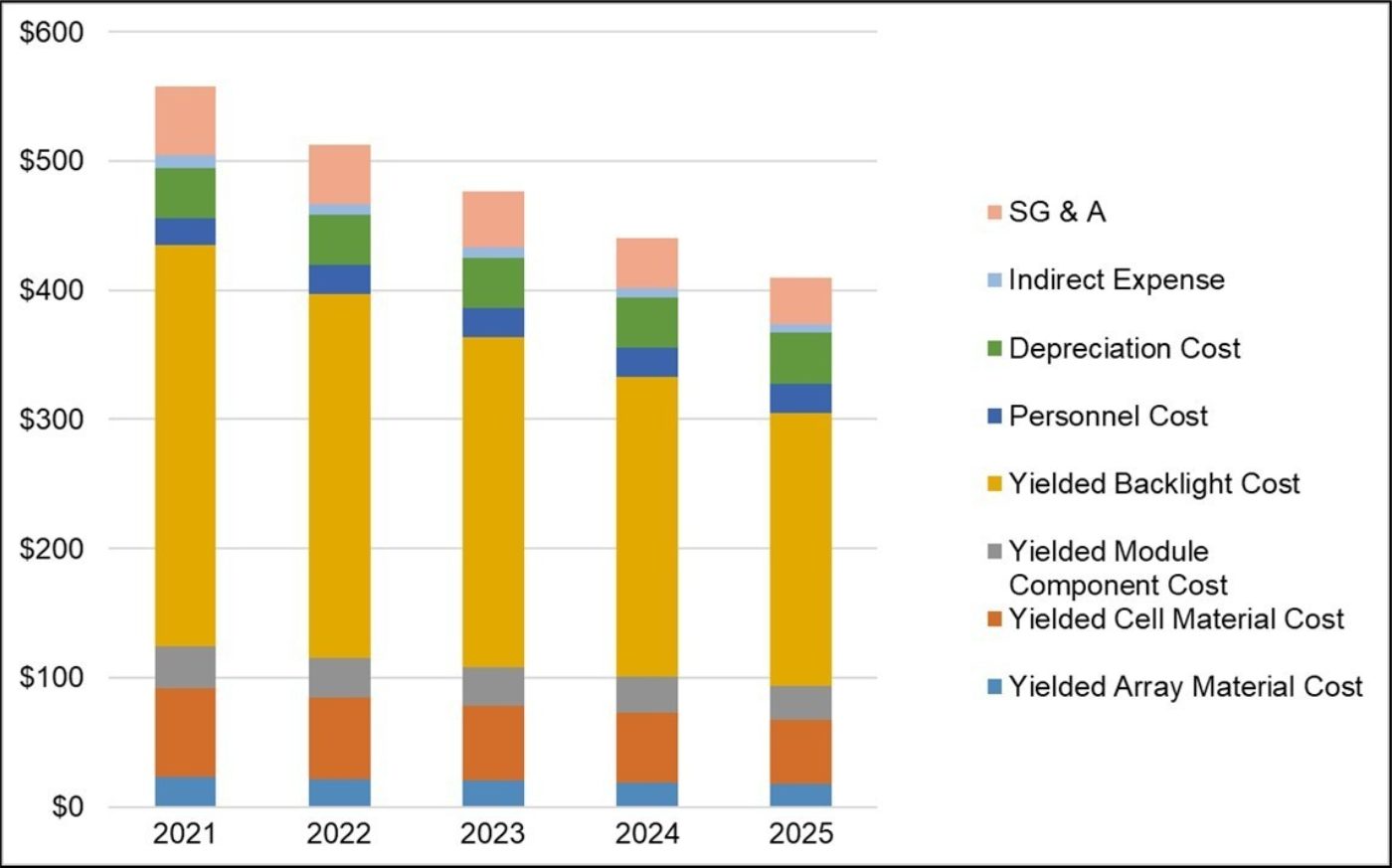

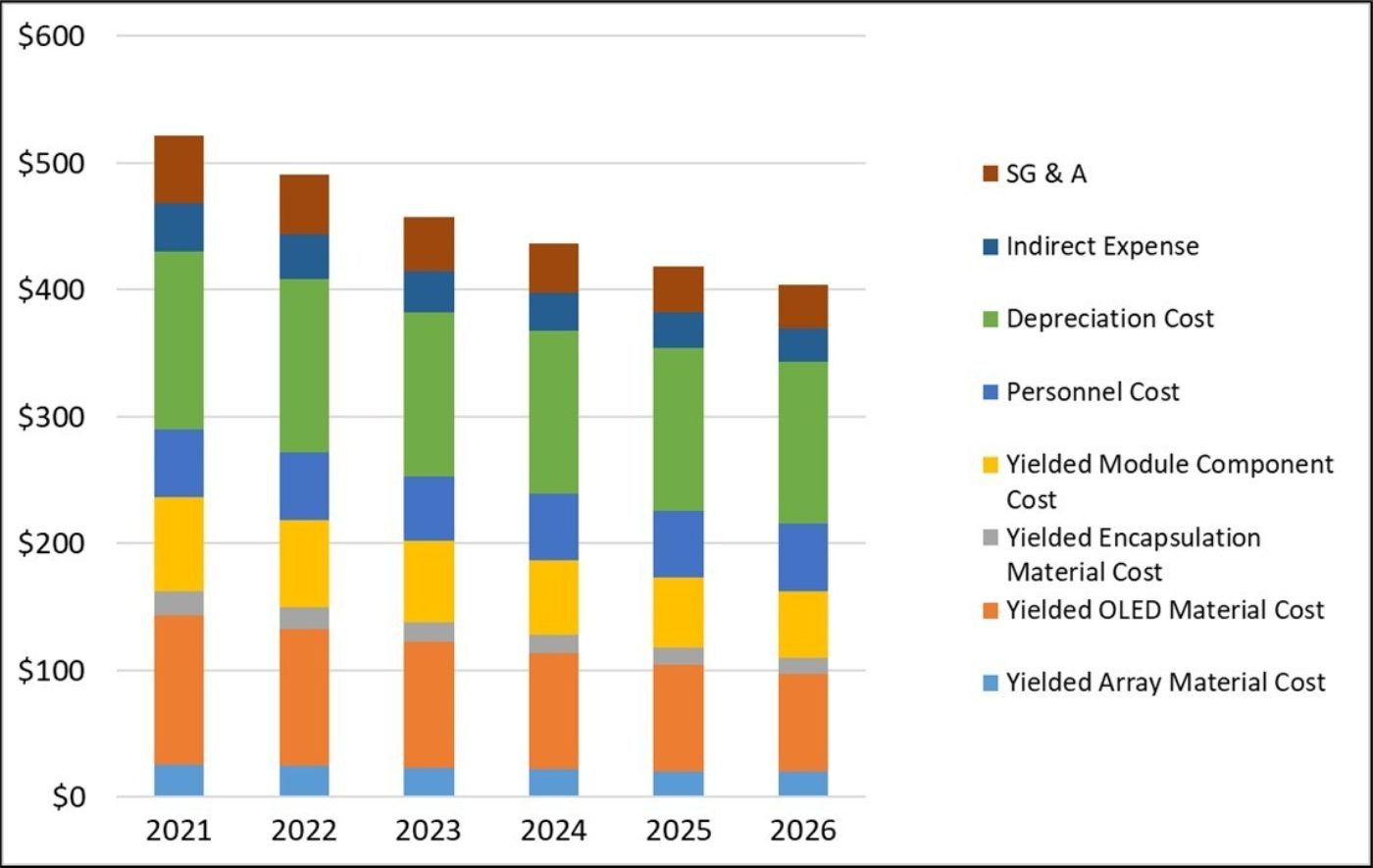

The next two charts here show the cost profiles for 65” panels, comparing MiniLED LCD with WOLED, in the most cost-effective fabs (China Gen 10.5 for LCD, China Gen 8.5 MMG for WOLED). The WOLED product in 2021 costs less than the MiniLED, but we expect the cost of MiniLED to decrease faster than WOLED, so the cost premium declines from 7% in 2021 to cost parity in 2025.

65” UHD 60Hz LCD Module Cost on Gen 10.5 in China with MiniLED and QD

Bottom Emission 65” UHD WOLED Panel Total Cost on Gen 8.5 in China with MMG

MiniLED and OLED will compete in the marketplace, and the cost profile of the two technologies shows they are both much more expensive than conventional LCD. This suggests that MiniLED TV products will compete at retail price points similar to WOLED TV, and that’s what we’ve seen from Samsung’s early pricing for its QD Neo MiniLED TVs.

MiniLED will have many variations across brands and product lines, with different levels of cost/performance depending on the number of LEDs. The highest-performance MiniLED TV panels will have even higher cost than our estimates, but there will also be some less expensive MiniLED designs on the market. For a more comprehensive overview of MiniLED panel costs that highlights these variations, see DSCC’s MiniLED Backlight Technology, Cost and Shipment Report.

With the pandemic-fed surge in TV demand, TV makers have been solidly profitable despite rising LCD TV panel prices. Those higher LCD prices may boost the prospects for OLED TV, but MiniLED models will compete with OLED at premium price points, and this may eventually lead to a price war between these competing technologies.

As noted above, subscribers to the Advanced TV Cost Report receive cost profiles of all major product configurations competing in the premium TV space in both LCD and OLED. The report includes Excel files with the detailed cost models in tables and in graphical form, and a PowerPoint which outlines the main findings of this quarter’s update. The PowerPoint includes comparisons of competing technologies (such as WOLED vs. Inkjet Printing, or LCD vs QDEF) and differing manufacturing platforms (Korea vs. China, Gen 8.5 vs. Gen 10.5). DSCC Weekly Review readers interested in subscribing to the Advanced TV Cost Report should contact info@displaysupplychain.co.jp.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。