国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 08/02/2021

LCD TV Panel Price Update Confirms Price Peak

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

Our latest update and forecast of LCD TV prices confirms our view of one month ago that prices are peaking in June or July 2021 and will decline for the rest of the year. The demand surge, which resulted from the COVID-19 pandemic, has eased and industry supply has caught up to demand. Even with the declines in the second half, prices at year-end will remain higher than they were in December 2020 and dramatically higher than their all-time lows.

In our June and July updates, we referred to a series of events that suggested slowing demand and increasing supply, and recent developments have only confirmed this outlook. The increasing panel prices have led to an unprecedented increase in TV prices in the US, which will hinder demand. The path of the pandemic continues to suggest a headwind for global TV demand, as emerging economies are still struggling with COVID and suffering an economic slowdown.

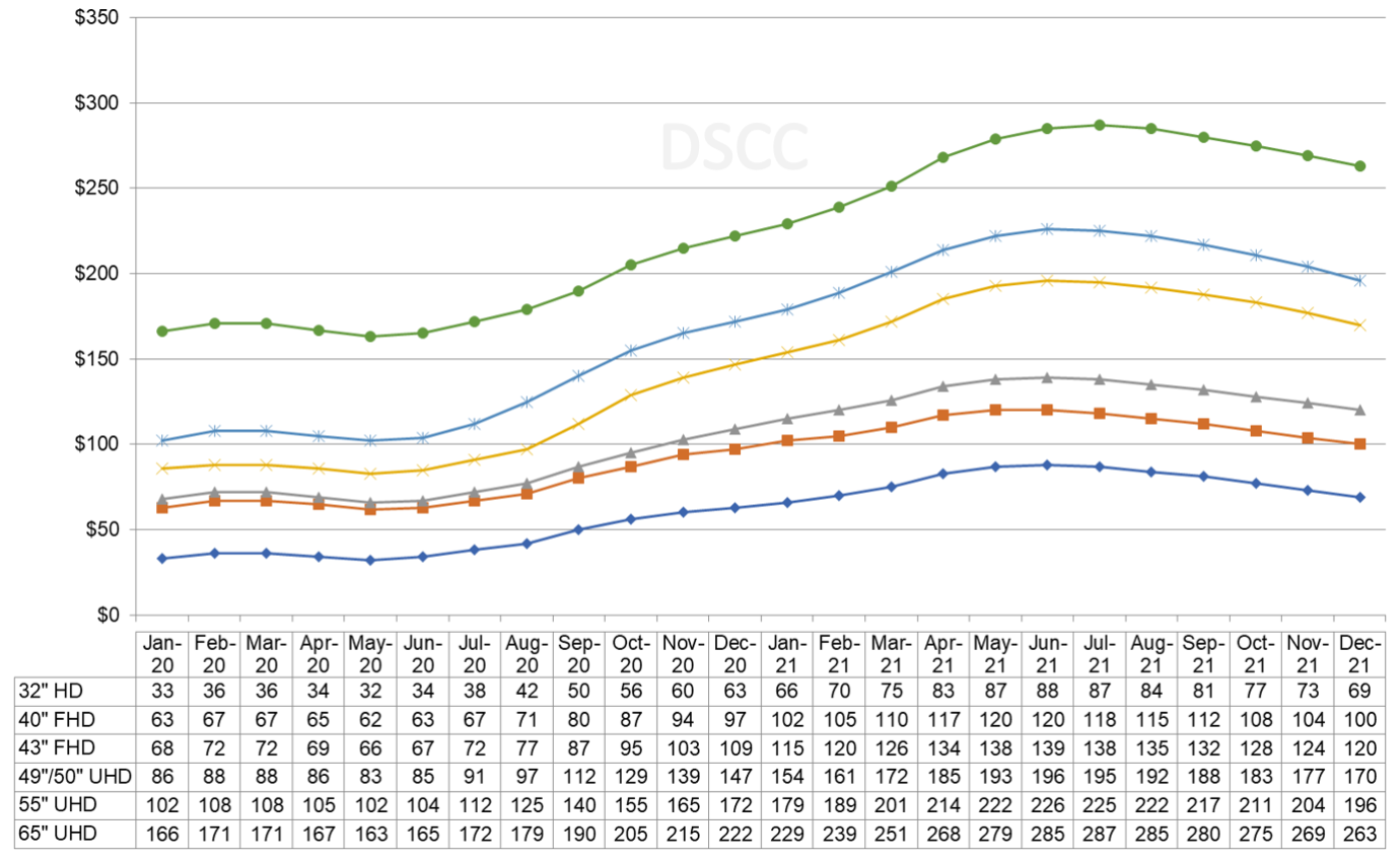

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to a high point in June or July of 2021 and then a decline to December 2021. We saw multiple inflection points for the year-long up cycle, but we now see the slowdown, which started in May 2021, as the end of the cycle. The peak prices in June/July 2021 reached levels last seen in July 2017.

Prices increased in Q2 2021 by a double-digit percentage for all sizes of TV panels, with increases ranging from 11% to 22%. The average price increase in Q2 for the seven screen sizes we track was 16%. Over the past year, the prices for 75” have increased by the smallest percentage as capacity has continued to increase on Gen 10.5 lines, where 75” is an efficient 6-cut.

LCD TV Panel Prices January 2020 - December 2021

We estimate that smaller TV screen sizes (32” up to 55”) peaked in June while the largest sizes (65” and 75”) peaked in July. Smaller screens saw the largest increases in the up cycle, with sizes made efficiently on Gen 10.5 (65” and 75”) having the smallest increases. As a result, in Q3 2021, we expect that prices for the three small sizes will decrease Q/Q while prices for the four larger sizes will increase Q/Q.

The current upturn in the Crystal Cycle has seen the biggest trough-to-peak price increases for LCD TV panels, far exceeding previous Crystal Cycle rallies. Comparing our forecast for peak panel prices (in June or July 2021) with the prices in May 2020, we see trough-to-peak increases from 32% for 75” to 175% for 32”, with an average of 106%. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48%, and prior cycles saw smaller increases.

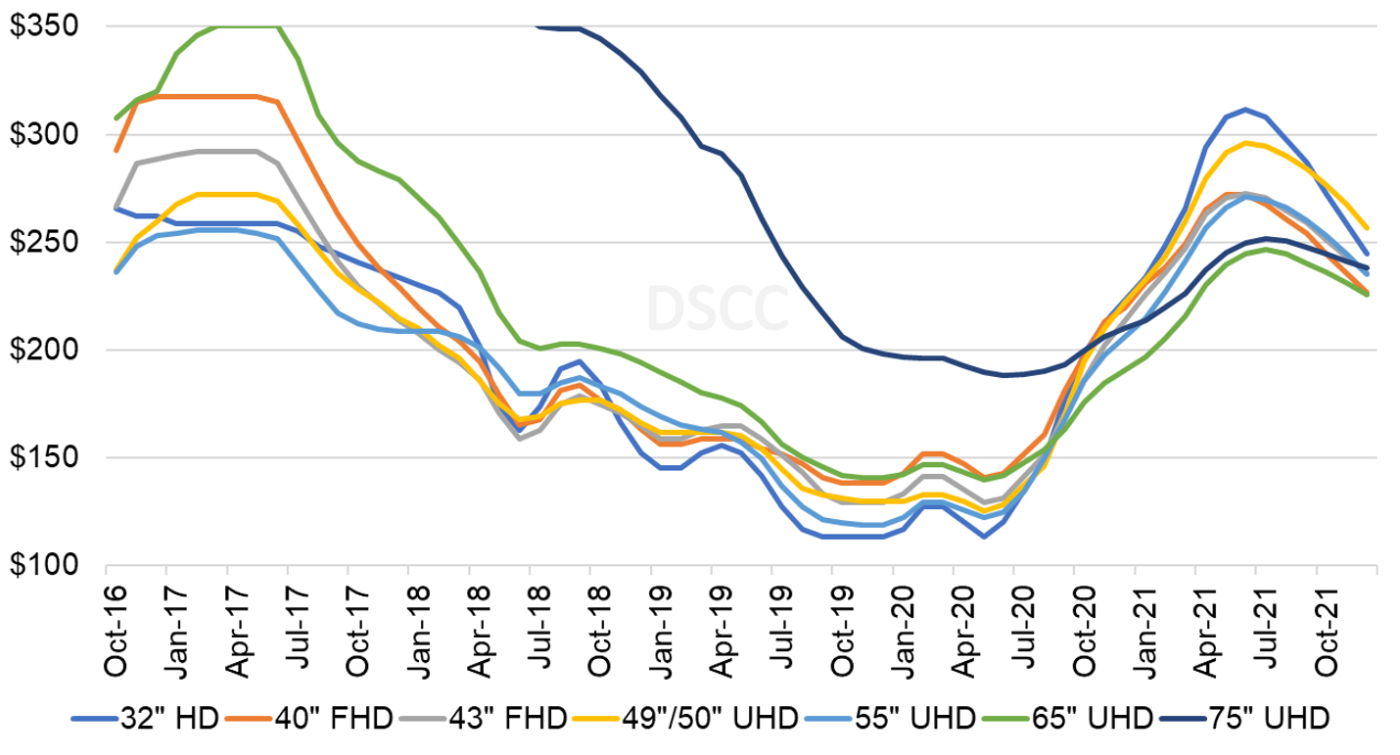

As we look at pricing on an area basis, we have noted that smaller screen TVs are the most commoditized: prices for 32” panels fall the fastest during a period of oversupply and rise the fastest during a period of shortage. We see that pattern repeating again as we head into oversupply. Before the current upswing, the largest panels sold with an area premium, but the year-long rally flipped that upside down, and the shift to oversupply is expected to have the pattern flip again, as shown in the next chart.

Monthly Area Prices per Square Meter for TV Panels, October 2016 - December 2021

Whereas in May 2020, 75” panels sold at an area premium of $77 per square meter higher than the 32” panel price. As of July 2021, they were selling at a $56 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32” panels than from 75” panels. The pattern for 65” is even more severe, and in June, 65” was selling at a $67 per square meter discount (alternately, a 21% area discount) compared to 32”.

In the second half of 2021, though, we expect 32” TV panel prices to fall fastest, with a 22% decline between June and December 2021, while 75” TV panel prices decline only 5% from their mid-year peak. By the end of the year, we expect area prices for the smallest and largest panels to be close to the same, and no doubt 32” panels will again be the lowest price on an area basis in 2022.

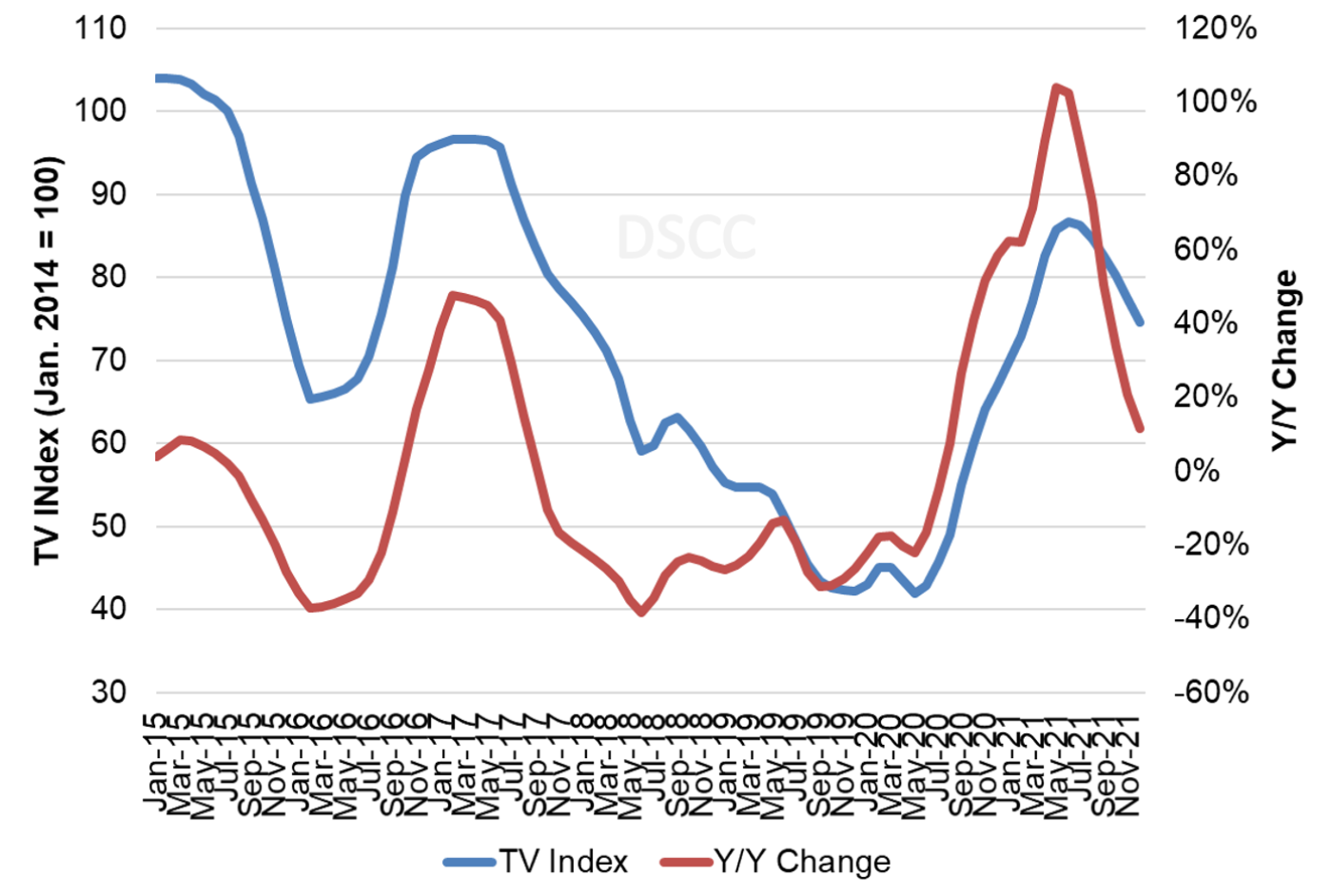

The last chart here shows our TV price index, set to 100 for prices in January 2014, and the Y/Y change of LCD TV panel prices. Our index has increased from its all-time low of 42.0 in May 2020 to 87 in June 2021, but this represents the peak and we expect the index to decline to 75 at year-end. The Y/Y increase surpassed 100% in May and June 2021 and will remain positive but at declining levels through the second half of 2021.

TV Panel Price Index and Y/Y Change, January 2015 - December 2021

In addition to being an exceptionally large upcycle, the current upswing matches some of the longest stretches of increasing prices ever seen, more than a full year from trough to peak. The length of the upswing can be attributed to several factors: glass and driver IC shortages, the pandemic-driven demand or the potential for Korean fab downsizing.

Based on their most recent financial reports, TV makers continued to make strong profits in Q2 2021, despite increasing panel prices. The earnings results from Samsung and LG for Q2 2021 confirm that both companies’ TV businesses remained solidly profitable in Q2, and both companies indicated that they expect to be profitable in the second half. With demand remaining strong, TV makers have weathered the increase in panel prices and remained very profitable, but if demand falls off, especially in the richest markets of North America and Western Europe, TV makers will pull back.

For three years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, we have seen a historic year of increases in panel prices. We have seen LGD and AUO post robust profits for the second quarter of 2021 (see separate stories), and we expect that other panel makers will enjoy similar profitability. Although we expect prices to start declining in Q3, the prices averaged over a full quarter are close to flat, and some companies may see a net increase in price depending on product mix. Even modest price declines in Q4 will sustain high profitability for LCD panel makers, who appear to be in line for record full-year profits.

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。