国内お問い合わせ窓口

info@displaysupplychain.co.jp

FOR IMMEDIATE RELEASE: 02/01/2021

「Blog] LGD Books Big Q4 Profit But Full Year Loss for 2020

Bob O'Brien, Co-Founder, Principal AnalystAnn Arbor, MI USA -

The big increases in LCD TV panel prices and a seasonal increase in shipments of OLED panels helped LG Display (LGD) to its best quarter for profitability in more than three years in Q4 2020, but LGD’s Q4 profits fell just short of bringing the company to profit for the full year.

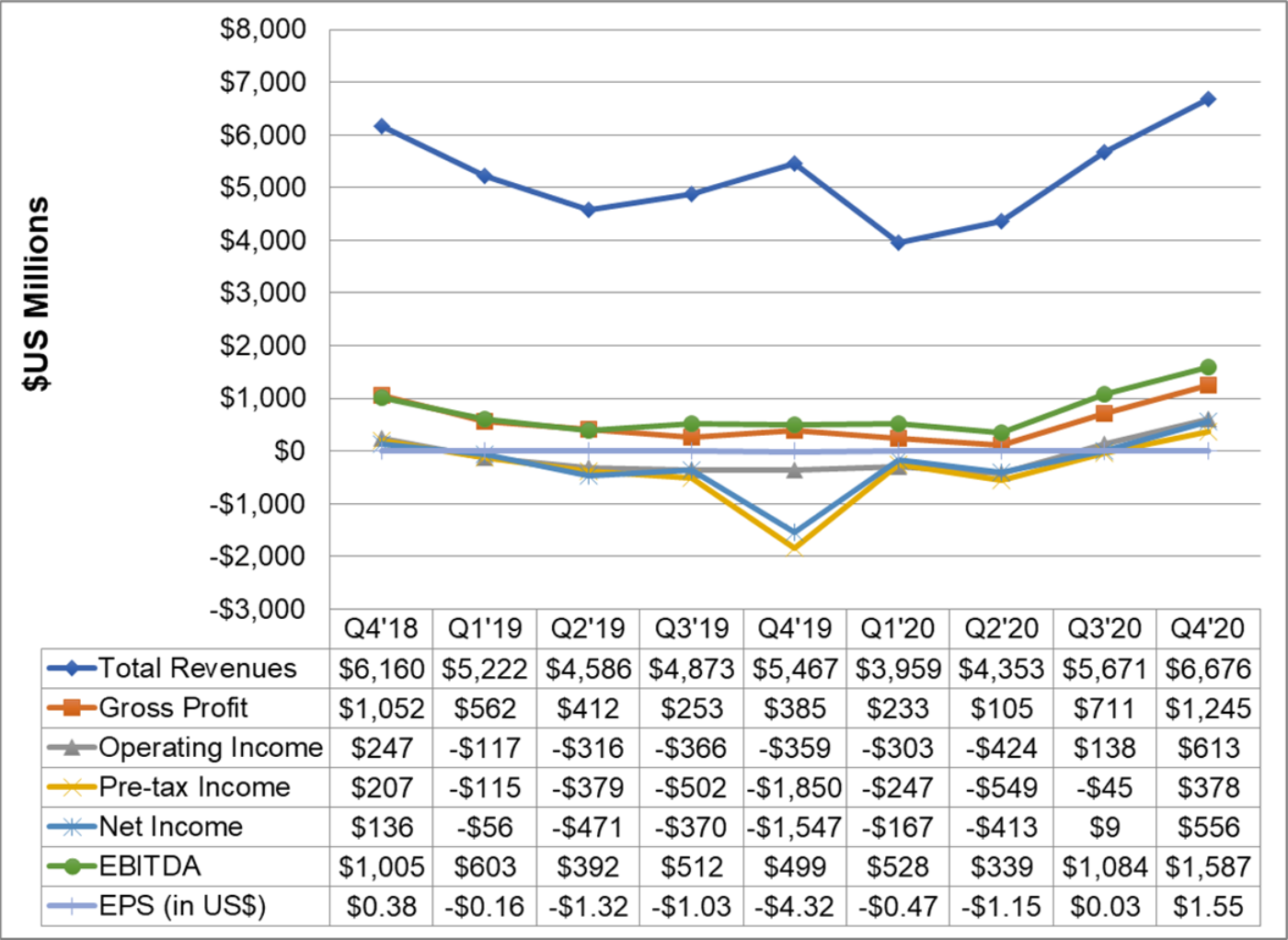

LGD reported a net profit of KRW 621 billion (US$556 million) on revenues of KRW 7.5 trillion ($6.7 billion) for the October to December quarter. Revenues increased 18% Q/Q and 22% Y/Y and reached the highest level since Q4 2016, and exceeded consensus analyst expectations of KRW 7.2 trillion. Both operating profits and net income soundly beat analyst expectations of KRW 278 billion and KRW 126 billion, respectively. LGD recorded KRW 685 billion ($613 million) in operating profits, its highest profit level since Q2 2017.

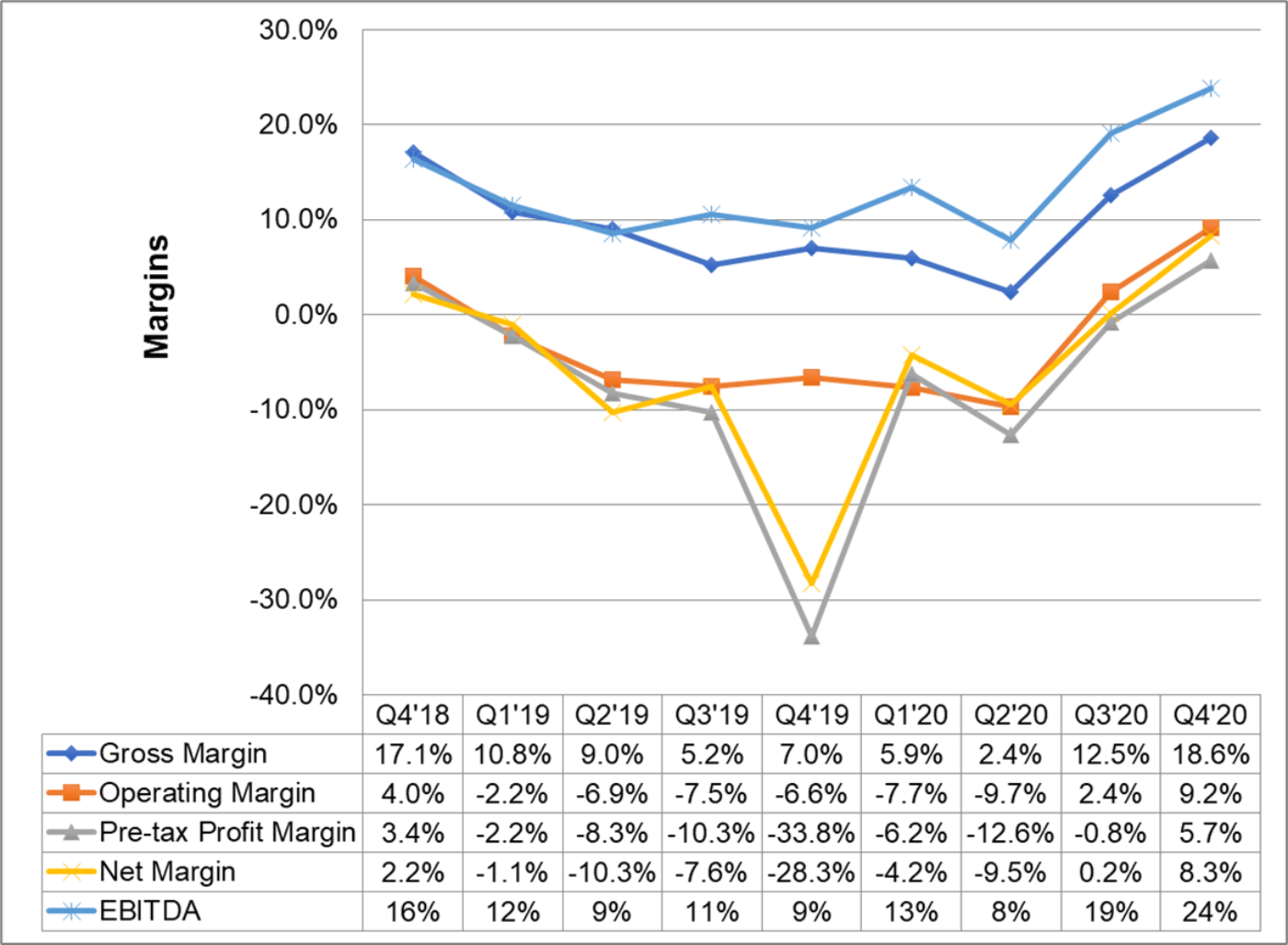

LGD’s margins all improved dramatically for the 2nd quarter in a row, by between 5% and 8%, with gross margins improving to 19% and EBITDA margins of 24% hitting the highest level since Q1 2017. LGD needs continued EBITDA improvement to generate cash to fund its transition from commoditized LCD to OLED, and booked an impressive KRW 1.8 trillion (US$1.6 billion) in Q4.

LG Display Income Statement Highlights, Q4 2018 to Q4 2020

LGD modestly outperformed guidance given in its Q3 earnings call. In late October, LGD guided to expect low-single-digit % growth in area shipments, and managed 5% area growth in Q4. Area shipments were still down 5% Y/Y at 8.7 million square meters but LGD’s capacity utilization, which had been in the 70s for the first three quarters, increased to 81%. LGD’s guidance on area ASP was a cryptic “keep the pace of increase”, and area prices increased 12% sequentially in Q4 and 30% Y/Y to $790 per square meter.

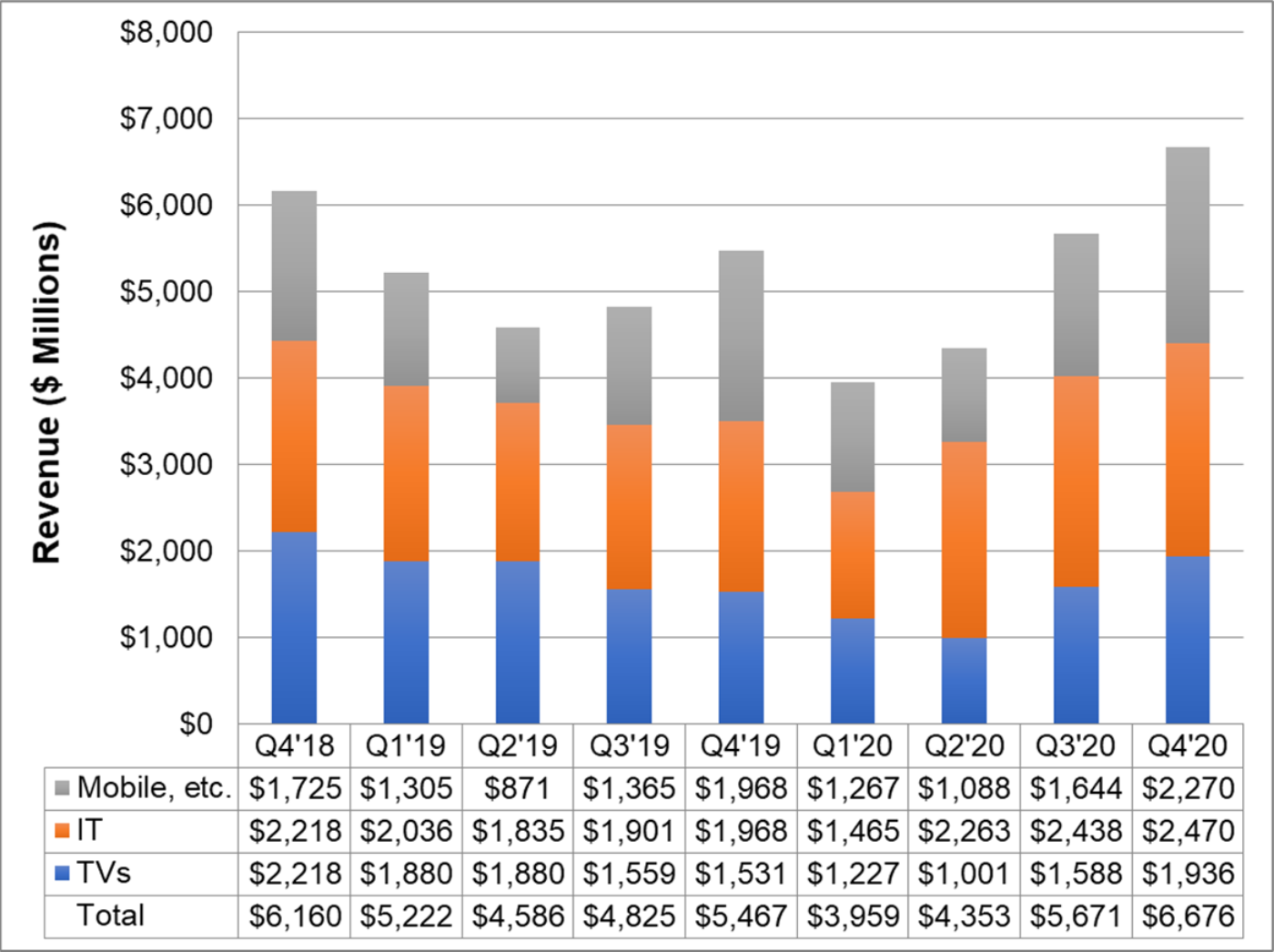

In Q3 2020, LGD changed its reporting by application, combining Monitors and Notebooks into an “IT” category, so it now reports only three product segments: TV, IT and Mobile. Following its established seasonal pattern, LGD’s share of revenue from Mobile panels increased sharply in Q4 to 34% of the total, taking share from IT which dropped from 43% in Q3 to 37% in Q4. In absolute value, IT revenue increased by just 1% Q/Q while Mobile revenue increased by 38% Q/Q and 15% Y/Y.

LG Display Revenue by Application, Q4 2018 to Q4 2020

Since mobile panels have the highest area prices, LGD’s product mix shift in Q4 helped to increase its area ASP, adding to the increases in LCD TV panel prices. LGD’s area prices increased to $790 per square meter, their highest level since at least 2013.

LGD’s Q4 profits helped it improve its balance sheet. LGD reported a positive cash flow from operations of KRW 1004 billion ($898 million). LGD’s inventory decreased by $77 million, and inventory days decreased from 37 to a lean 33. LGD again booked more than KRW 1 trillion in depreciation in the quarter, as the company starts to depreciate its OLED TV lines in Guangzhou.

LGD’s capex in 2020 has been restrained compared to its big investment surge in 2018-2019, and Q4 capex was the lowest since at least 2014 at KRW 254 billion ($227 million). LGD recorded positive free cash flow of KRW 750 billion ($671 million), bringing the full year almost up to positive free cash flow at KRW -50 billion (-$7 million).

LGD’s debt level increased to $12.6 billion, while LGD’s book value of equity increased by 11% to $11.4 billion. LGD debt to equity improved from 118% to 110%, and net debt to equity improved from 90% to 76% during the quarter.

The debt picture continues to look much worse if you consider the market value of LGD’s equity, which despite a recent increase in the stock price remains 51% lower than its book value. LGD’s market capitalization as of October 23rd was KRW 8.23 trillion ($4.99 billion), so LGD’s debt to market equity is still a hefty 170%, but this is greatly improved from mid-2020.

LGD provided the following guidance for Q1 and 2021:

- LGD expects area shipments to be flat Q/Q in Q1.

- LGD expects ASPs to decline by high-single digits on product mix changes.

- Sales of OLED TV panels in 2021 will be 7-8 million units.

- Capex in 2021 will be in mid KRW 2 trillion level, and capex will be less than EBITDA.

In other notes from the earnings call:

- LGD expects TV and IT demand to remain solid in Q1.

- LGD’s “P-OLED” or plastic OLED (we refer to this as flexible OLED) is expected to record better Y/Y results in 2021 with reduced seasonality, and profitability will show a sizeable improvement, but LGD did not make a statement that P-OLED would be profitable.

- Korea LCD TV capacity will be run flexibly based on short term supply/demand and customer needs.

- In terms of LCD TV supply/demand, Samsung sustaining their capacity is a less important factor than the Gen 10.5 capacity increases in China.

- LGD will monitor the market to determine when to add capacity at its Guangzhou Gen 8.5 OLED TV line. That line could increase from 60k/month to 90k/month (note – DSCC expects the added 30k to have MP in Q2 2021).

About Counterpoint

https://www.displaysupplychain.co.jp/about

[一般のお客様:本記事の出典調査レポートのお引き合い]

上記「国内お問い合わせ窓口」にて承ります。会社名・部署名・お名前、および対象レポート名またはブログタイトルをお書き添えの上、メール送信をお願い申し上げます。和文概要資料、商品サンプル、国内販売価格を返信させていただきます。

[報道関係者様:本記事の日本語解説&データ入手のご要望]

上記「国内お問い合わせ窓口」にて承ります。媒体名・お名前・ご要望内容、および必要回答日時をお書き添えの上、メール送信をお願い申し上げます。記者様の締切時刻までに、国内アナリストが最大限・迅速にサポートさせていただきます。